Author: Mike Shell

-

Gifts are given. Asymmetry comes from choices.

Talent may help investors understand markets, but it rarely determines outcomes. Asymmetric results come from choices—defining downside, sizing positions intentionally, and maintaining convex opportunities within a disciplined portfolio process. Read More Read More

-

What Stanley Druckenmiller Actually Means by “Rate of Change” — And Why It’s the Foundation of Asymmetric Risk Management

Most investors watch price and call it analysis. More sophisticated investors watch momentum. Very few monitor the change in momentum itself — the acceleration, the second derivative, the variable that often shifts before price confirms… Read More

-

S&P 500: Where Asymmetric Risk Accelerates

Markets don’t break gradually—they transition. The S&P 500 is approaching a key level near 6,550 where behavior shifts, volatility expands, and risk begins to compound. The difference isn’t direction—it’s what happens if you’re wrong. Read More

-

When the Hedge Stops Hedging

Many investors believe bonds protect them when equities fall. But in certain regimes, that relationship breaks down. When inflation, rates, and growth expectations pull markets in different directions, the hedge investors rely on may stop… Read More

-

S&P 500: Where Asymmetric Risk Accelerates

S&P 500: Where Asymmetric Risk Accelerates Markets don’t break gradually—they transition. The S&P 500 is approaching a key level near 6,550 where behavior shifts, volatility expands, and risk begins to compound. The difference isn’t direction—it’s… Read More

-

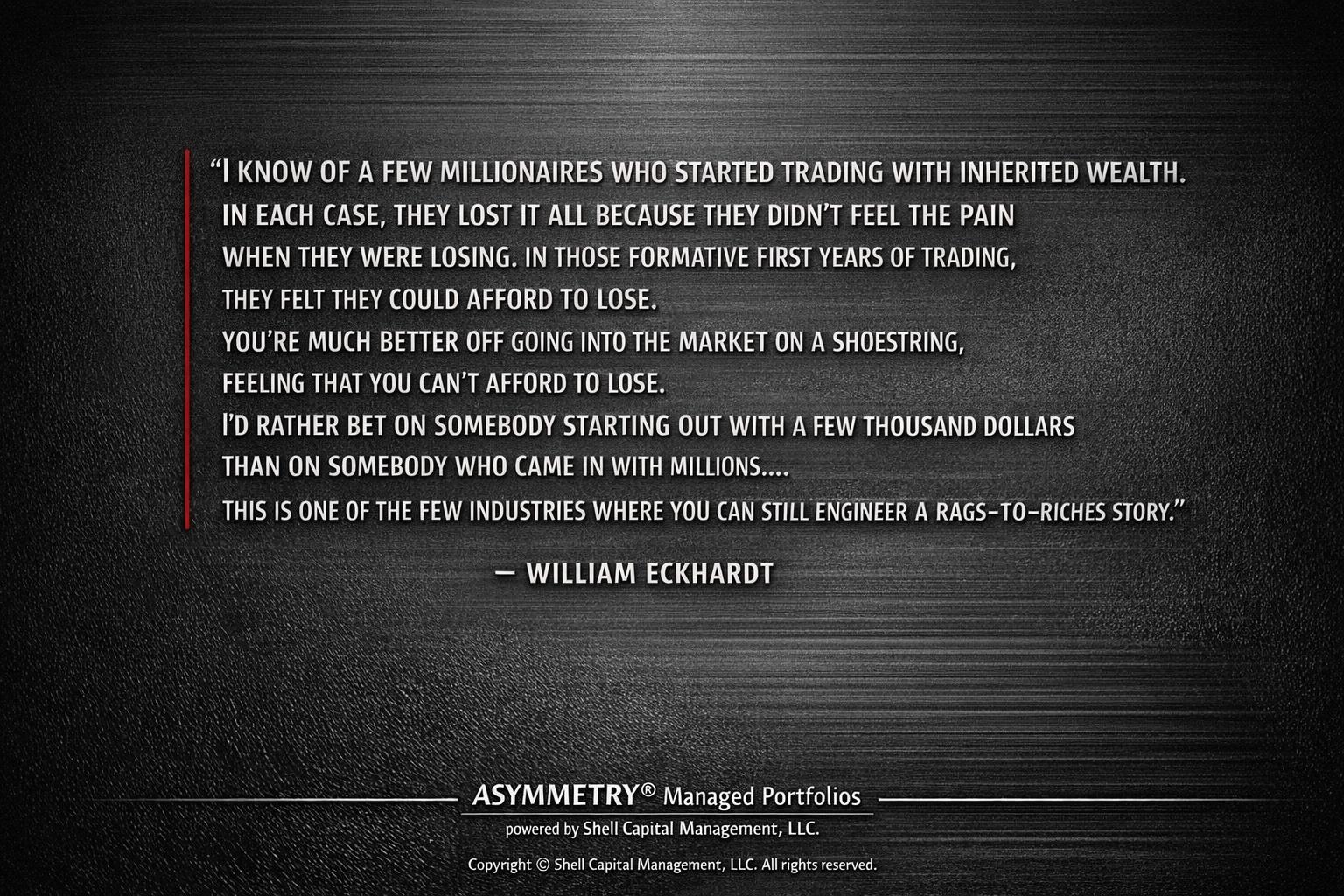

Why Feeling the Loss Matters

William Eckhardt’s warning is simple: people who don’t feel the pain of loss often lose everything. The real edge in investing isn’t starting with more capital. It’s building a process that defines downside before the… Read More

-

Capital Efficiency Sounds Like Optimization. It’s a Leverage Decision.

Capital efficiency expands exposure, but it also increases interaction risk. When stacked exposures move together, drawdowns accelerate and recovery math becomes more demanding. Read More

-

Heads I Win, Tails I Don’t Lose Much

This isn’t asset allocation. It’s risk allocation. Define the downside first, size positions intentionally, and structure portfolios so upside can expand while losses remain contained. Read More Read More

-

When the Hedge Stops Hedging

Many investors believe bonds protect them when equities fall. But in certain regimes, that relationship breaks down. When inflation, rates, and growth expectations pull markets in different directions, the hedge investors rely on may stop… Read More

-

The Three Dimensions of Risk — And How We Engineer Around Them

Risk isn’t a single score — it’s the interaction between risk tolerance, risk required, and risk capacity. At Shell Capital, we engineer portfolios by aligning psychological comfort, return objectives, and financial absorption ability to create… Read More