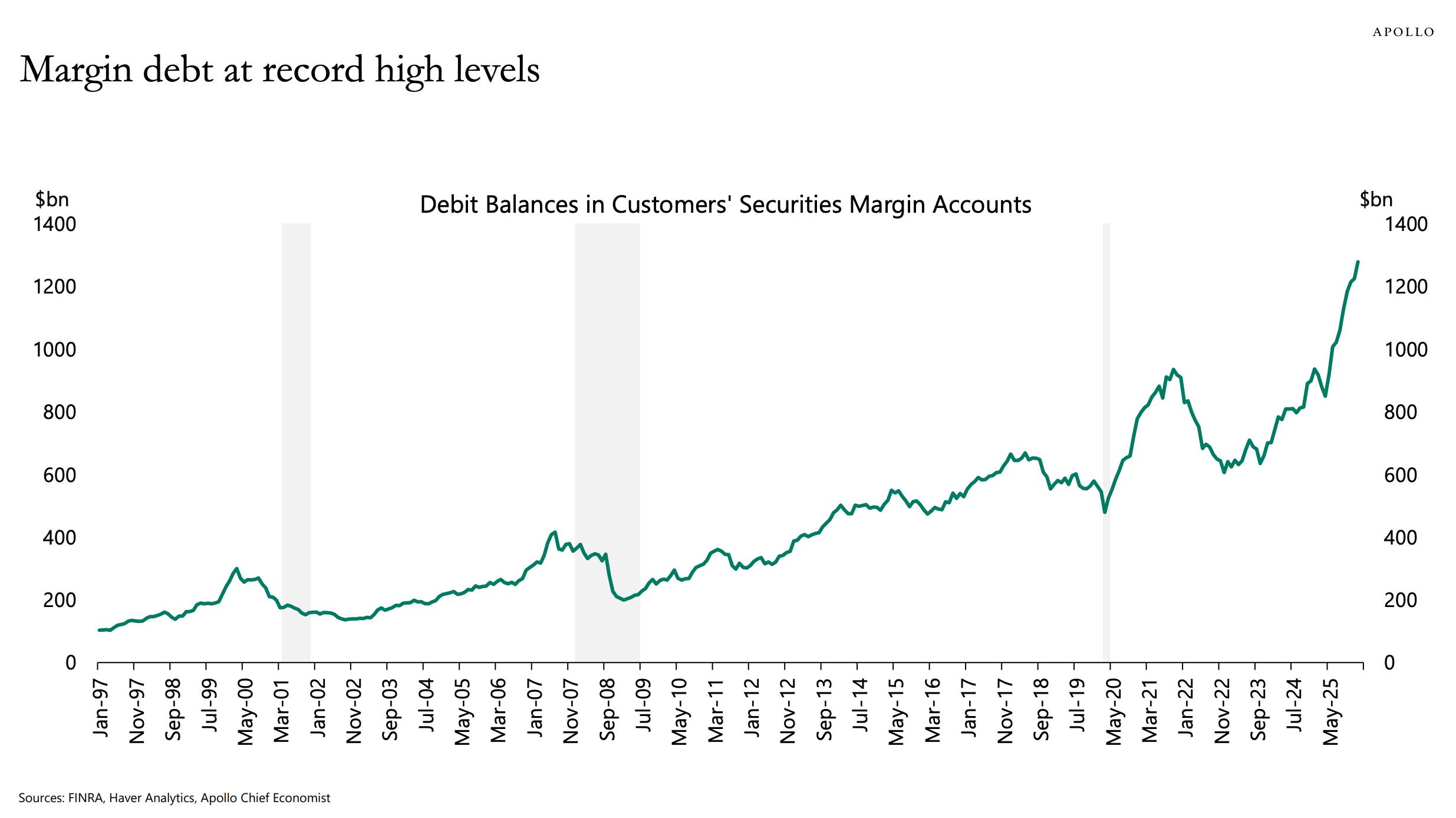

The Market’s Leverage Trap: When Borrowed Confidence Becomes Forced Selling

Record margin debt isn’t automatically bearish. The risk appears when borrowed buying power, a thin cash cushion, and falling collateral values meet at the same time.

Record margin debt isn’t automatically bearish. The risk appears when borrowed buying power, a thin cash cushion, and falling collateral values meet at the same time.

This market isn't only an AI story. It's an earnings-dependency story. Prices can keep rising if forward earnings keep confirming the move, but once that confirmation fades, portfolio risk can show up fast.

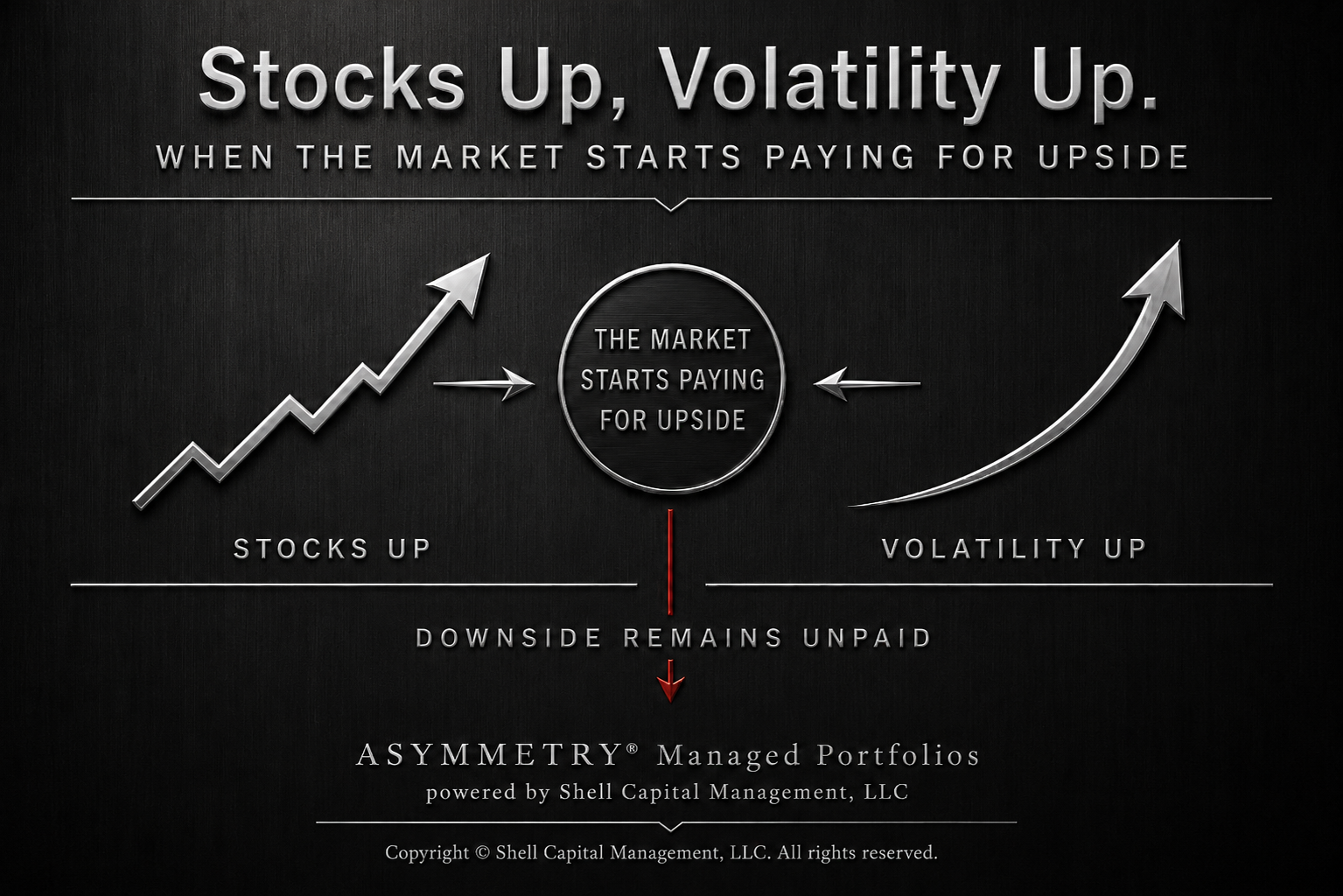

Stocks up, volatility up: When stocks rise and volatility rises too, the real tell is not VIX. The real tell is skew. If put skew steepens, the market may be advancing with protection underneath it. If skew flattens, investors may be chasing upside through calls after the move has already happened. That is not the seatbelt. That is the accelerator getting crowded.

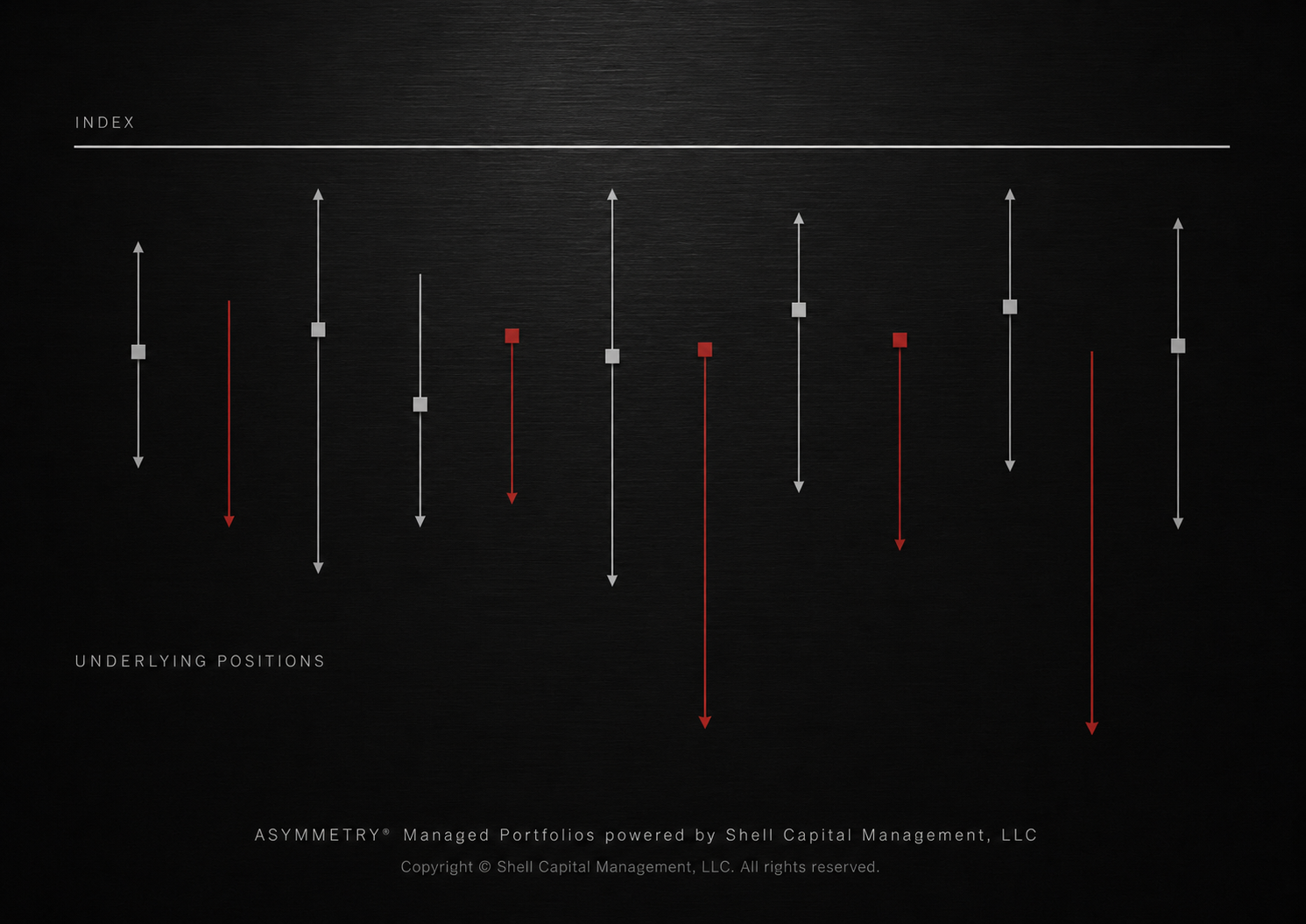

A quiet index doesn’t always mean a quiet market. Sometimes it means the violence underneath is cancelling itself out.

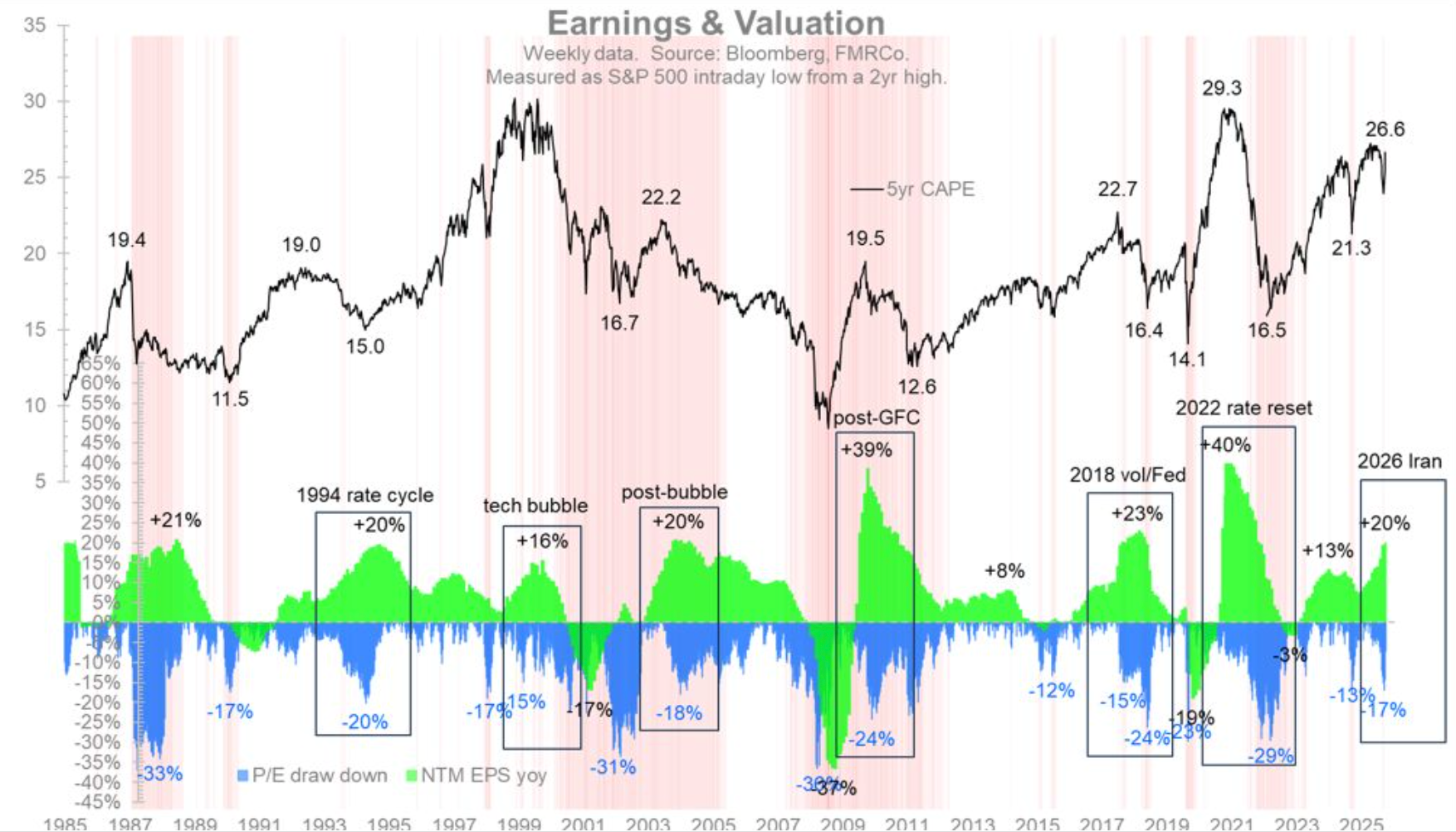

Price can decline without earnings breaking. When valuation compresses during earnings growth, the result isn’t just volatility—it’s a shift in the return distribution that can create asymmetric opportunity for disciplined portfolio management.

Oil gets the headline. Inventory is the structure underneath it. When the buffer disappears, price doesn’t have to move gradually. Risk becomes nonlinear.

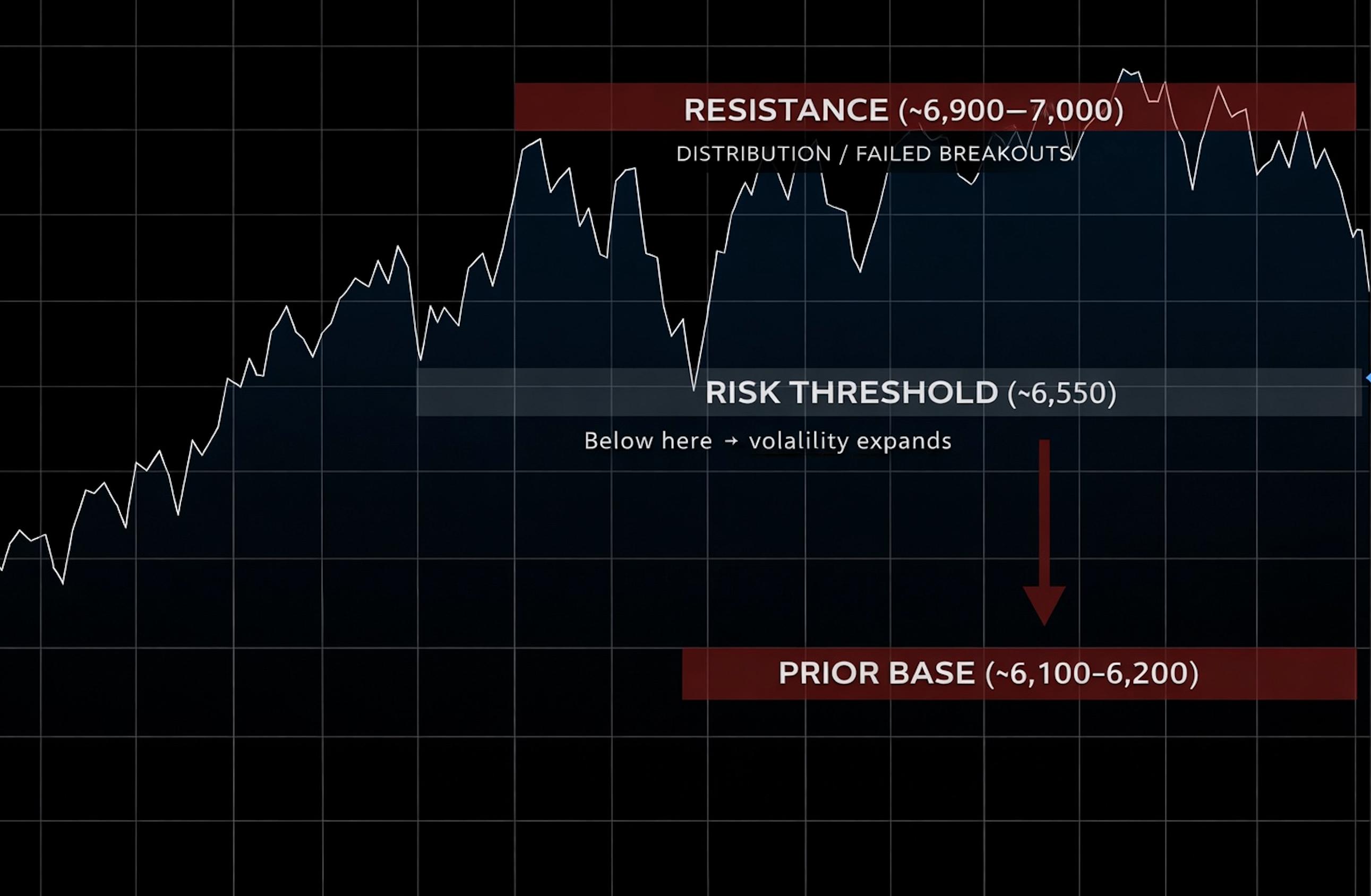

Markets don’t break gradually—they transition. The S&P 500 is approaching a key level near 6,550 where behavior shifts, volatility expands, and risk begins to compound. The difference isn’t direction—it’s what happens if you’re wrong.

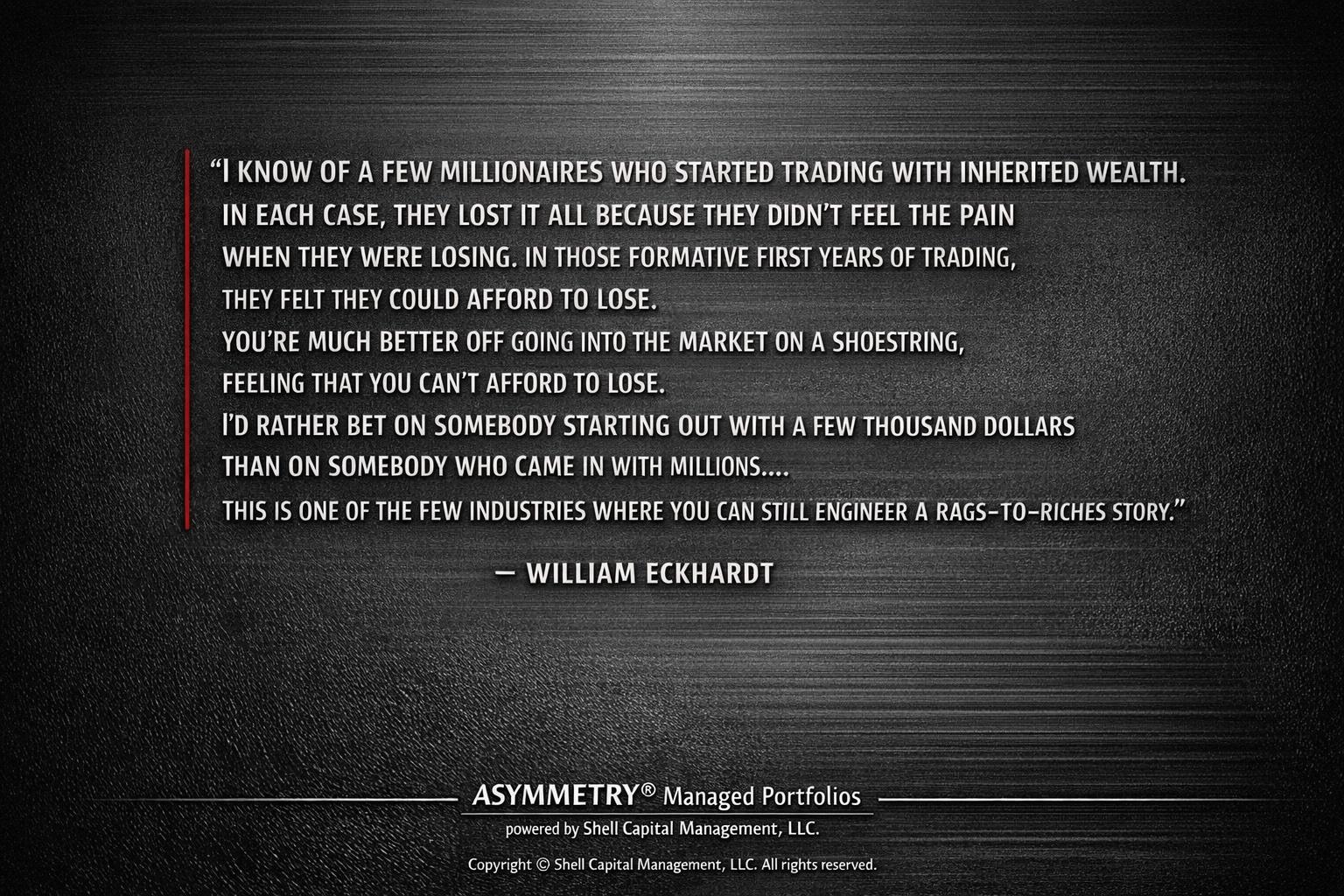

William Eckhardt’s warning is simple: people who don’t feel the pain of loss often lose everything. The real edge in investing isn’t starting with more capital. It’s building a process that defines downside before the market does.

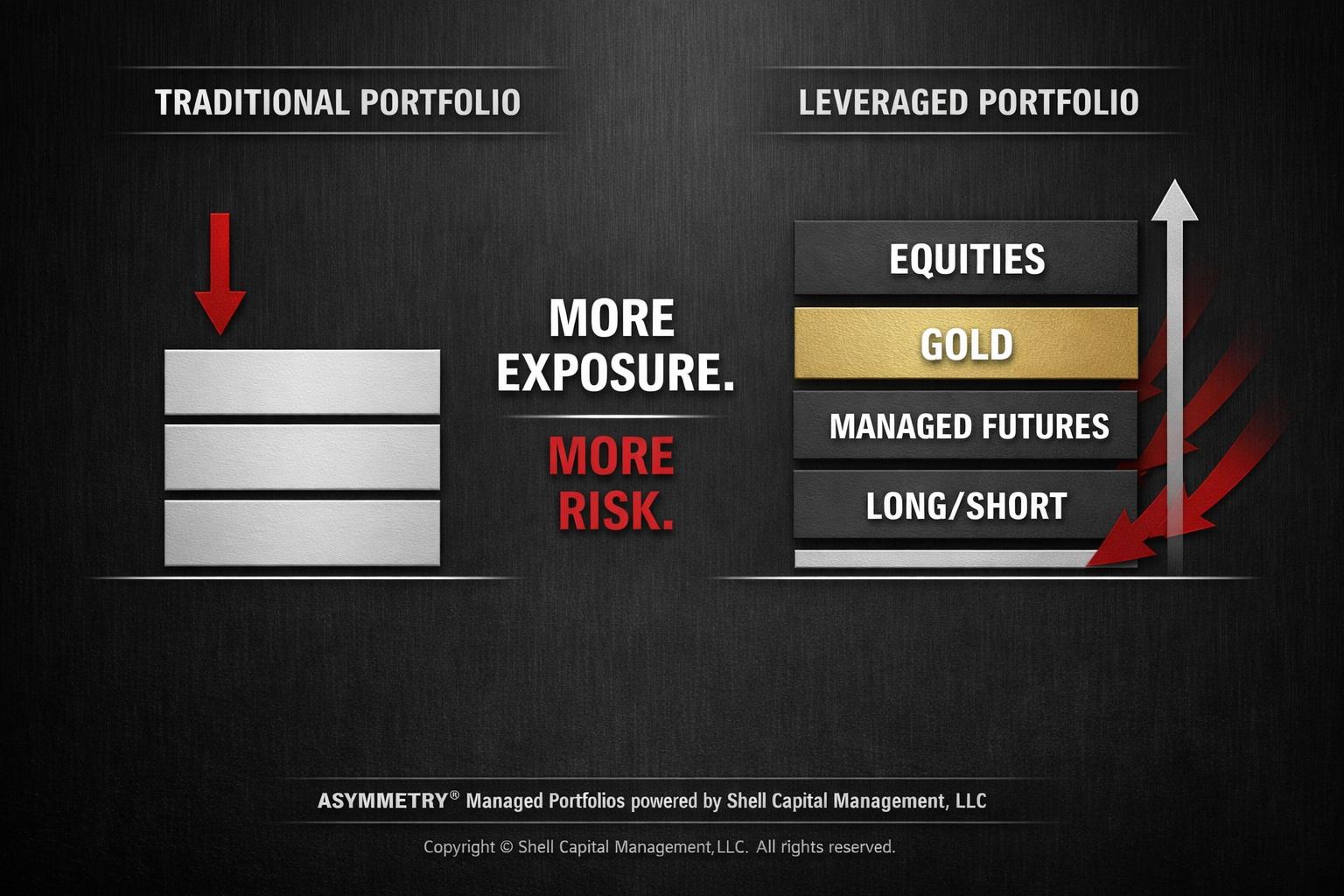

Capital efficiency expands exposure, but it also increases interaction risk. When stacked exposures move together, drawdowns accelerate and recovery math becomes more demanding.

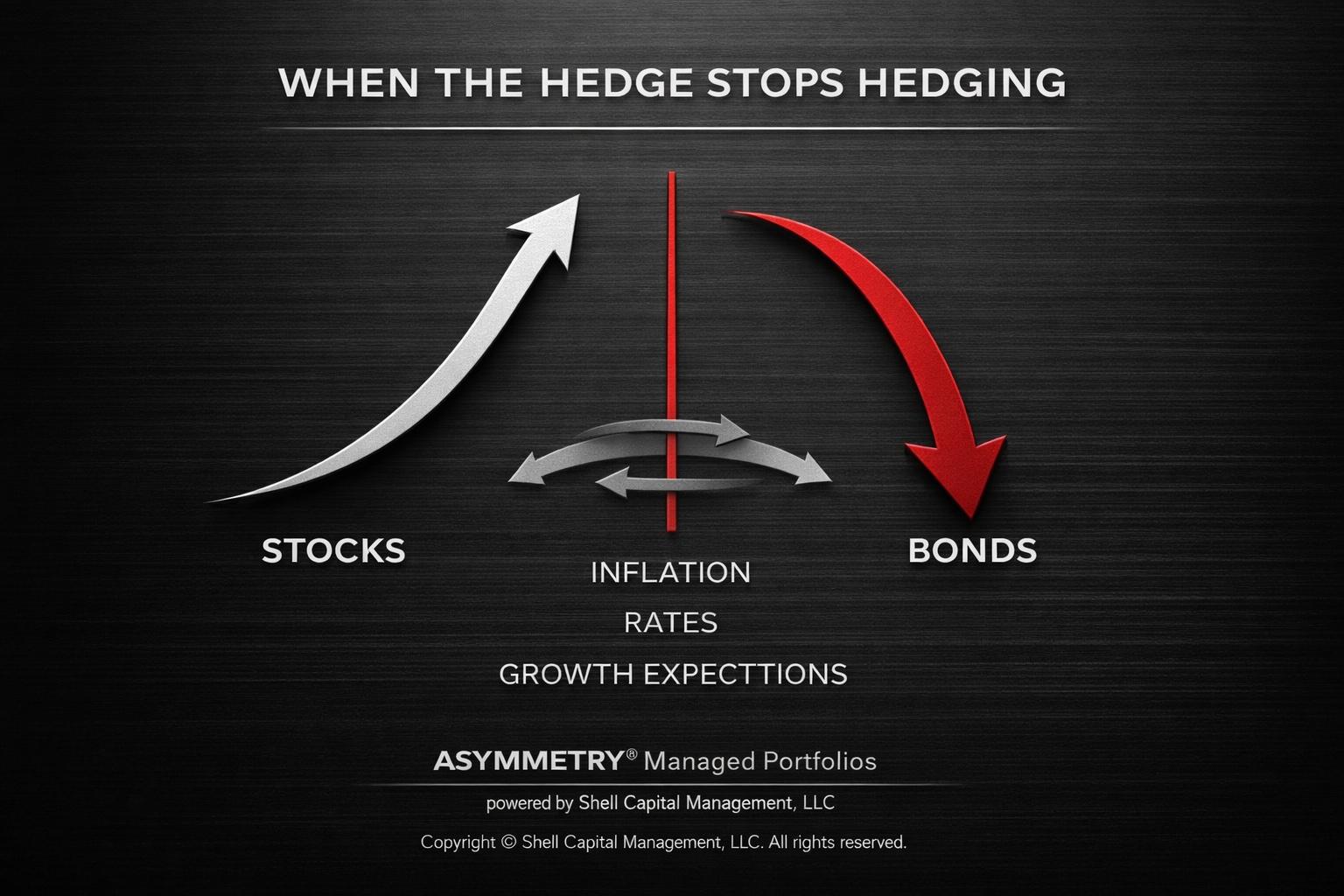

Many investors believe bonds protect them when equities fall. But in certain regimes, that relationship breaks down. When inflation, rates, and growth expectations pull markets in different directions, the hedge investors rely on may stop working.

Measurement doesn’t just track performance—it defines behavior. In portfolio management, what you measure becomes the incentive system driving risk, exposure, and outcomes.

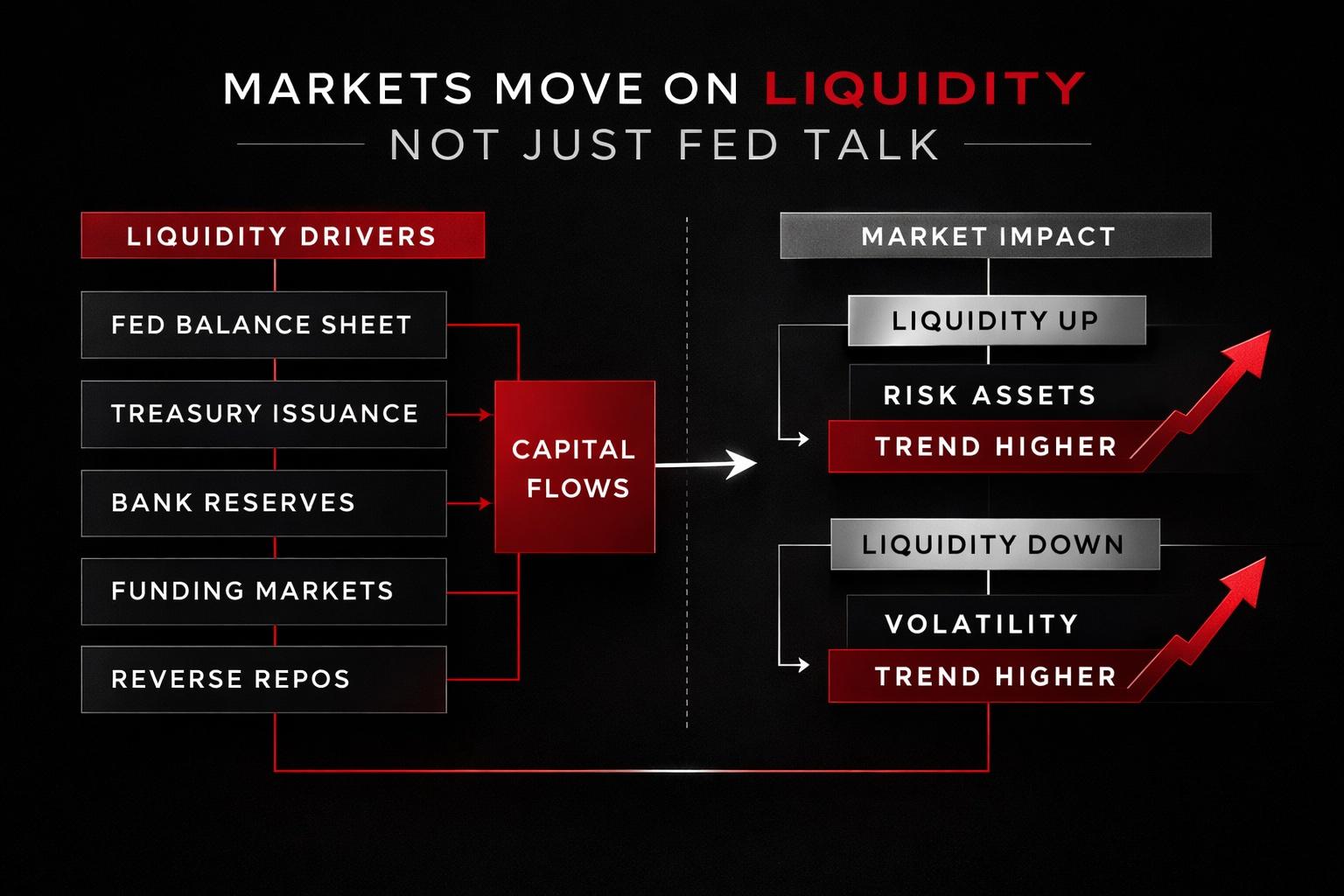

This week’s Fed meeting will dominate headlines. But markets often move less because of Powell’s words and more because of liquidity conditions—bank reserves, Treasury flows, and the availability of capital to buy risk assets. Understanding that distinction matters when managing portfolios through changing regimes.

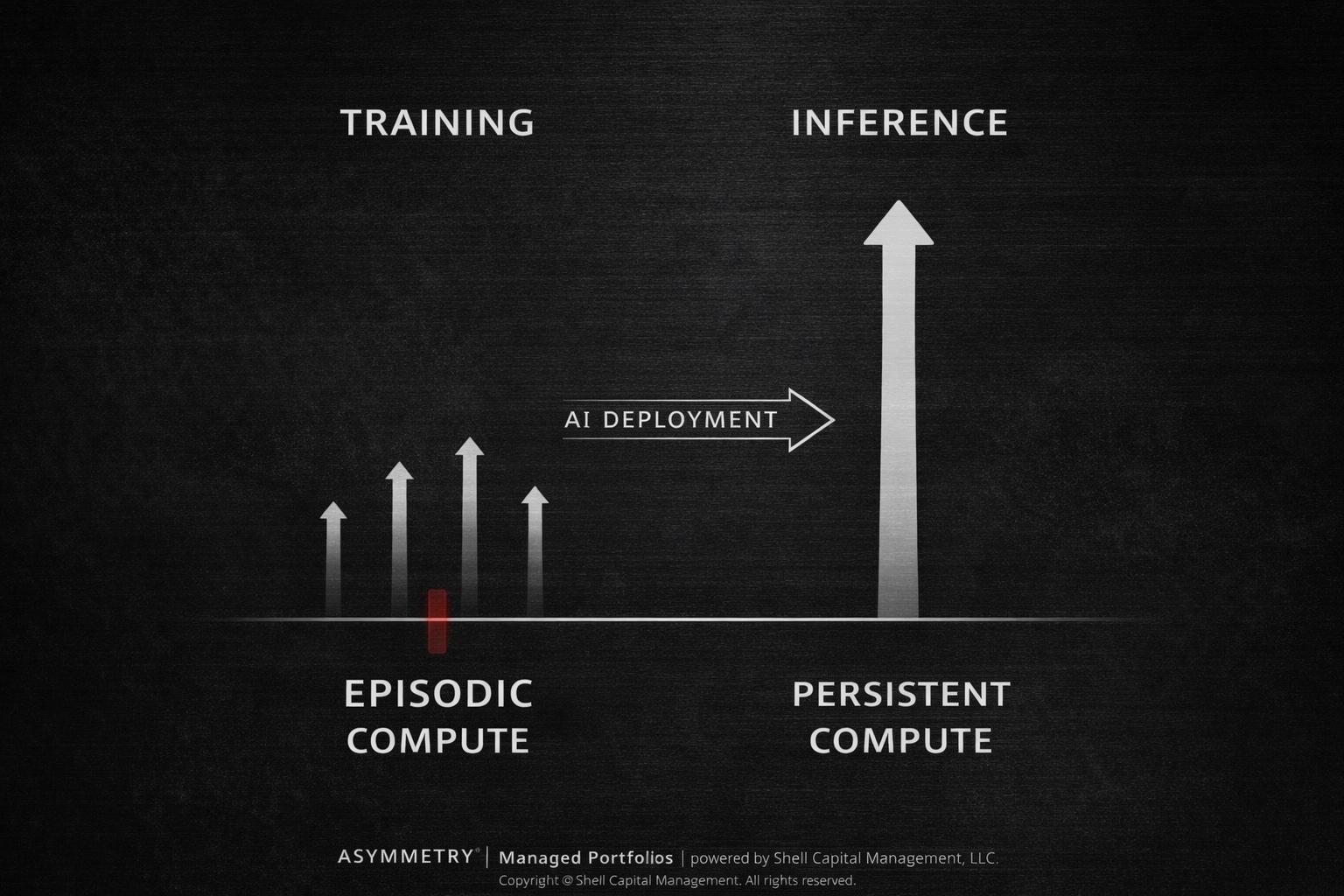

AI’s first wave was about training massive models. The next wave is about running them continuously. Nvidia’s push into inference infrastructure suggests the AI cycle may be shifting from episodic training bursts to persistent deployment across the economy.

Markets rarely break because of the headline everyone is watching. They tend to correct when valuations are stretched, liquidity tightens, and investors are positioned for the best outcome. That combination creates a fragile environment where downside risk expands faster than upside potential.

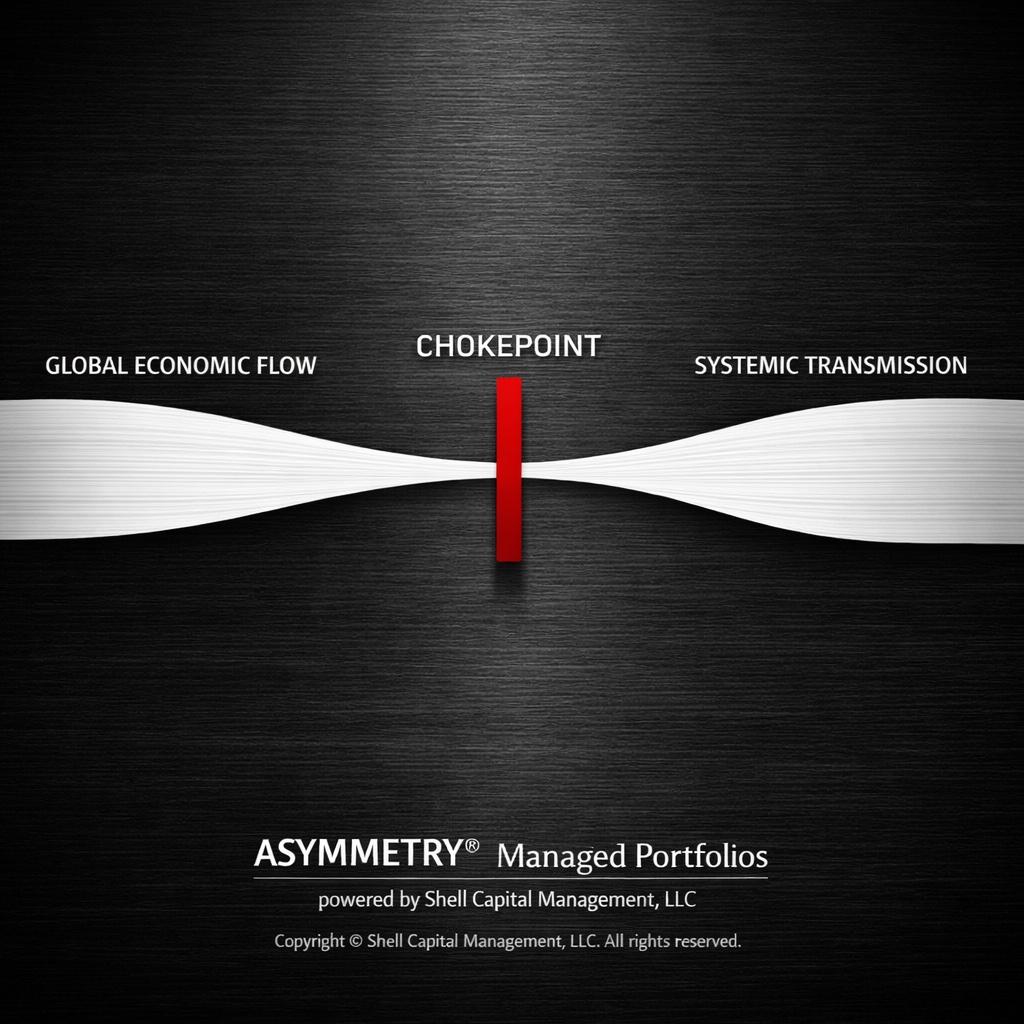

The global economy looks diversified. In reality, enormous economic flow passes through a few narrow geographic chokepoints. The Strait of Hormuz—just 21 miles wide—moves roughly 20% of the world’s oil supply, showing how small structural nodes can transmit outsized financial risk.

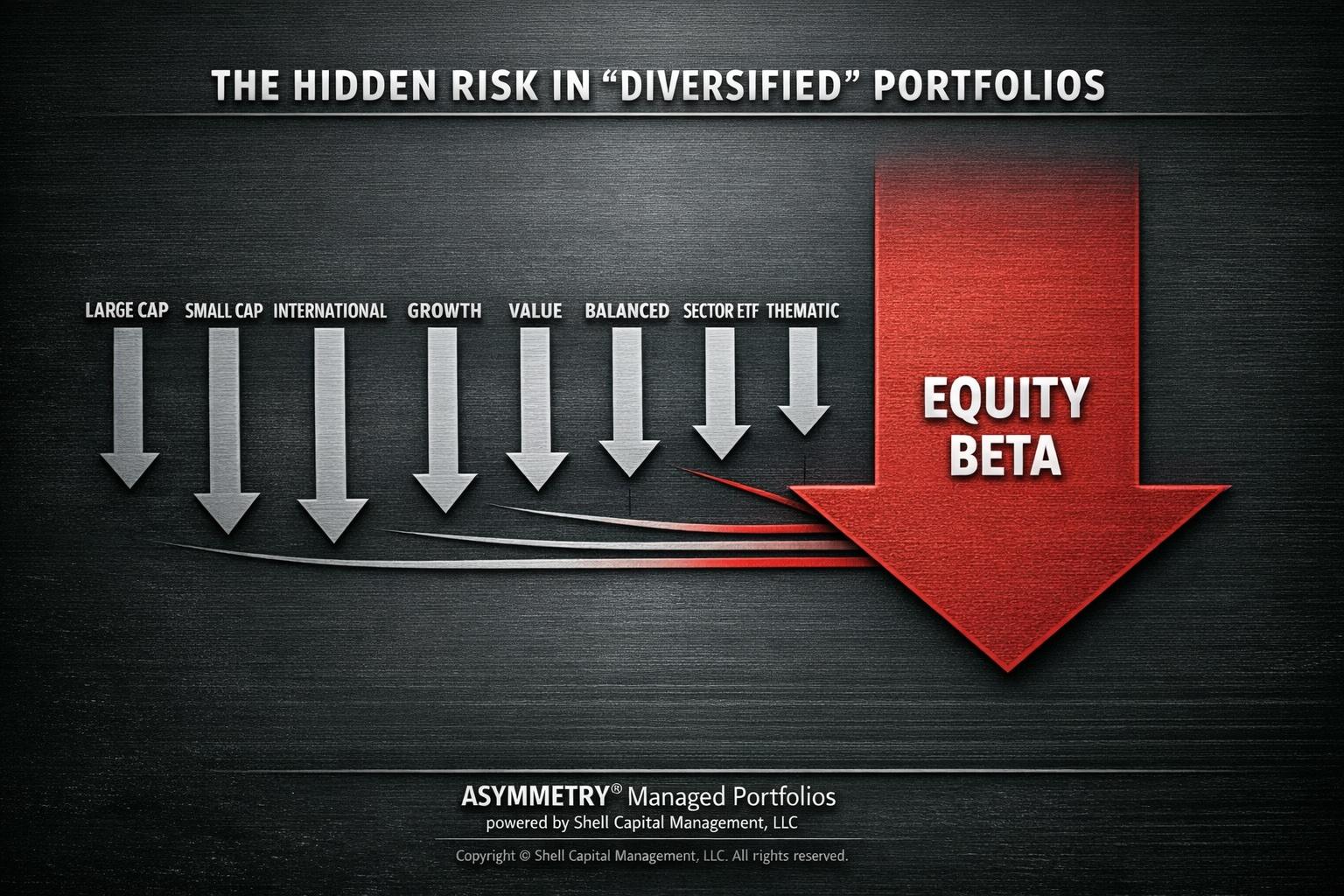

A portfolio can hold dozens of funds and still have a single dominant exposure. The hidden risk in many “diversified” portfolios is that the underlying return driver is the same.

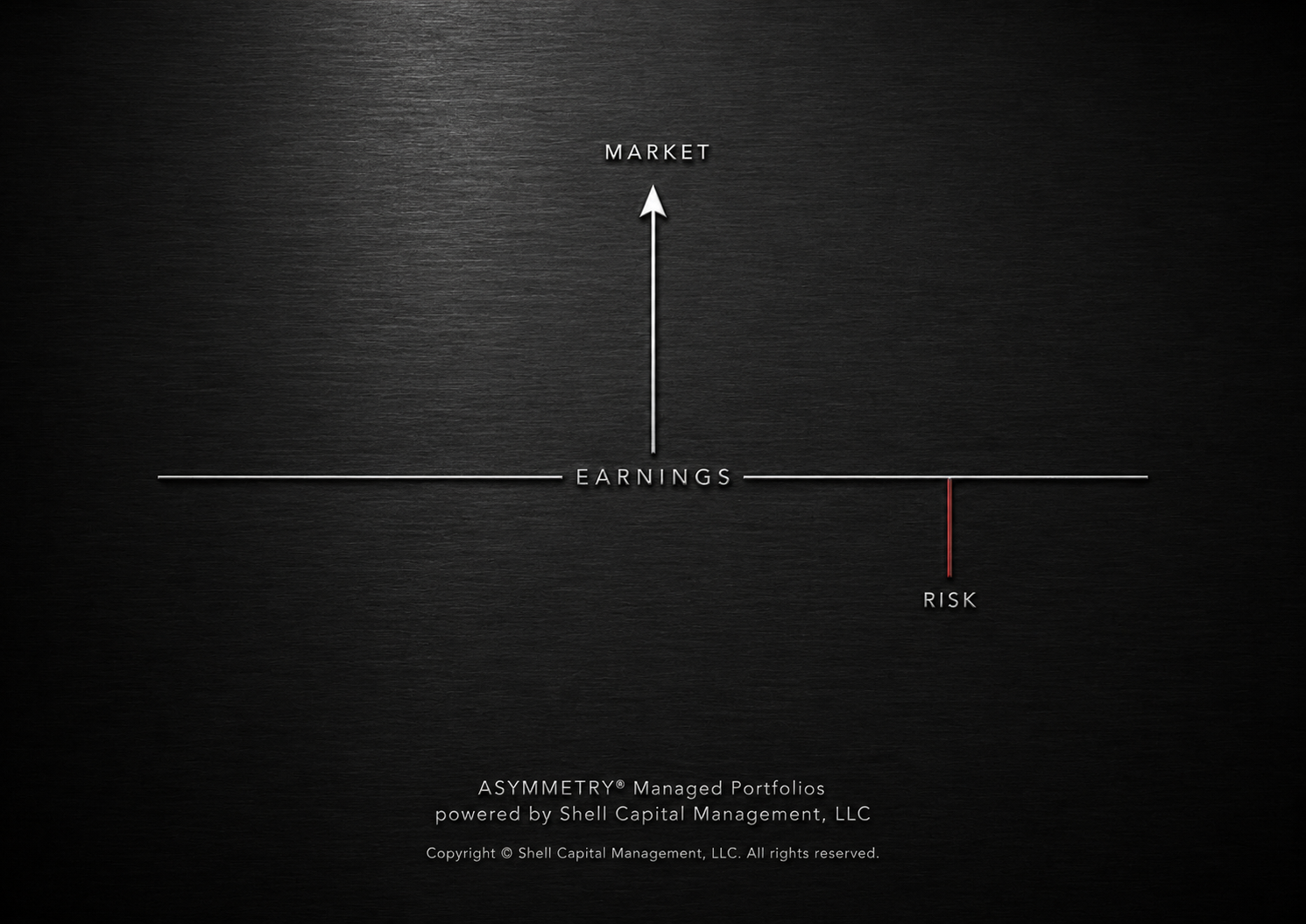

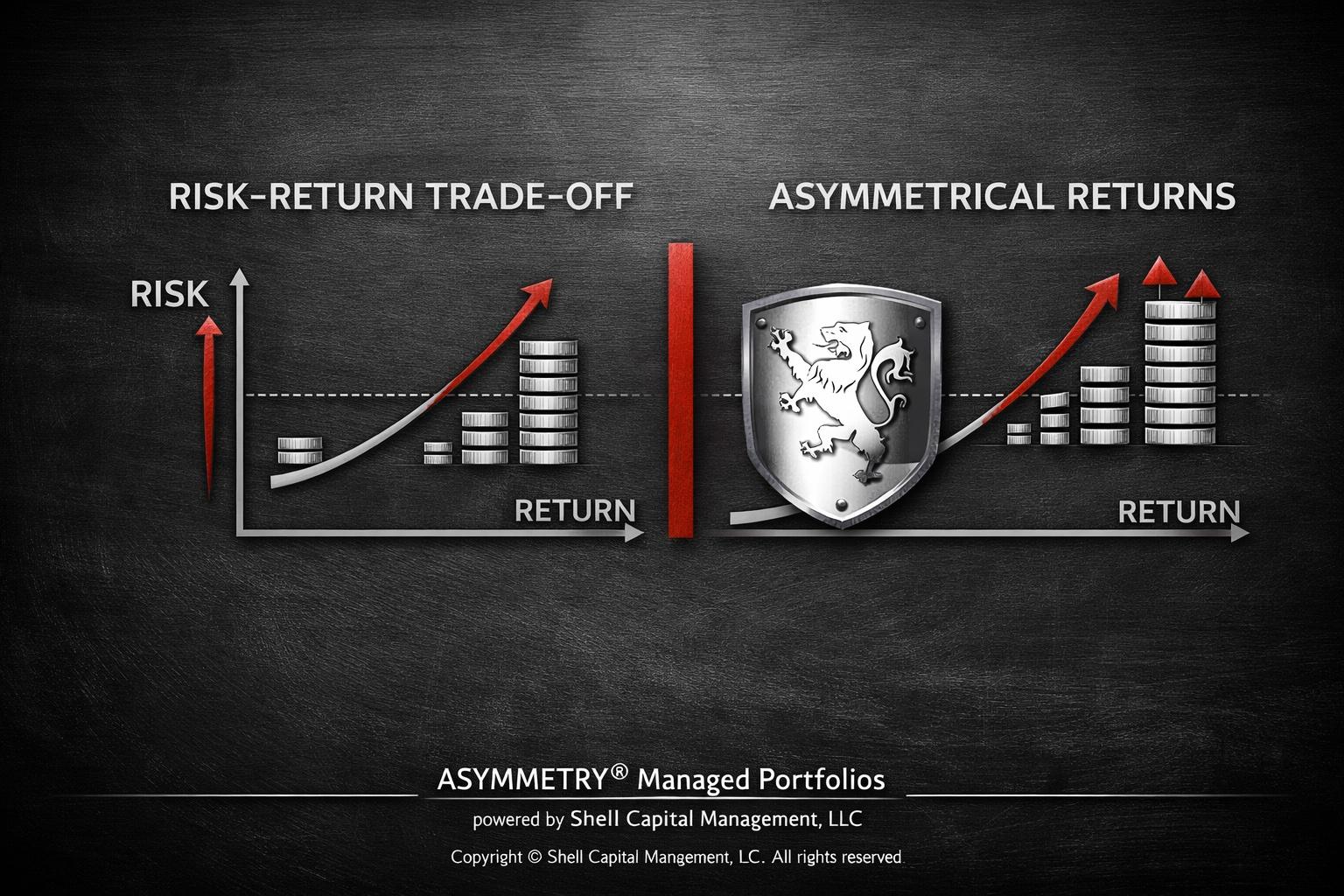

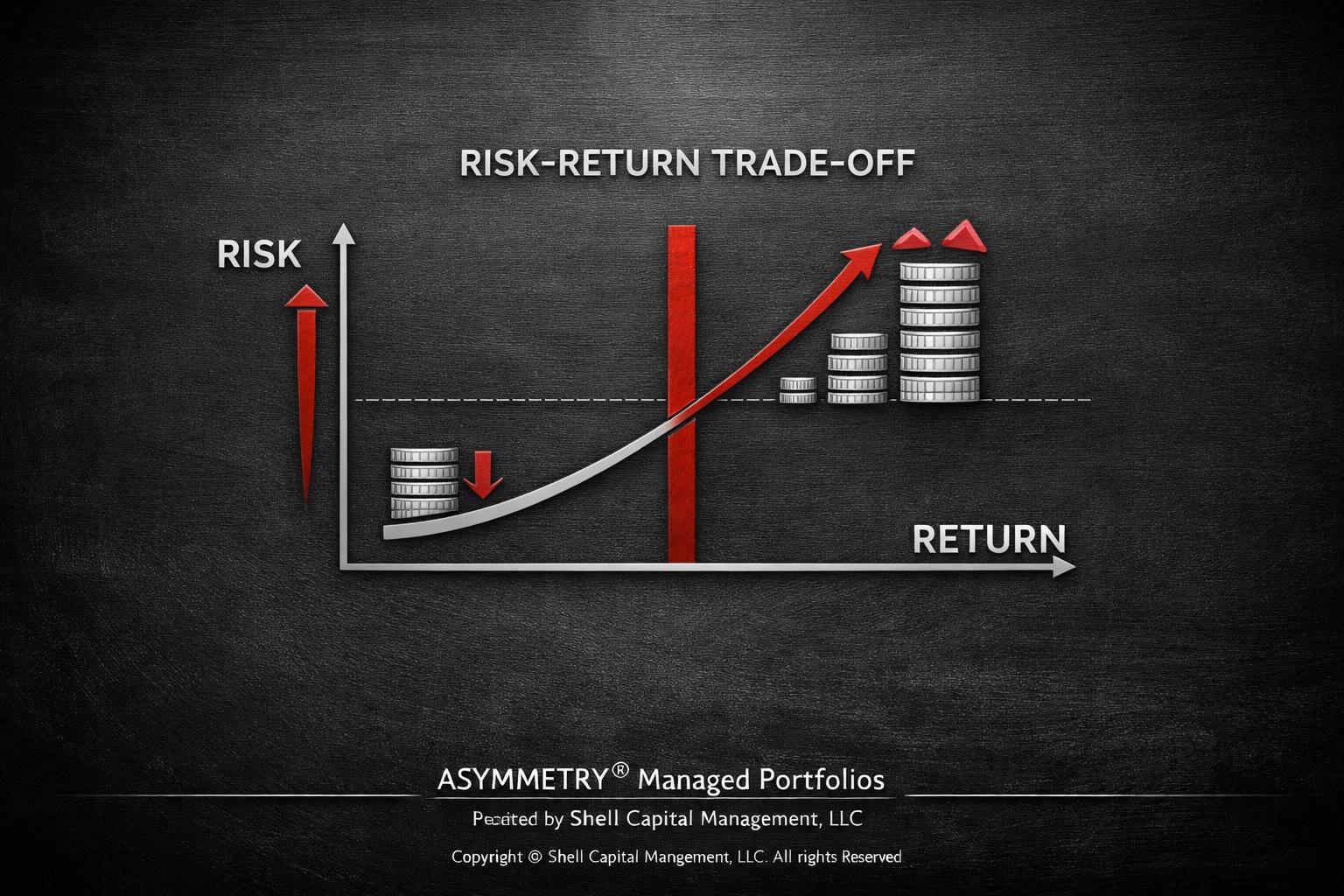

The risk–return trade-off is one of the most cited ideas in finance, but it’s also one of the most misunderstood. The framework correctly explains why returns exist—but it says very little about how intelligent investors structure those returns asymmetrically.

The risk–return trade-off is one of the most widely cited ideas in investing, but it’s often misunderstood. The real lesson isn’t that more risk guarantees higher returns. It’s that meaningful returns only exist where uncertainty exists—and the intelligent investor’s task is to structure that uncertainty asymmetrically.

When margin debt climbs to record highs, the real risk isn’t the leverage itself—it’s the forced selling that occurs when prices fall. Markets don’t decline in isolation. They decline through balance sheets.

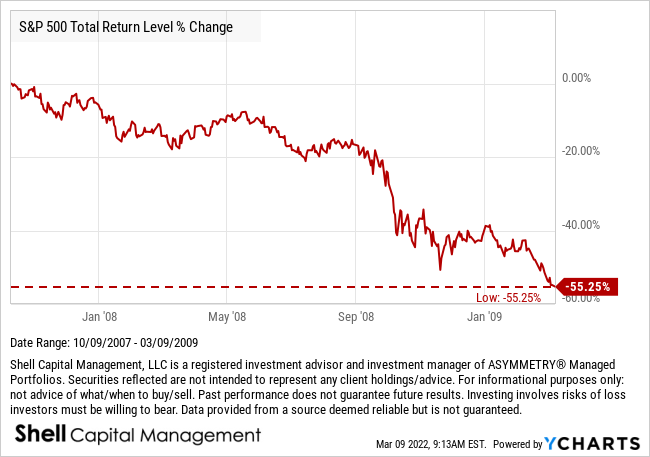

March 9, 2009 marked the end of the financial crisis bear market. But the deeper lesson isn’t the recovery that followed—it’s how investors and portfolio managers often stay positioned for the crisis that already happened.