Asymmetry Is Defined by Downside, Not Upside

Asymmetry Is Defined by Downside, Not Upside

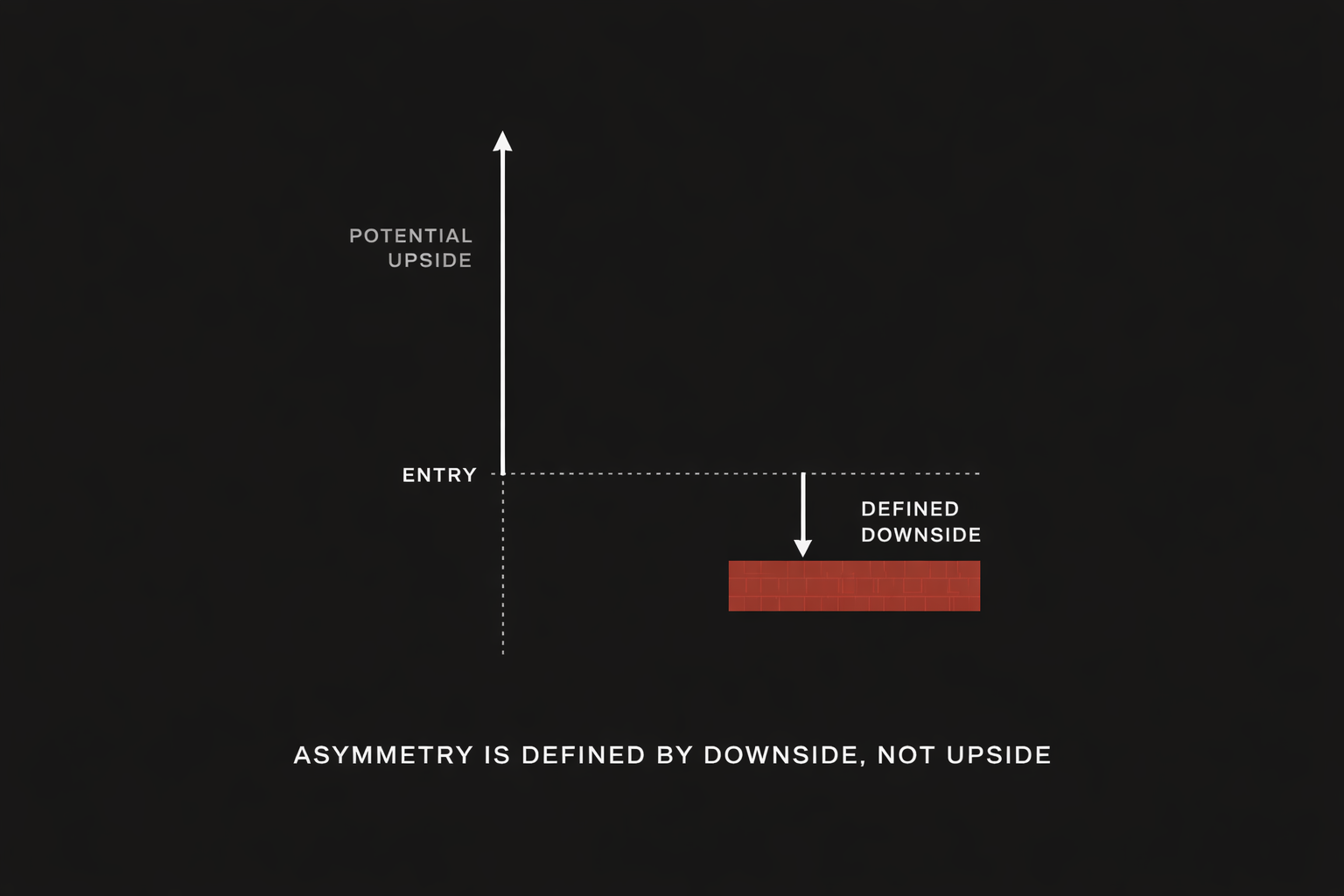

Asymmetry in investing is often described as “large upside potential.” That framing is incomplete, and in practice it’s usually wrong. True asymmetry is not created by imagining how much something could go up. It’s created by defining how much it can go down before you ever participate in the upside.

This distinction matters because capital isn’t lost in missed upside. It’s lost in unbounded downside, drawdowns that impair compounding, and exposures that only look attractive when things go right. Asymmetry begins with survival, not stories.

The misconception

Many investors believe asymmetry exists whenever the upside appears larger than the downside. A stock that “could double” or an asset that “can only go to zero” is often labeled asymmetric by default. The focus is placed on payoff potential rather than loss structure.

That framing confuses possibility with geometry.

The correction

Asymmetry is a property of the risk profile, not the return narrative. It emerges when downside is explicitly defined, limited, and survivable, while upside remains open-ended or meaningfully larger than the predefined loss.

Without a known loss boundary, the distribution cannot be asymmetric in a useful way. The downside dominates the math, regardless of how compelling the upside sounds. This is why two investments with identical expected returns can produce dramatically different outcomes over time: one contains loss, the other compounds it.

Upside is optional. Downside is compulsory.

The boundary condition

This principle breaks the moment downside is assumed rather than specified. If risk expands during stress, if exits are discretionary, or if correlations rise when protection is needed most, the asymmetry collapses. What appeared convex becomes linear, and what appeared limited becomes fragile.

Undefined risk doesn’t create asymmetry. It destroys it.

Implications for capital

For serious capital, asymmetry is not an idea-level concept. It’s a portfolio construction discipline. Defined downside enables position sizing, risk aggregation, and durability across regimes. Without it, upside potential is irrelevant because losses dominate long-term outcomes.

This is why professional capital allocators start with loss tolerances and risk budgets, not return targets. Compounding requires staying in the game.

Asymmetry is not about how much you can make when you’re right. It’s about how much you lose when you’re wrong, and whether that loss is controlled.

If you can’t define the downside, you don’t get to talk about the upside.

Disclosure: Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. Examples are illustrative and not indicative of future results. Investing involves risk, including the potential loss of principal. Opinions are subject to change without notice.