Quantitative Rules-Based Trading Systems Don't Remove the Emotion

I began engineering and testing quantitative trading systems during the 2000–2003 market collapse that followed the tech bubble. At the time, there were very few complete frameworks that addressed the full set of decisions real markets demand: what to buy or sell short, when to do it, how much to allocate, when to exit a loser, when to abandon a laggard, and when to let a winner run.

What did exist came primarily from the CTA and managed futures world. My early work was influenced by that discipline—particularly the structure behind the Original Turtle Trading Rules. Not the mythology, but the engineering: predefined downside, volatility-based position sizing, systematic entries and exits, and an explicit focus on asymmetric outcomes. I spent years testing and observing these systems through real-time, walk-forward market conditions before launching Shell Capital in 2004 to operate them in live portfolios.

Those systems were not designed to feel comfortable. They were designed to function when markets were unstable, correlations were breaking, and volatility regimes were changing. That design was tested during the next major stress event, from October 2007 through March 2009. Through that period, our methods behaved as intended, producing the positive asymmetry they were built for and allowing us to continue operating tactically when many others could not.

After what is now shorthand as “2008” and the Global Financial Crisis, the advisory industry found itself exposed. Long-only, fully invested portfolios had failed precisely when protection mattered most. In response, advisers and asset managers began searching for systematic approaches they could present as alternatives.

That search led many of them to backtesting.

Where the misunderstanding begins

Backtesting itself wasn’t the problem. The problem was what people inferred from it.

Rules-based models built on historical data began to be marketed as if they removed emotion from investing altogether. The implication was that quantitative systems replaced human judgment with mathematical certainty—that discipline could be automated and psychology eliminated.

That idea is not just wrong. It’s dangerous.

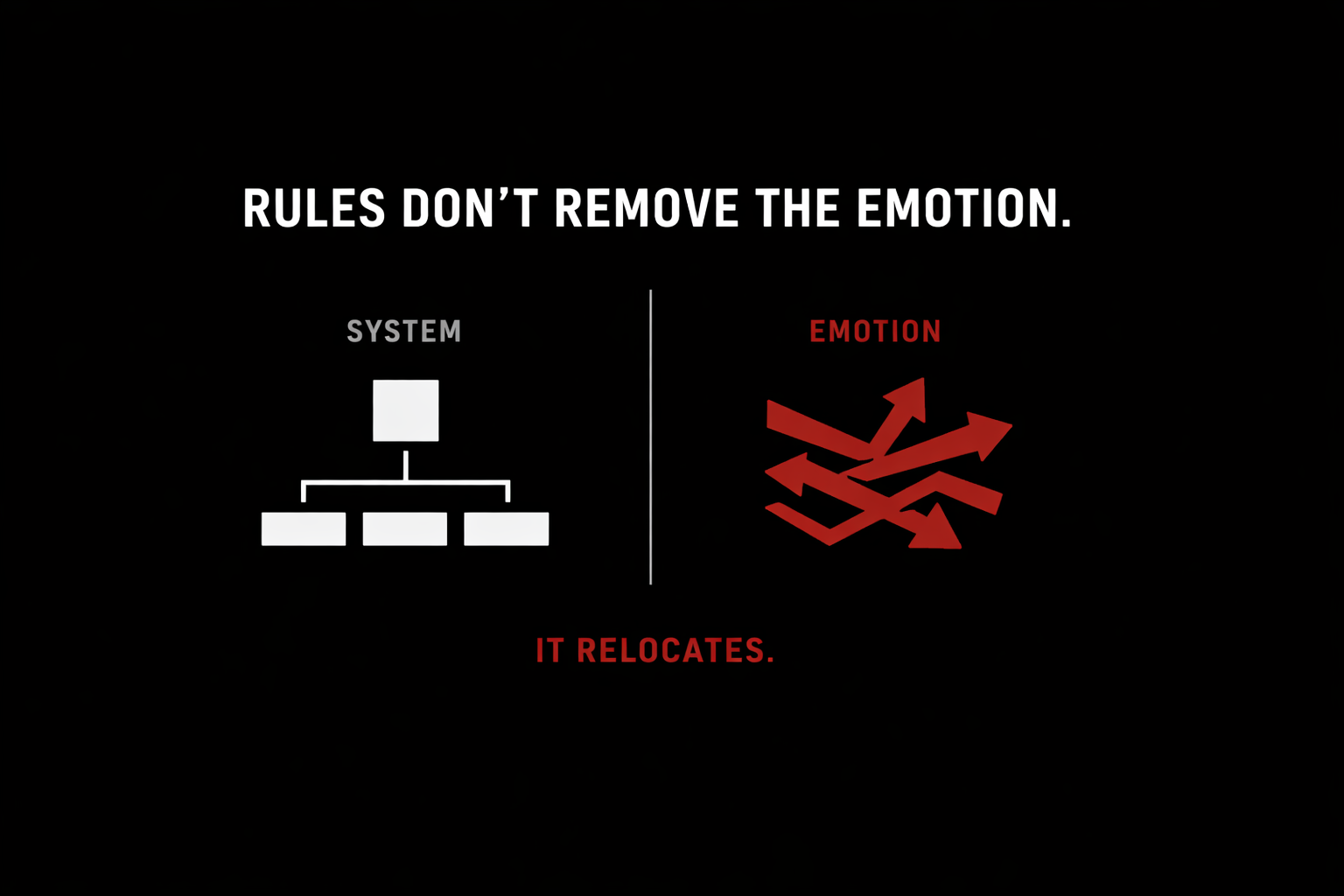

Emotion is not a variable you subtract from an equation. It’s a constant.

What rules can remove is discretion at the point of execution. They can standardize sizing, predefine exits, and eliminate impulsive decision-making in the moment. That matters. But it is not the same thing as removing emotion from the process.

Emotion doesn’t disappear. It relocates.

Where emotion actually does damage

The hardest emotional decisions in investing are rarely about entries.

They happen:

- after a long string of losses

- when a system underperforms for months or years

- when open profits retrace sharply

- when peers are doing something that feels easier

- when confidence erodes but rules remain intact

This is where most systems fail—not mathematically, but behaviorally.

Not because the rules stop working, but because the operator or investor stops trusting them.

Systems don’t eliminate emotion. They reveal whether emotion is allowed to override structure under stress.

Why asymmetry is uncomfortable by design

Asymmetric strategies rarely feel good in real time.

They tend to involve:

- frequent small losses

- long periods of frustration

- infrequent but meaningful gains

- giving back profits before exits trigger

- acting in opposition to consensus

If a strategy feels emotionally easy, it’s often because the asymmetry has already been compressed away.

Discomfort isn’t a flaw. It’s evidence that the payoff distribution is skewed.

The real challenge isn’t finding asymmetric opportunities. It’s building—and maintaining—a structure that allows exposure to persist long enough for asymmetry to materialize.

The ASYMMETRY® perspective

The edge isn’t prediction. The edge isn’t intelligence. The edge isn’t emotional detachment.

The edge is structure.

Structure that defines downside before hope intervenes. Structure that sizes risk before confidence peaks. Structure that exits without negotiation. Structure that assumes emotion will show up—and designs around it.

Anyone can claim their system removes emotion. Very few can demonstrate how it behaves when markets break.

Emotion isn’t removed by systems.

It’s revealed by them.

P.S. After running quantitative systems and tactical methods continuously since the late 1990s—through the tech bubble collapse, the Global Financial Crisis, and multiple volatility and regime shifts in between. What experience teaches you, very quickly, is this: markets don’t test theories, they test operators. If you’re invested with someone who didn’t actively manage capital through those periods—who didn’t have to make real decisions, absorb real drawdowns, and stick with a process when conditions were hostile—you have no way of knowing how they, or their models, will behave in the next recession-driven market crash. Backtests don’t feel stress. Portfolios do, trigger pullers do, and eventually clients do.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.