VIX Term Structure: The Hidden Edge in Market Complacency

The VIX futures curve is sending a clear signal—one that’s easy to misread without a sharp eye.

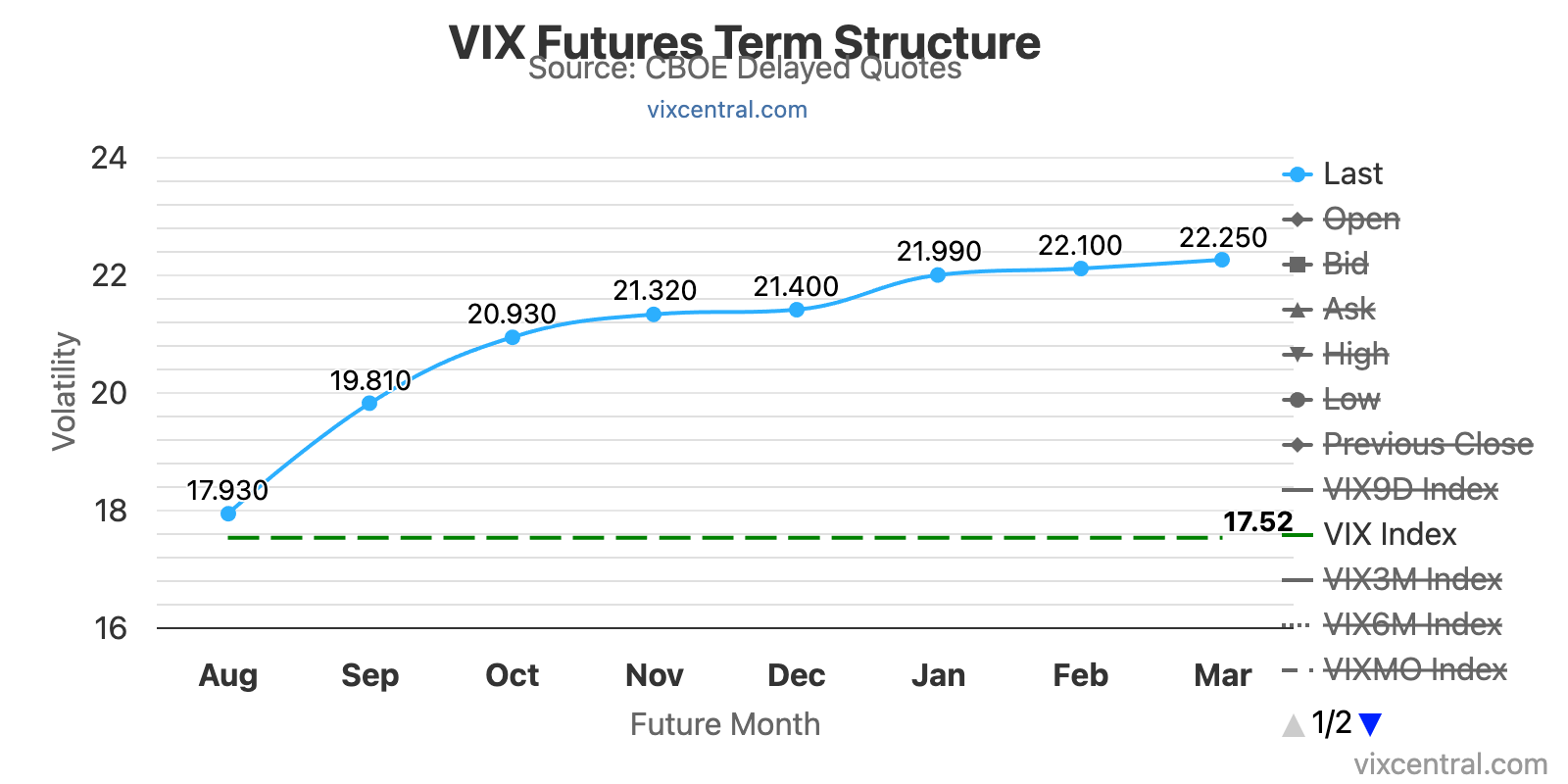

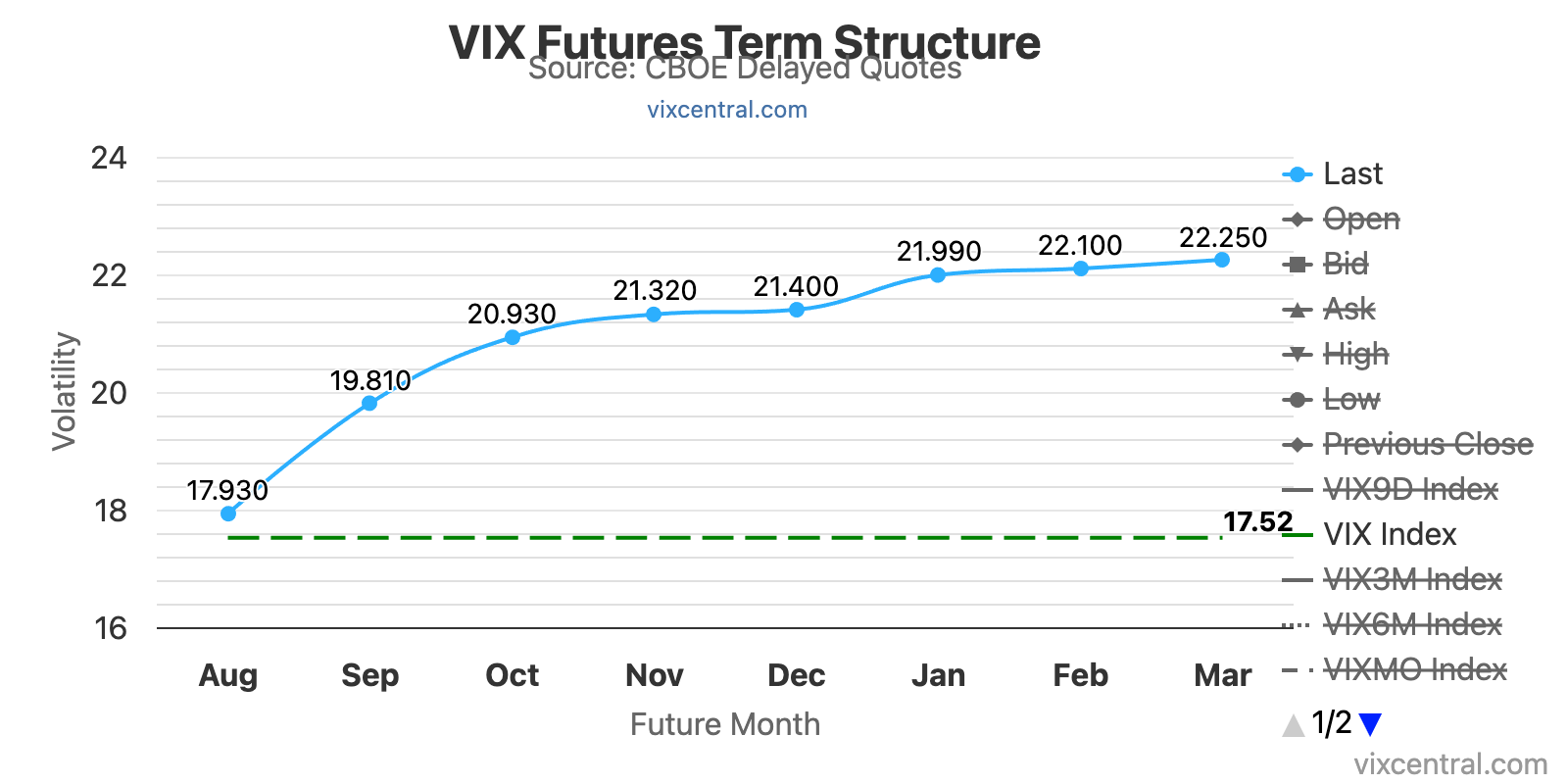

Right now, the curve slopes sharply upward in steep contango: near-term VIX futures trade significantly below longer-dated contracts. This structure screams one thing: market complacency. Investors expect volatility to stay muted in the short term, with only a gradual rise over time. Hedging demand is low, carry trades are thriving, and the market is betting on smooth sailing.

But beneath this calm lies a powerful asymmetry—a coiled spring of risk.

The Setup: Complacency Breeds Fragility

Contango reflects a market lulled into a sense of security. As of August 4, 2025, the spot VIX hovers around 19–20, with August VIX futures near 19.75 and longer-term contracts pricing even higher volatility. This curve shape aligns with a broader narrative of stability, where short-volatility strategies profit from the volatility risk premium—investors consistently overpaying for distant protection.

Contango dominates roughly 80% of the time, but that dominance creates fragility. When markets are positioned for stability, any unexpected shock—geopolitical flare-ups, CPI surprises, Fed missteps, or liquidity cracks—can ignite a volatility spike. We saw this play out in April 2025, when the VIX surged past 60, flipping the curve into backwardation and repricing volatility risk across the board. By July, calm returned and the curve normalized—delivering over +35% gains to inverse-volatility strategies like SVIX.

The Asymmetry: Nonlinear Payoffs

Here’s where the edge lies: volatility doesn’t just rise—it explodes.

When complacency is wrong, the repricing isn’t linear. Traders scramble to hedge, short-vol positions get forcibly unwound, and the curve can invert in hours. This creates convex, nonlinear upside for long-volatility exposures—whether via call options on VIX, structured hedges, or ETPs like VXX.

These long-vol trades act like cheap insurance with explosive optionality. They offer small controlled cost and defined downside, with the potential for outsized payoffs when stress hits the system. That’s the asymmetric risk/reward profile that most investors ignore—until it’s too late.

Watch for leading signals. Metrics like VVIX (the volatility of volatility) and flattening in the front end of the curve can offer early warnings. These subtle shifts—seen briefly in June—suggest market makers are quietly preparing for turbulence before it becomes obvious.

The Edge: ASYMMETRY® Thinking

This isn’t about guessing the next shock.

It’s about structuring the portfolio for payoff asymmetry—preparing in advance for when the odds become skewed in your favor.

The current steep contango presents two paths:

- Exploit the carry: When calm persists, shorting volatility (via SVIX, short VIX futures, or options overlays) can capture steady return from negative roll yield.

- Prepare for the spike: When complacency is mispriced, long-volatility trades can deliver convex payoffs that hedge downside and capitalize on regime shifts.

At Shell Capital, we engineer both sides of this equation. We don’t rely on forecasts—we structure portfolios to adapt, with total portfolio risk exposure limits, predefined exits, and asymmetric hedges in place.

The Bottom Line

- A steep VIX futures curve signals calm—but that calm can be fragile

- Volatility spikes are reflexive and nonlinear—rewarding those positioned with asymmetric payoff structures

- ASYMMETRY® means focusing not just on what the market expects, but where it may be wrong.

In today’s uncertain environment, don’t just ride the calm.

Prepare for the storm.

Because when risk is least expected, the payoff is most asymmetric.