Capital Efficiency Sounds Like Optimization. It’s a Leverage Decision.

Capital efficiency is often presented as a smarter way to build a portfolio. More exposures. Better diversification. Expanded opportunity set.

That framing is incomplete.

The reality is simpler and more important: capital efficiency is a decision to separate capital from exposure—and in many implementations, to use leverage to stack exposures inside the same portfolio.

The misconception is that stacking exposures automatically improves diversification.

It doesn’t.

It changes the structure of the portfolio.

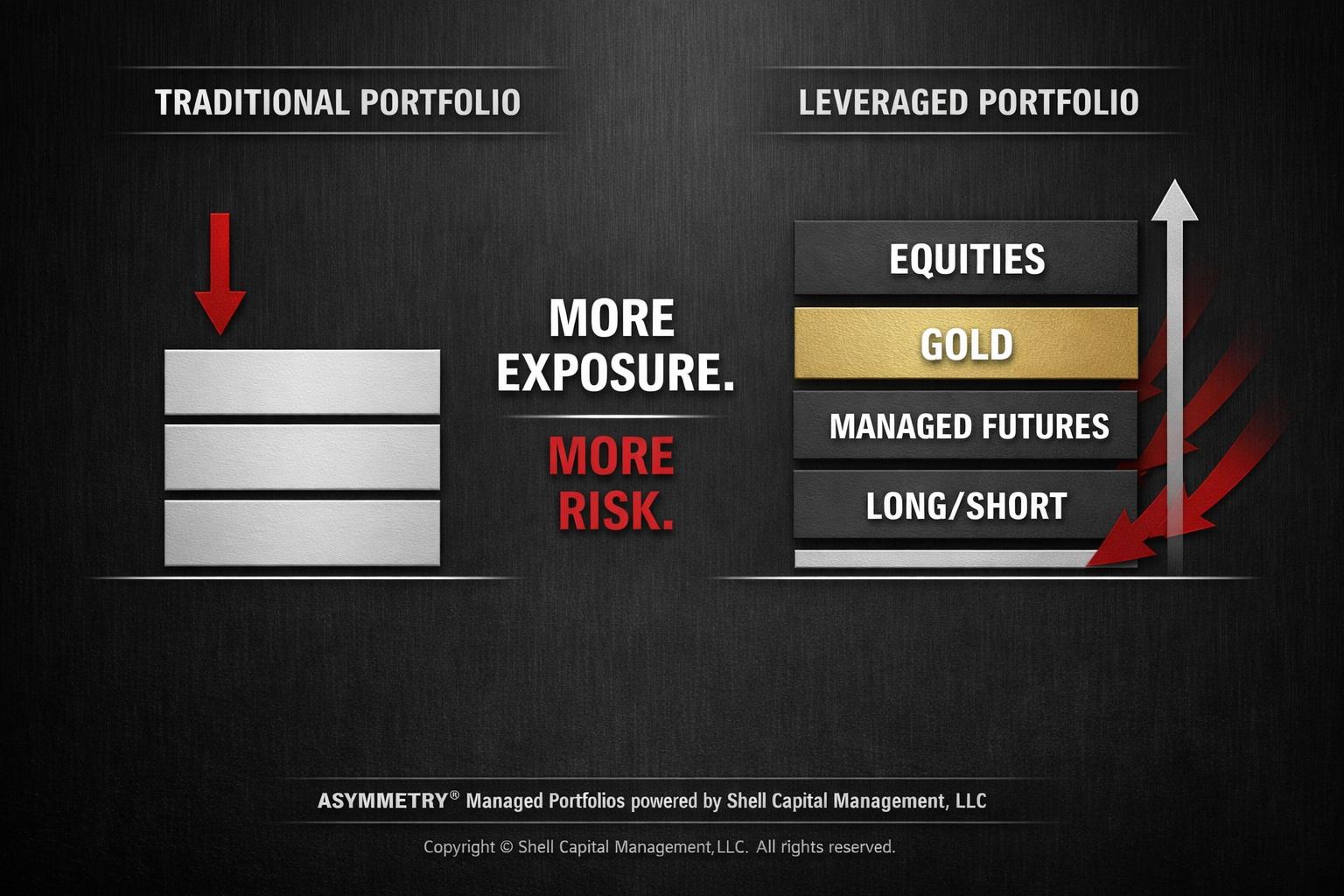

Traditional portfolios are constrained by capital. If you want to add something, you typically have to sell something else. That forces tradeoffs.

Capital-efficient structures remove that constraint.

They allow a portfolio to maintain core exposures while layering additional return drivers on top through derivatives and overlays.

On the surface, that looks like an improvement.

In practice, it replaces a simple tradeoff with a more complex one.

The question is no longer “What do I own?”

The question becomes “What is my total exposure—and how does it behave when conditions change?”

This is where outcomes diverge.

Stacking exposures increases gross exposure relative to capital. That introduces path dependence, financing costs, and—most importantly—interaction risk between components.

Those interactions are stable in calm markets.

They are not stable in stressed markets.

What appears diversified when volatility is low can begin to move together when liquidity tightens and selling pressure builds. That’s not a theoretical risk. It’s how portfolios behave when they’re tested.

This is the part most investors underestimate.

Capital efficiency doesn’t fail because the idea is wrong.

It fails when the interaction between exposures is not fully understood in advance.

From a first-principles perspective, stacking exposures does four things:

It increases total notional exposure.

It introduces path-dependent outcomes through roll, financing, and rebalancing.

It relies on correlations that shift across regimes.

It concentrates risk in the interaction between exposures, not just the exposures themselves.

That doesn’t make it bad.

It makes it conditional.

If the added exposures are truly differentiated—if they behave differently when it matters, reduce drawdown depth, or improve recovery—then the portfolio’s asymmetric profile may improve.

If they converge with the core risk during stress, the same structure can amplify drawdowns while appearing diversified in normal conditions.

This is where consequence shows up.

A 10% drawdown requires roughly an 11% recovery to break even.

A 20% drawdown requires 25%.

A 30% drawdown requires over 40%.

When exposures are stacked, those drawdowns can accelerate—not because any single position failed, but because multiple exposures began trending together at the same time.

That is the difference between theoretical diversification and realized risk.

Viewed through an ASYMMETRY® lens, the objective isn’t to increase exposures per dollar of capital.

The objective is to improve asymmetric outcomes: define downside, preserve optionality, and introduce convexity where it matters.

That requires discipline at the portfolio level, not just the position level.

Total exposure must be measured, not assumed.

Correlation must be evaluated under stress, not just in stable periods.

Volatility must be accounted for as it changes effective position size.

Downside must be defined in advance and actively managed as conditions shift.

Without that, capital efficiency does not create an edge.

It introduces leverage without improving the distribution of outcomes.

A simple example illustrates the point.

A portfolio maintains equity exposure through derivatives and uses freed capital to add gold, managed futures, or long/short strategies. Structurally, it now holds more exposures without reducing the core.

But the result depends entirely on how those exposures behave together.

If they offset each other during stress, the portfolio becomes more resilient and recovery improves.

If they move together at the wrong time, drawdowns deepen and recovery becomes more demanding.

Capital efficiency doesn’t eliminate tradeoffs.

It transforms them.

Instead of choosing between assets, the portfolio accepts leverage, complexity, and interaction risk in exchange for expanded exposure.

For those responsible for managing meaningful capital, that distinction matters.

The goal isn’t to build the most efficient-looking portfolio.

The goal is to manage consequence.

Capital efficiency is best understood as exposure engineering.

In many real-world implementations, it is leveraged portfolio construction expressed through overlays.

It improves outcomes only when the added exposures enhance asymmetry—by reducing downside, improving recovery, or introducing convexity across different regimes.

If it doesn’t, it simply amplifies whatever risk already exists.

The relevant question isn’t whether a portfolio is more capital efficient.

The relevant question is what happens when those exposures are wrong at the same time.

Because that is when the math—and the consequences—become real.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.