Why Beneficiary Designations Deserve Regular Review

Some of the most significant wealth transfer decisions are controlled by forms families completed years earlier.

Private Wealth Strategist is where Christi Shell, Certified Wealth Strategist®, shares insights from her work advising business owners, physicians, executives, and families responsible for meaningful capital.

Families with complex financial lives eventually face a consistent set of wealth decisions—how to structure a business exit, how to reduce tax drag, how to protect assets from liability, how to generate retirement income, how to transfer wealth efficiently to heirs, and how to support family, philanthropic, and legacy goals.

Private Wealth Strategist explores those issues through the lens of integrated wealth strategy. Articles address topics such as investment strategy and portfolio management, tax planning, risk management and insurance, asset protection structures, executive compensation and stock options, business succession planning, education and family support, charitable giving strategies, retirement planning, estate distribution, and liquidity or credit management.

Rather than treating these decisions in isolation, Private Wealth Strategist examines how they interact—because the structure of one decision often shapes the outcome of another.

Christi Shell serves as Managing Director and Private Wealth Strategist at Shell Capital Management, LLC.

Some of the most significant wealth transfer decisions are controlled by forms families completed years earlier.

Postponing estate and protection planning may reduce flexibility and increase the likelihood of operational, legal, and family complications later.

Probate is an administrative process. Estate planning is a much broader discipline.

A trust structure is only as effective as the people responsible for administering it.

Many wealth disruptions occur when multiple risks converge simultaneously.

Medical uncertainty becomes harder when families lack documented guidance.

Authority that is not documented before incapacity may require court intervention later.

Wanting a business to remain in the family or with current partners is not the same as having an executable succession plan.

Many families use the terms interchangeably even though the programs operate very differently.

Some of the largest enterprise risks are attached to people, not property.

Most protection strategies become less effective once a legal threat is already visible.

The need for disability planning is real, even when the insurance market does not fully replace a client’s lifestyle.

The policy structure should follow the planning objective. It should never be selected in isolation from the problem it is meant to address.

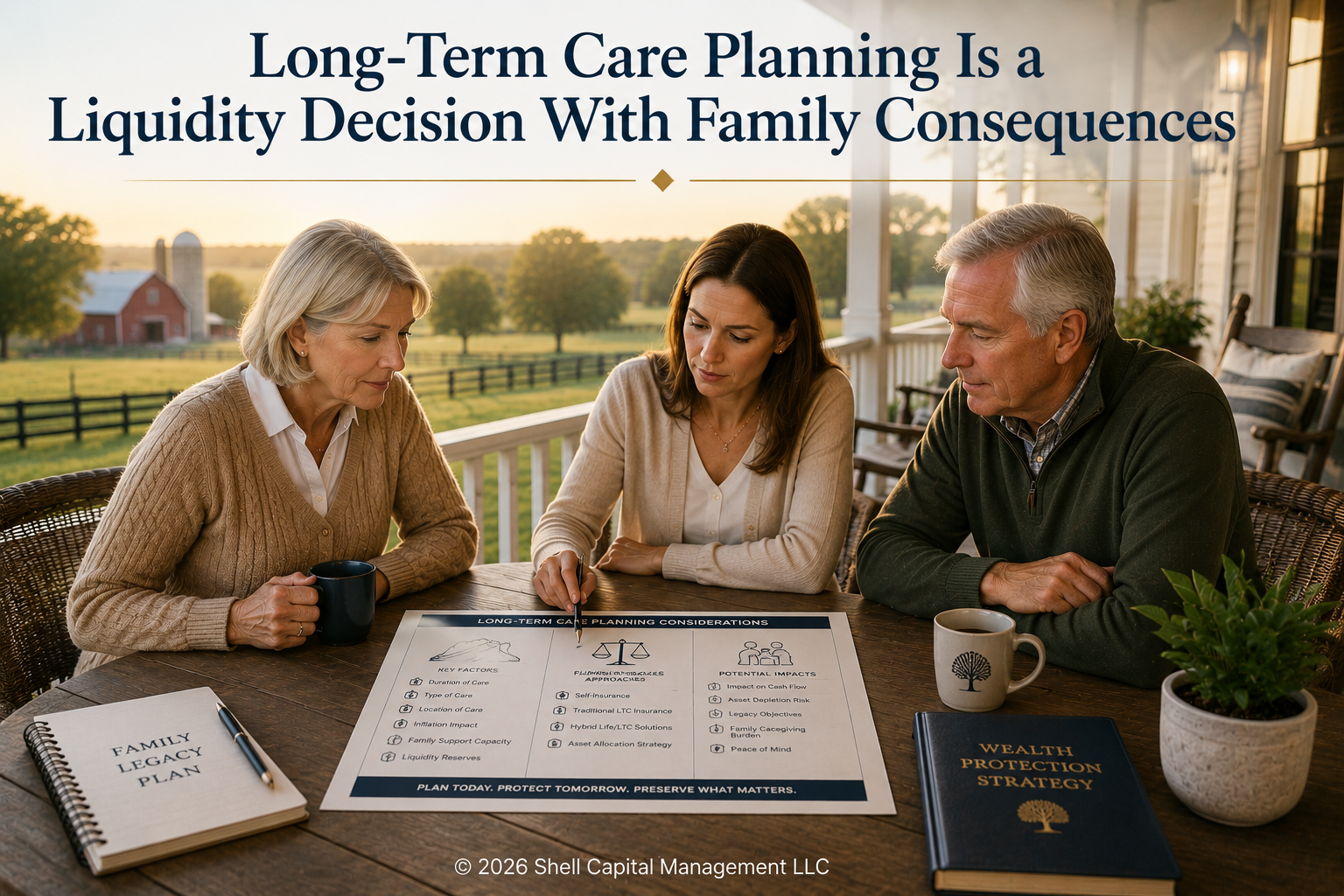

The central long-term care question is not simply whether insurance is needed. It is how the family intends to fund care without disrupting everything else.

A policy can remain fully in force and still fail its purpose if the beneficiary and ownership structure no longer align with the plan.

A sophisticated insurance strategy is only as durable as the assumptions supporting it.

A trust only functions as intended when assets, governance, and implementation remain aligned.

The planning window for incapacity often closes earlier than families expect.

As assets, activities, and visibility grow, the map of potential liability tends to expand as well.

Convenience and simplicity often drive joint ownership decisions, but long-term implications deserve closer review.