Asymmetric Returns: Definition, Meaning, and Why It Matters

What Are Asymmetric Returns?

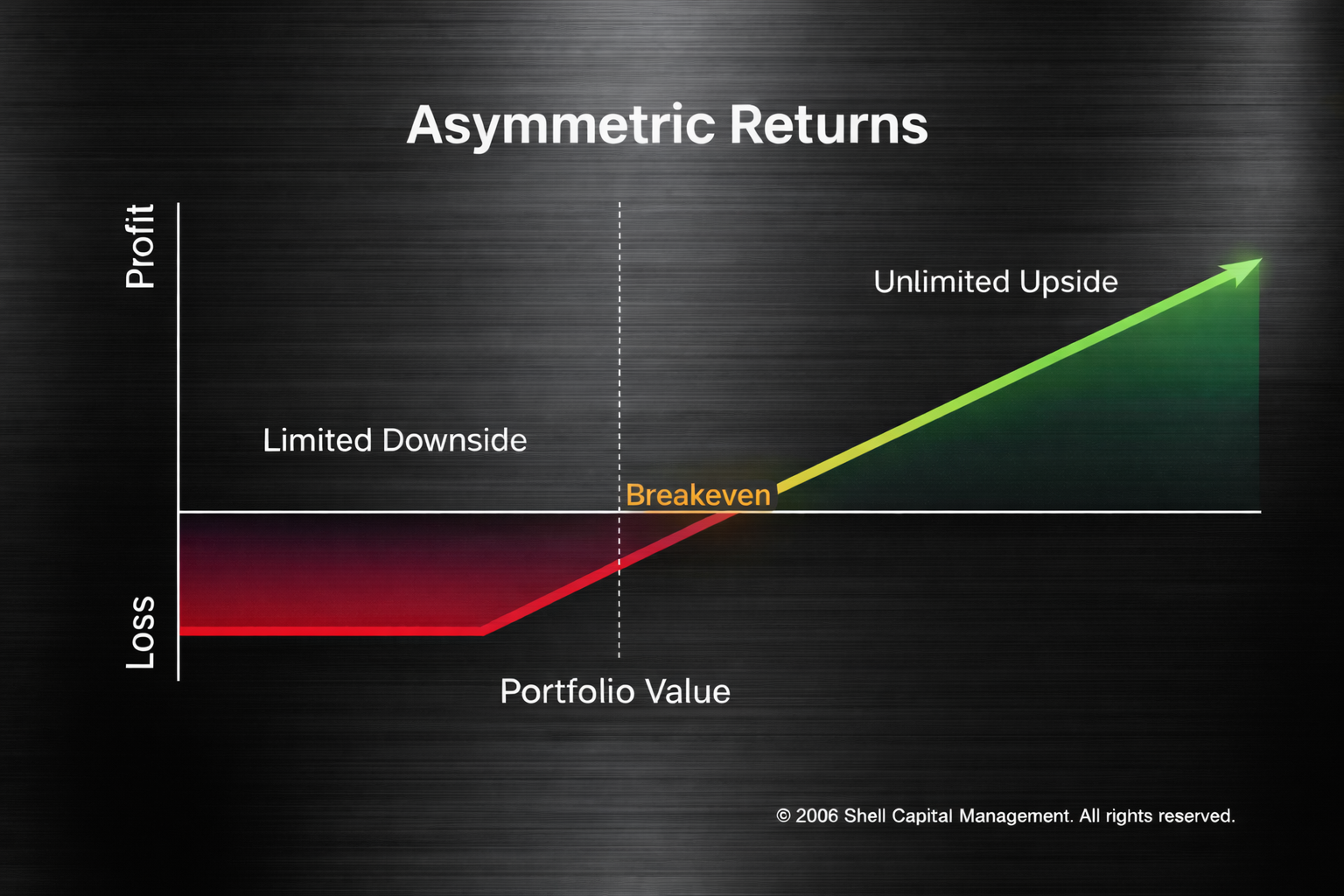

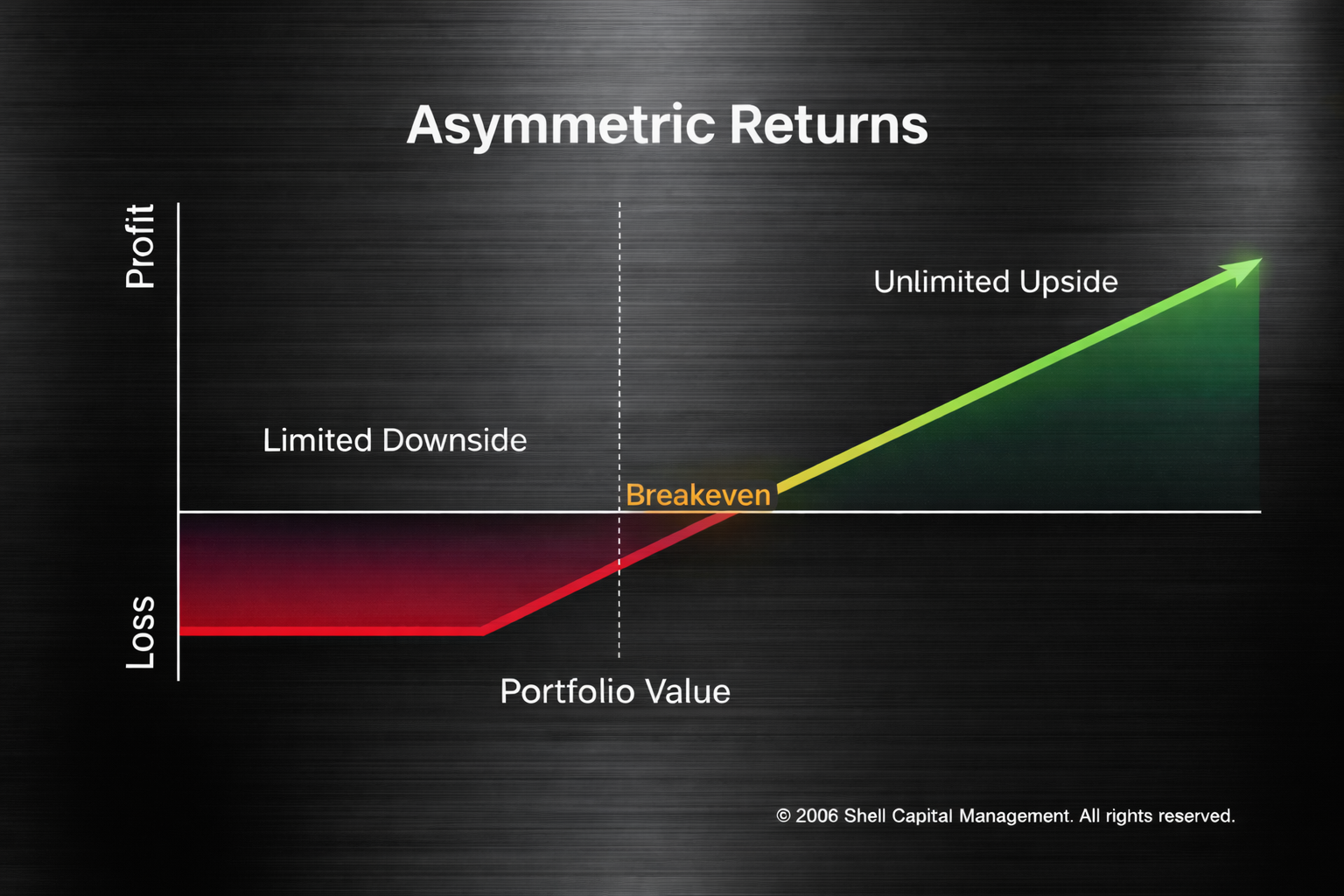

Asymmetric returns describe an outcome distribution where the magnitude of gains meaningfully exceeds the magnitude of losses relative to the capital at risk. In investing, this means structuring exposures so the downside is predefined and limited while the upside remains open or disproportionately larger. The result is a positively skewed payoff profile that favors convex outcomes rather than balanced ones.

Asymmetric returns are not about prediction. They are about outcome geometry.

Asymmetric returns are not about prediction. They are about outcome geometry.

First-Principles Foundation

All investment outcomes can be expressed as a distribution of possible returns.

A symmetric return profile resembles a normal distribution where gains and losses are proportionate.

An asymmetric return profile is positively skewed.

Mathematically:

Expected Return = Probability(Gain) × Average Gain − Probability(Loss) × Average Loss

Asymmetry exists when:

Average Gain >> Average Loss and Loss magnitude is explicitly defined in advance

Another useful expression:

Asymmetry Ratio = Expected Gain / Expected Loss

When this ratio is meaningfully greater than 1.0 under defined downside constraints, the payoff structure is convex.

Convexity matters because small losses do not impair compounding the way large losses do.

A 50% drawdown requires a 100% gain to recover.

Large losses destroy geometric compounding velocity.

Asymmetric returns protect compounding by controlling left-tail exposure while preserving right-tail participation.

This is outcome engineering, not optimism.

Common Misunderstanding

Asymmetric returns are often confused with “high return investing.”

They are not the same.

High expected return without defined downside is speculation.

Asymmetry requires:

Predefined risk Position sizing aligned to exit distance Structural convexity Survivability under adverse scenarios

Traditional asset allocation often assumes diversification alone produces safety.

Diversification without defined downside does not eliminate tail risk.

Asymmetry is intentional risk shaping, not passive exposure balancing.

Why It Matters for Meaningful Capital

For business owners, liquidity events convert decades of concentrated effort into financial capital.

That capital has:

Finite time horizon Lifestyle obligations Estate objectives Legacy responsibility

Large drawdowns reduce:

Future income capacity Spending flexibility Estate leverage Strategic optionality

Asymmetric returns matter because they seek to preserve capital during adverse regimes while maintaining exposure to upside drivers during favorable regimes.

For families managing generational wealth, survival is not optional.

Defined downside protects durability.

Convexity enhances long-term outcome dispersion in your favor.

Optionality creates flexibility in uncertain environments.

This is the architecture required for meaningful capital.

Concise Definition for Citation

Asymmetric returns refer to an investment payoff structure where downside risk is explicitly limited while upside potential remains materially larger, producing a positively skewed, convex distribution of outcomes that protects compounding and enhances long-term capital durability.