Optionality in Retirement Planning: Preserving Flexibility Over Time

Retirement planning benefits from flexibility. Preserving optionality allows for better decisions as conditions evolve.

Private Wealth Strategist is where Christi Shell, Certified Wealth Strategist®, shares insights from her work advising business owners, physicians, executives, and families responsible for meaningful capital.

Families with complex financial lives eventually face a consistent set of wealth decisions—how to structure a business exit, how to reduce tax drag, how to protect assets from liability, how to generate retirement income, how to transfer wealth efficiently to heirs, and how to support family, philanthropic, and legacy goals.

Private Wealth Strategist explores those issues through the lens of integrated wealth strategy. Articles address topics such as investment strategy and portfolio management, tax planning, risk management and insurance, asset protection structures, executive compensation and stock options, business succession planning, education and family support, charitable giving strategies, retirement planning, estate distribution, and liquidity or credit management.

Rather than treating these decisions in isolation, Private Wealth Strategist examines how they interact—because the structure of one decision often shapes the outcome of another.

Christi Shell serves as Managing Director and Private Wealth Strategist at Shell Capital Management, LLC.

Retirement planning benefits from flexibility. Preserving optionality allows for better decisions as conditions evolve.

Healthcare costs are one of the largest unknowns in retirement. Planning requires flexibility, not fixed assumptions.

Inflation does not need to be extreme to create long-term damage. Even moderate increases can materially affect retirement income.

For business owners, retirement planning is not just accumulation—it is conversion from illiquid enterprise value to usable capital.

Income decisions during retirement directly affect estate outcomes. Coordination is essential to preserve efficiency and intent.

Behavioral risk increases in retirement as income depends on portfolio performance. Decision-making under stress becomes a central risk factor.

The transition into retirement requires intentional liquidity staging to support income and preserve flexibility.

Reducing volatility does not eliminate risk. In retirement, excessive conservatism can create its own form of instability.

Income in retirement does not come from a single source. It is the result of a coordinated system designed to manage uncertainty.

Withdrawal strategy is not just about timing. It is about coordinating across account structures to manage long-term tax exposure.

Wealth built through concentration often enters retirement unchanged. Without adjustment, that concentration can create fragility.

The first years of retirement are structurally fragile. Market declines combined with withdrawals can reshape long-term outcomes.

Living longer increases uncertainty. Retirement plans must be built to adapt over extended time horizons.

Estimating retirement income needs is only a starting point. The gap between resources and spending changes over time.

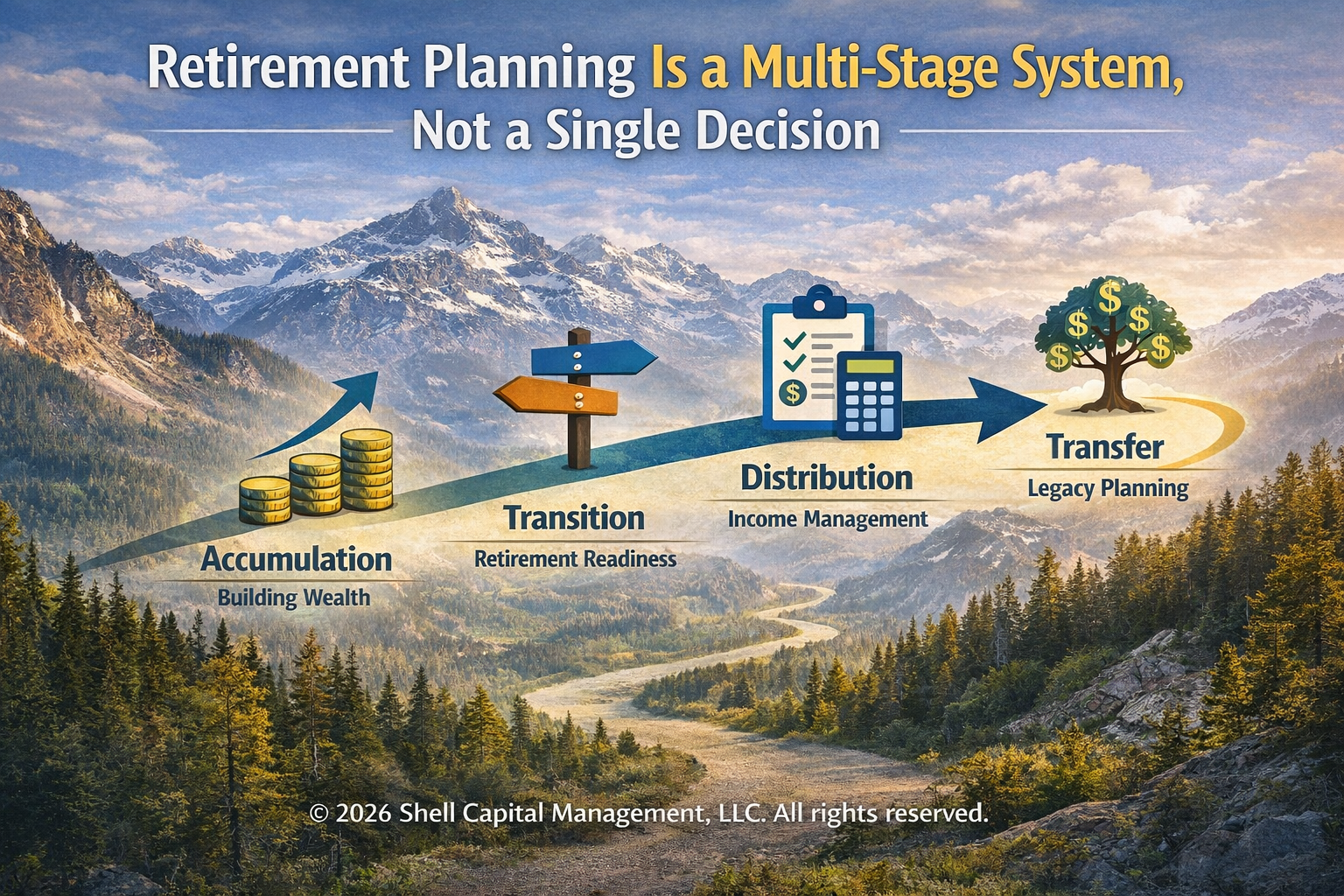

Retirement is not a single event. It is a staged process that requires coordination across time, liquidity, and decision-making.

Not all retirement withdrawals are taxed the same. In 2026, understanding Roth ordering rules and conversion strategy is essential.

This blog will share tips for women entrepreneurs navigating both running their business and saving for retirement.

This blog is about what temporary retirement means, the potential benefits, and some financial planning considerations of taking a career break.

This blog will share some of the biggest insights from the 2024 EBRI Retirement Confidence Survey.

financial advisor for retirement planning for freelancers and self-employed, including the different plan options and some tips to help freelancers save for retirement.