When Credit Spreads Compress, Asymmetric Risk/Reward Shifts

What the Research Shows

In “When the Upside Is Thin, Upgrade the Carry,” GMO argues that tight credit spreads create asymmetric downside risk. When spreads are already compressed, the opportunity shifts from chasing yield to structuring carry with defined downside and lower convexity risk.

In “When the Upside Is Thin, Upgrade the Carry,” GMO writes that current investment-grade corporate spreads sit near historically tight levels. When spreads compress to these levels, the forward distribution of outcomes tends to skew toward widening rather than further tightening.

That matters structurally.

Credit markets are cyclical but also incentive-driven. When spreads compress, yield targets don’t disappear. Institutional investors still need income, and that pressure often pushes capital down the credit stack or into structures with embedded risk.

The result is a common regime: tight spreads, persistent demand for yield, and investors accepting thinner compensation for credit risk.

In that environment, the opportunity isn’t prediction. It’s structure.

If the upside from further spread compression is limited while downside from widening remains open, the asymmetry shifts. Portfolio construction must rotate from maximizing carry to upgrading the quality of that carry.

What the research actually says

GMO’s core thesis is straightforward.

When credit spreads are already tight, investors should focus on improving the quality of carry rather than reaching for additional yield.

The firm highlights several observations from historical spread data and structured credit markets.

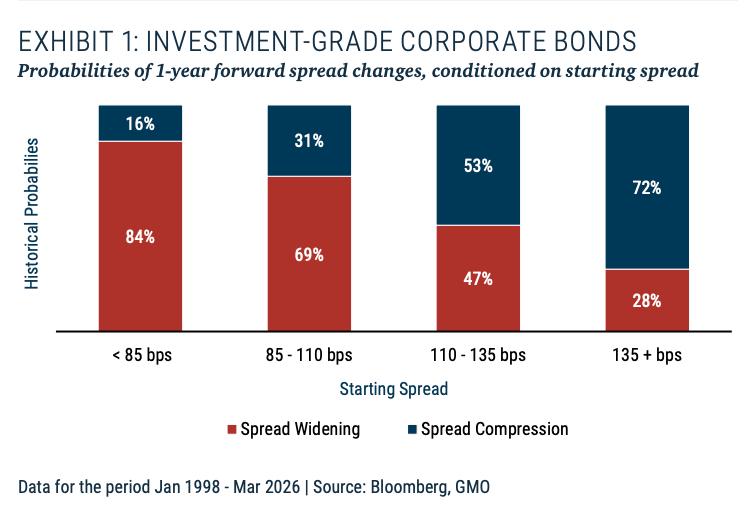

First, investment-grade spreads are currently near historically compressed levels. IG spreads around 85 basis points sit near the 19th percentile over the past five years. Based on historical data since 1998, starting spreads below this level have led to spread widening roughly 84% of the time over the following year.

Second, tight spreads create asymmetric mark-to-market risk. Even though investment-grade bonds have low default risk, they remain vulnerable to price declines if spreads widen. With long spread duration, modest widening can overwhelm the expected carry over a typical holding period.

Third, structured credit can offer similar or better carry with lower spread sensitivity. GMO reports that its Opportunistic Income Strategy generated an average spread advantage of roughly 42 basis points over IG corporates since 2016 while maintaining about 5.6 years less spread duration.

Fourth, the capital structure often contains mispriced risk. Investors frequently move down the capital stack in search of yield, which can leave senior tranches undervalued on a risk-adjusted basis. Senior structured credit bonds receive payments first and absorb losses only after subordinate tranches are wiped out.

Fifth, negative convexity can distort risk/reward. Certain structured securities—such as some CLO tranches—contain embedded options that create asymmetric behavior. When spreads tighten, upside is capped because the issuer may refinance. When spreads widen, duration extends, increasing downside exposure.

GMO argues that avoiding poorly compensated negative convexity and focusing on senior positions in the capital structure can materially improve risk-adjusted returns.

The assumptions behind this thesis are relatively clear.

Credit spreads are currently near cycle tights. Investor demand for yield remains persistent. Structured credit markets contain pricing inefficiencies across capital structures. Spread duration and convexity materially influence realized returns during credit volatility.

Boundary conditions and limitations

The research is strongest where it analyzes spread distributions and capital-structure mechanics.

Historical data showing how starting spreads influence forward outcomes provides a clear statistical framework. Similarly, the structural examples illustrating tranche leverage and loss absorption are grounded in well-understood securitization mechanics.

Where the research is weaker is in implementation generalization.

Structured credit markets are heterogeneous. Performance depends heavily on collateral quality, deal structure, manager selection, and liquidity conditions. The analysis also relies on strategy-specific performance data from GMO’s Opportunistic Income portfolio, which may not represent the broader asset class.

The paper also does not address liquidity stress scenarios in detail. Structured credit can behave differently during systemic liquidity shocks, particularly when dealer balance sheets are constrained.

What would falsify the thesis is straightforward.

If spreads continue compressing materially from current levels without widening, the assumed asymmetric distribution would weaken. Alternatively, if structured credit markets become crowded with capital seeking the same “quality carry” exposure, pricing advantages could compress.

The ASYMMETRY® perspective

From an ASYMMETRY® perspective, the most important idea in this paper isn’t the specific securities GMO prefers.

It’s the geometry of the opportunity set.

When spreads compress, the asymmetry in credit markets changes shape.

Upside becomes constrained because spreads can only tighten so much. Downside remains open because spreads can always widen. That creates a distribution where expected returns increasingly depend on carry and volatility management rather than capital gains.

In other words, the edge shifts from direction to structure.

Several structural forces reinforce this.

Institutional mandates often encourage reaching for yield within rating buckets. Pension funds, insurance portfolios, and income strategies frequently maintain yield targets regardless of spread levels. When spreads compress, those incentives push capital toward lower-quality or structurally riskier exposures.

That demand can misprice risk inside capital structures.

The safest tranches sometimes offer relatively attractive risk-adjusted returns because investors prefer higher coupons from subordinate slices. Behavioral incentives interact with regulatory constraints and portfolio mandates, creating structural inefficiencies.

That’s where asymmetry appears.

Not because the asset class itself is inherently asymmetric, but because investor behavior and market structure can temporarily distort risk pricing.

In this case, the edge is primarily structural and behavioral.

The structural element comes from capital-stack mechanics and convexity features. The behavioral element comes from yield-seeking flows.

Neither is permanent. But both can persist long enough to matter for portfolio construction.

Asymmetric risk/reward geometry

Downside definition

The primary risk is spread widening. When spreads are already tight, duration exposure can translate modest widening into meaningful mark-to-market losses.

Defined downside in this environment means controlling spread duration, limiting structural leverage, and avoiding securities where convexity amplifies widening events.

Upside optionality

Upside comes primarily from carry rather than price appreciation. If spreads remain stable, higher-quality carry compounds over time. Additional optionality appears if volatility increases and new credit opportunities emerge at wider spreads.

Path dependency

The path matters.

If spreads remain tight or grind tighter slowly, carry dominates returns. If spreads widen sharply, strategies with lower spread duration and stronger capital-structure protection should experience smaller drawdowns.

Skew

The distribution is negatively skewed for long-duration credit exposure at tight spreads. Structuring carry with shorter duration and senior capital-structure positioning can improve skew by compressing the downside tail.

Time dimension

This is primarily a medium-cycle structural opportunity. It tends to emerge late in credit cycles when spreads compress and investor demand for yield intensifies.

Portfolio construction implications

The research primarily affects several return drivers.

Credit spreads Liquidity conditions Volatility in fixed income markets Real rates and duration sensitivity

Reducing spread duration directly lowers exposure to spread volatility. Prioritizing senior tranches shifts risk away from default events toward collateral performance and structural protections.

Correlation also matters.

Traditional corporate credit tends to correlate strongly with equity risk during stress periods. Certain structured credit exposures may exhibit different sensitivity depending on collateral type, capital-structure position, and duration.

From a risk budgeting perspective, the key issue is portfolio risk concentration.

Portfolios heavily exposed to long-duration corporate credit effectively embed a directional spread trade. If spreads widen, those exposures can fail together.

A structured approach to carry attempts to isolate income generation while controlling the spread sensitivity embedded in the position.

Implementation approaches could include:

structured credit exposure with senior capital-structure positioning active management of spread duration defined-risk overlays to control spread volatility liquidity-aware rebalancing as credit spreads shift

None of these require predicting credit cycles. They require structuring exposure so that the downside remains controlled if spreads move against the position.

Why this matters for families with meaningful capital at stake

For families managing permanent capital, credit exposure often plays a stabilizing role in the portfolio.

But stability depends on structure.

When spreads are tight, credit portfolios can quietly accumulate asymmetric downside risk. Investors may believe they hold “high-quality income,” yet the embedded spread duration creates vulnerability to drawdowns if spreads widen.

That matters for portfolios tied to real-world obligations.

Liquidity events, retirement funding, business transitions, and estate planning all depend on capital preservation. Drawdowns in fixed income allocations can become particularly damaging when they coincide with other portfolio stress.

The practical implication isn’t to abandon credit.

It’s to understand how the risk geometry changes across regimes.

Carry isn’t automatically safe. It must be structured.

Failure modes and what we’d watch

Several signals would indicate that the asymmetry described in this research is changing.

Credit spreads widening materially toward historical medians Investor flows rotating away from yield-seeking strategies Structured credit spreads compressing relative to corporate credit Liquidity deterioration in securitized markets Volatility regimes shifting in fixed income

Each of these would alter the distribution of outcomes and potentially compress the asymmetry currently embedded in carry structures.

Bottom line

When spreads are already tight, the asymmetric opportunity in credit shifts from chasing yield to structuring higher-quality carry with defined downside and controlled convexity.

This commentary is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. All investments involve risk, including possible loss of principal. Past performance does not guarantee future results. Shell Capital Management, LLC is a registered investment adviser. Registration does not imply a certain level of skill or training.