Tax-Aware Withdrawal Strategy in Retirement Planning

Retirement income planning is often framed around how much to withdraw.

Less attention is given to where those withdrawals come from.

That distinction matters.

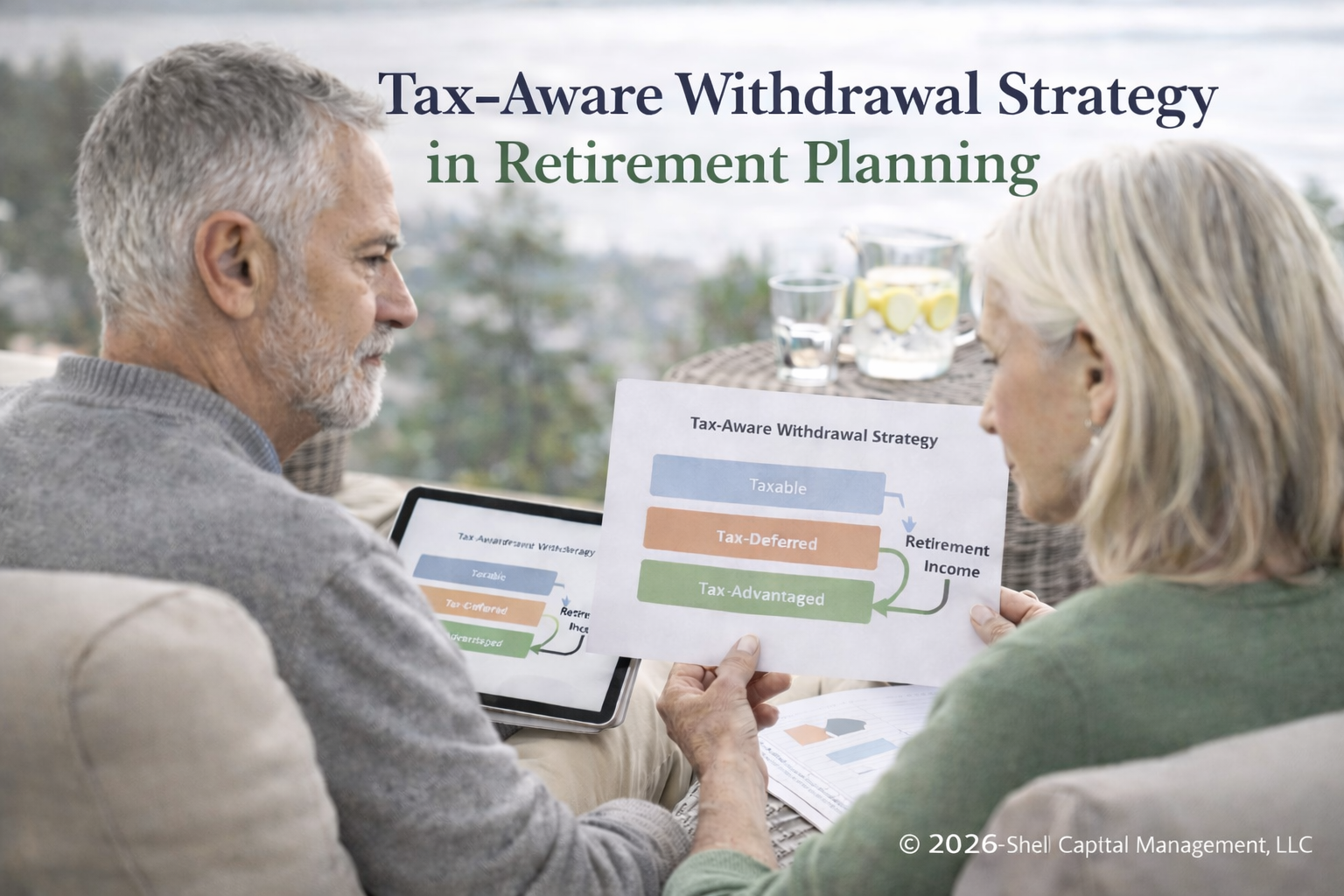

Most portfolios include a mix of taxable accounts, tax-deferred accounts, and tax-advantaged structures. Each carries different tax characteristics. The sequencing of withdrawals across these accounts can materially affect long-term outcomes.

The common mistake is defaulting to a static withdrawal approach. For example, drawing proportionally from all accounts without regard to tax structure.

This approach can create inefficiencies.

Withdrawals from tax-deferred accounts may increase taxable income in a given year. Taxable accounts may offer more flexibility in timing. Tax-advantaged accounts may be more valuable if preserved for later stages.

The interaction between these accounts is dynamic. It changes with income levels, tax policy, and distribution requirements.

A tax-aware approach focuses on coordination rather than optimization in a single year. The objective is to manage lifetime tax exposure while preserving flexibility.

This requires aligning withdrawal strategy with broader planning considerations, including estate design and future income needs.

For physicians, founders, and executives, large tax-deferred balances and deferred compensation structures can amplify this issue.

Without coordination, withdrawals can create unintended tax concentration in certain years, reducing overall efficiency.

Withdrawal strategy is not a mechanical process. It is part of a broader system that connects portfolio structure, tax exposure, and long-term planning objectives.

Managing that system requires ongoing evaluation, not one-time decisions.

Written by Christi Shell, CWS®, AAMS®, BFA™, CETF®, Managing Director and Private Wealth Strategist at Shell Capital Management, LLC.

To speak with Christi about your financial situation, request a private consultation.

Shell Capital Management, LLC is a registered investment adviser. This material is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Advisory services are only offered to clients or prospective clients where Shell Capital Management, LLC is properly registered or exempt from registration. Any views are as of the date published and may change. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.