When Enthusiasm Crowds One Side of the Boat

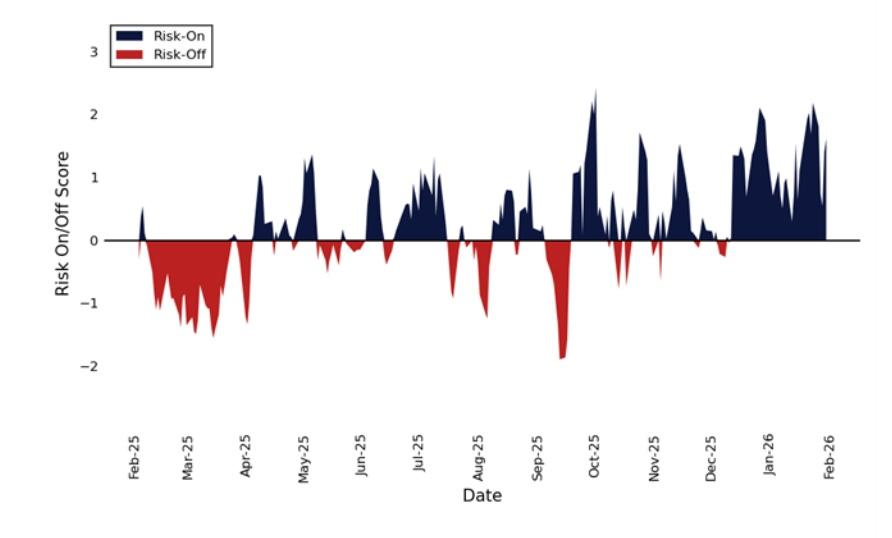

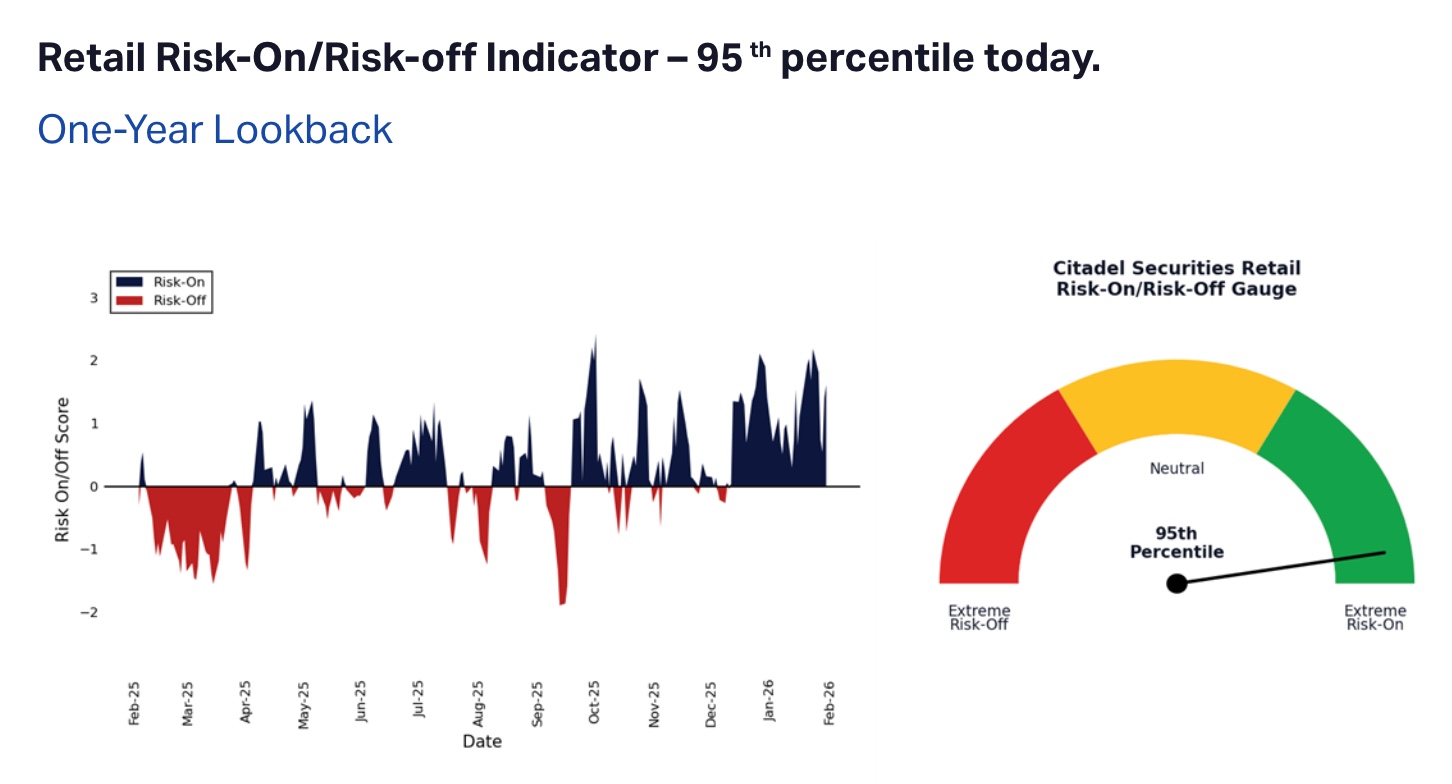

Citadel Securities’ Retail Risk-On/Risk-Off Gauge

is currently at the 95th percentile on a one-year lookback, signaling unusually strong retail risk appetite. When retail positioning clusters at extremes, forward return dispersion often widens. Extremes in risk preference don’t predict timing, but they materially change the distribution of potential outcomes.Citadel Securities is one of the largest market makers in the world. They internalize and execute a significant share of U.S. retail equity and options order flow. That gives them something most investors don’t have: a real-time lens into how millions of individual investors are positioning across risk assets.

When a firm with that kind of order flow visibility publishes a “Retail Risk-On/Risk-Off” gauge, it isn’t based on survey sentiment. It’s based on actual transactions — where retail capital is flowing, what it’s buying, and how aggressively it’s expressing risk.

Right now, that gauge sits at the 95th percentile over the past year.

That’s not neutral. That’s crowded.

What “95th percentile” really means

A percentile doesn’t tell you direction. It tells you extremity.

At the 95th percentile, retail risk appetite has been higher only 5% of the time in the past year. That’s statistically rare. It implies concentration — positioning skewed toward risk-on exposure rather than defensiveness.

In market structure terms, it means:

Retail demand for upside participation is elevated. Risk-off hedging appetite is subdued. Positioning asymmetry is building on one side of the distribution.

This is not a forecast. It’s a condition.

And conditions shape asymmetry.

Extremes and asymmetric payoffs

When positioning becomes one-sided, two things happen simultaneously.

First, incremental buyers diminish. If most retail participants are already leaning risk-on, the marginal new buyer pool shrinks. Upside velocity can slow because enthusiasm is already expressed.

Second, downside air pockets expand. If something shifts — macro, liquidity, volatility regime — the unwind can accelerate as crowded positioning reverses.

This is classic convexity math.

When enthusiasm clusters at extremes, upside becomes more linear while downside can become more convex.

That’s not bearish. It’s structural.

Retail isn’t the whole market — but it’s not irrelevant

Institutional flows, CTA positioning, dealer gamma, volatility supply/demand, and macro liquidity all matter. Retail is one component of a multi-lens framework.

But retail extremes have historically coincided with:

Momentum extensions near late-stage moves Elevated options activity Compressed perceived risk

None of these guarantee reversal. They increase fragility.

From an ASYMMETRY® perspective, fragility matters more than direction.

Regime awareness versus prediction

If the tape is trending and risk appetite is expanding, fighting it prematurely destroys convexity. But ignoring positioning extremes entirely is equally dangerous.

The question isn’t “Is this bullish or bearish?”

The question is:

Is the risk/reward still asymmetric in your favor, or has it shifted toward symmetry — or worse, negative convexity?

At the 95th percentile, retail enthusiasm is no longer under-owned. It’s well expressed.

That changes how capital should be structured.

Capital implications for families and founders

For families with meaningful capital at stake, this is where process matters more than opinion.

When sentiment is extreme:

Defined exits become more important. Portfolio risk budgeting becomes more critical. Optionality becomes more valuable than linear beta.

You don’t need to predict the turn. You need to define the downside in advance.

If risk-on trends continue, disciplined exposure participates. If risk-on reverses, predefined risk controls preserve optionality.

That’s engineered asymmetry.

Citadel Securities’ retail data tells us retail risk appetite is stretched to the 95th percentile. That’s a condition of elevated enthusiasm and concentrated positioning.

Extremes don’t tell us what happens next. They tell us the distribution has shifted.

In markets, asymmetry doesn’t come from guessing direction. It comes from structuring exposure so that when positioning extremes unwind — or extend — you remain convex either way.

That’s the edge.