People Often Earn Money in One Business — Then Lose It in Another

One of the most common and costly patterns in private wealth has nothing to do with intelligence, effort, or ambition.

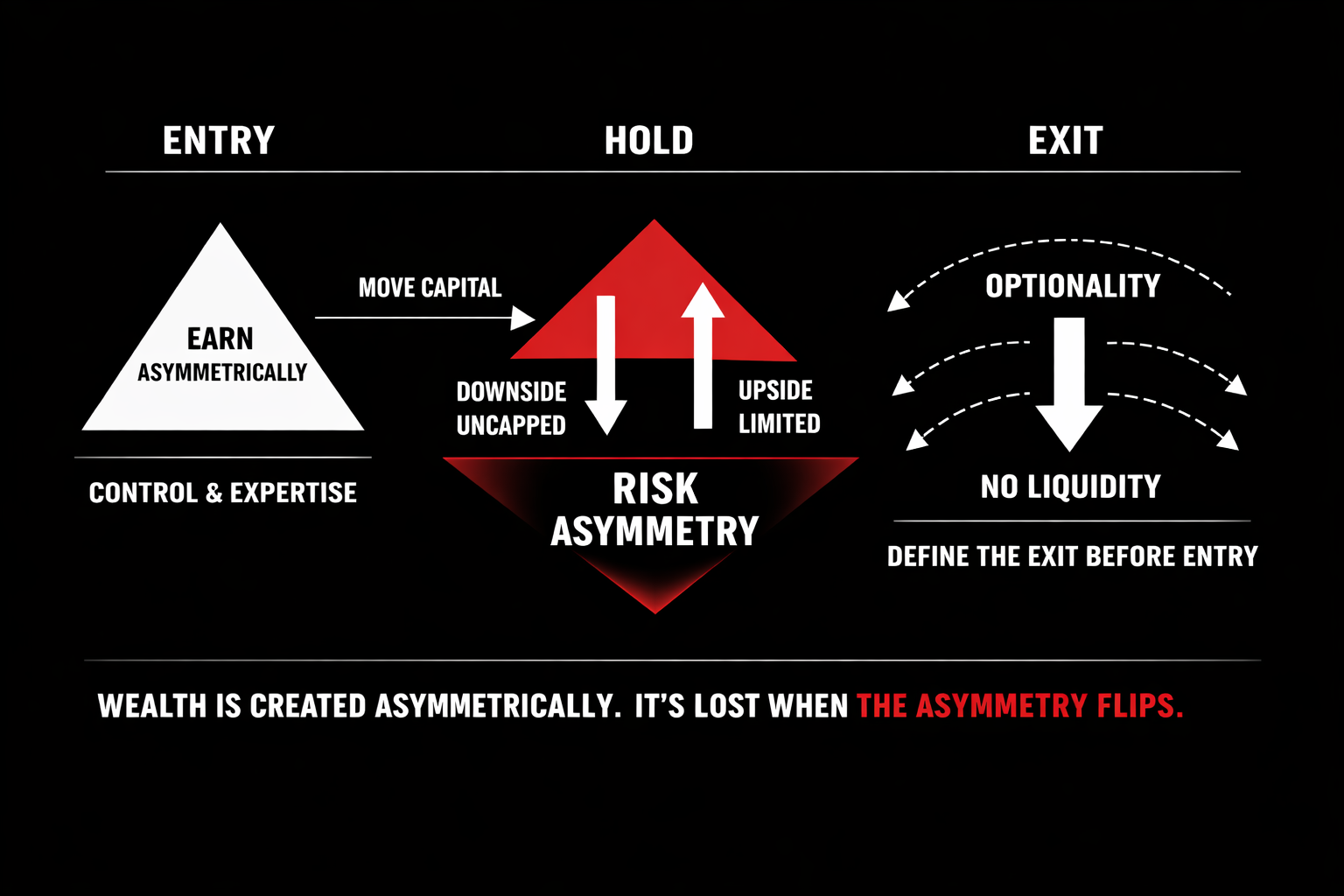

It has everything to do with asymmetry.

People often earn significant wealth in one profession or business—then lose a meaningful portion of it when they redeploy that capital somewhere else.

Not because they were reckless. Not because they were uninformed.

But because the risk geometry changed, and they carried the wrong mental model with them.

The Core Principle

Wealth is usually created under one set of asymmetric conditions and lost under another.

Earning money and allocating capital are not the same skill.

Where Wealth Is Typically Earned

Across professions and businesses, wealth is most often created under favorable asymmetry:

- Concentrated effort

- Deep domain expertise

- Control over decisions

- Time arbitrage

- Bounded losses with open-ended upside

This shows up clearly in:

- Physicians, surgeons, and dentists building durable income streams

- Business owners compounding enterprise value over decades

- Entrepreneurs enduring volatility for a nonlinear exit

The common thread isn’t luck.

It’s structural asymmetry.

Where the Asymmetry Breaks

The break usually happens after the money is earned.

Professionals Investing Outside Their Field

We’ve seen highly successful physicians, surgeons, and dentists invest heavily in businesses they don’t operate.

They move from:

- High control → low control

- Transparent risk → opaque risk

- Repeatable income → dependent outcomes

What looks like diversification is often concentrated, illiquid exposure with limited exit paths.

The upside is capped by deal terms. The downside is uncapped by structure.

Business Owners After a Liquidity Event

We see the same pattern after a successful exit.

An owner sells a business they built and controlled—then:

- Buys another business

- Invests heavily as a passive partner

- Starts something new with significant capital

The mistake isn’t ambition.

It’s the silent shift from operator to capital provider.

Control disappears. Timing authority disappears. Exit optionality disappears.

The asymmetry flips.

The Exit Lens (Our Framework)

Here’s the principle we use internally:

Every capital decision has an exit—explicit or implicit.

Most losses occur not because the opportunity was inherently bad, but because:

- The exit wasn’t defined before entry

- Liquidity was assumed instead of engineered

- Timing depended on ideal conditions

- Downside wasn’t structurally limited

Capital without an exit plan isn’t invested.

It’s exposed.

The ASYMMETRY® Perspective

Capital earned asymmetrically should be managed asymmetrically.

That means:

- Defined downside before capital is committed

- Optionality instead of obligation

- Multiple exit paths, not one

- Liquidity as a feature, not a hope

- Structures designed to survive extraordinary periods

Whether you’re a professional investing outside your expertise or a business owner redeploying proceeds after a sale, the geometry matters more than the story.

A Quiet but Expensive Truth

Most fortunes aren’t lost where they’re made.

They’re lost when success creates confidence—and confidence replaces structure.

Earning money is about expertise. Keeping it is about asymmetry. Compounding it over a lifetime requires understanding the entire lifecycle of capital—from creation, to exit, to redeployment.

The exit doesn’t just determine the outcome of a business.

It determines what happens to everything that comes after.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. The content is not intended to provide a complete description of Shell Capital’s investment process or strategies and should not be relied upon in making investment decisions.

Securities, charts, indicators, formulas, or examples referenced are illustrative in nature and are not intended to represent actual client holdings or recommendations. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal.

Any opinions expressed are subject to change without notice as market conditions evolve. All information is believed to be reliable but is not guaranteed and should be independently verified. Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement.

This material is not intended as an offer or solicitation for advisory services in any jurisdiction where such offer or solicitation would be unlawful.