Fighting the Last Battle

March 9, 2009, marked the end of the financial crisis bear market. But the deeper lesson isn’t the recovery that followed—it’s how investors and portfolio managers often stay positioned for the crisis that already happened.

March 9, 2009, is often remembered as the start of a powerful bull market. It marked the final low of the Global Financial Crisis, but no one knew it at the time.

But the more important lesson begins earlier.

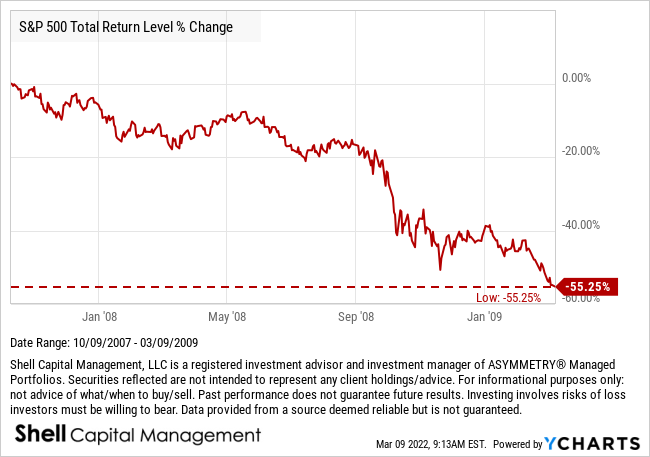

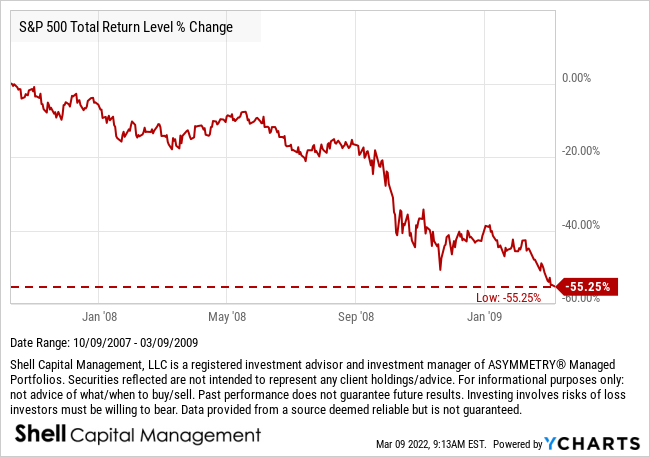

The financial crisis bear market didn’t start in 2008. It began in October 2007 and continued until March 9, 2009. Over that period the S&P 500 declined about −56%.

That’s the part many investors prefer to forget.

Market anniversaries tend to focus on the gains that followed the low. But starting the clock at the bottom distorts the full cycle. A meaningful evaluation of risk and reward begins at the previous peak, not the point of maximum panic.

A +100% gain after a −50% loss doesn’t create wealth if the loss occurred first.

This is why downside matters more than upside.

The upside rarely causes the real damage in portfolios. The downside does.

Large drawdowns permanently alter the path of compounding. Recovering from deep losses requires exponentially larger gains, and the time required to repair that damage can span years.

The −56% decline during the financial crisis left more than financial damage. It left psychological scar tissue across the entire investment landscape.

And that scar tissue shaped investor behavior long after the crisis ended.

In the years following the March 2009 low, many investors and portfolio managers remained positioned for another immediate collapse. Their portfolios reflected the trauma of the financial crisis rather than the regime that was actually emerging.

In the Marines, there was a phrase for this.

Fighting the last war.

Armies often prepare for the previous conflict, deploying tactics that once worked against an enemy that no longer exists.

Capital markets exhibit the same pattern.

After the financial crisis, investors continued searching for the same risks that caused the collapse: housing, bank solvency, and systemic credit stress. Those threats dominated the narrative even as markets began transitioning into an entirely different environment.

Meanwhile, the regime had changed.

Central banks injected unprecedented liquidity into financial markets. Credit conditions stabilized. Volatility gradually contracted. Risk assets began trending higher as capital flowed back into the system.

Markets had moved forward.

But many portfolios had not.

Part of this anchoring is behavioral. Severe drawdowns create powerful recency bias. Investors naturally overweight the probability that the most recent disaster will repeat.

But there is another force at work in professional asset management.

Career risk.

After a catastrophic drawdown, the safest professional posture is often defensive positioning. Being underexposed is easier to justify than being fully invested ahead of another potential decline.

The safer professional decision can become the wrong portfolio decision.

Ironically, the investors who were able to take advantage of the March 2009 recovery were not simply courageous at the bottom. They were prepared before the collapse.

They had preserved capital. They had liquidity available. They had defined their downside earlier in the cycle.

Preparation created optionality.

Optionality allowed them to deploy capital when forced liquidation created asymmetric opportunity.

That distinction matters.

The real edge in markets rarely appears during the panic itself. It is created beforehand through risk management, capital preservation, and process.

This pattern has repeated across market history.

After the Great Depression, investors spent years fearing another economic collapse. After the inflation crisis of the 1970s, markets priced persistent inflation risk for nearly a decade. After the technology bubble burst in 2000, investors remained skeptical of growth companies for years.

Major crises reshape expectations.

But markets rarely repeat the same crisis mechanics immediately afterward. Policy responses, regulation, and investor behavior all shift after the collapse.

In other words, the next cycle almost never looks like the last one.

This is where asymmetry becomes critical.

Asymmetric portfolio management isn't about predicting the next crisis. It is about defining the downside in advance so capital can remain exposed to the opportunities created by the regime that actually unfolds.

Defined downside creates optionality.

Optionality allows portfolios to adapt rather than remaining anchored to the narrative of the previous crisis. For us, preparation created optionality.

During the financial crisis, the S&P 500 declined about −50.95% from peak to trough. Over the same period, my ASYMMETRY® Global Tactical portfolio experienced a maximum drawdown of about −14.33%. By avoiding most of the collapse, the portfolio entered the recovery from a position of strength rather than weakness. Investors who lose −50% of their capital must first repair the loss before they can participate in new gains. Investors who preserve capital can focus on opportunity instead of recovery.

The real lesson of March 9, 2009, isn’t simply that markets recover after catastrophic declines. In fact, past performance is never a guarantee of future results.

It’s that the biggest mistakes often occur after the crisis ends—when investors and portfolio managers remain positioned for the battle that has already been fought.

Capital compounds when portfolios evolve with the regime.

Capital stagnates when investors continue fighting the last battle.

And the next market cycle will almost certainly look different from the last one.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.