The Asymmetric Risk Hidden Inside a Calm Market

A quiet index is often a lie of omission.

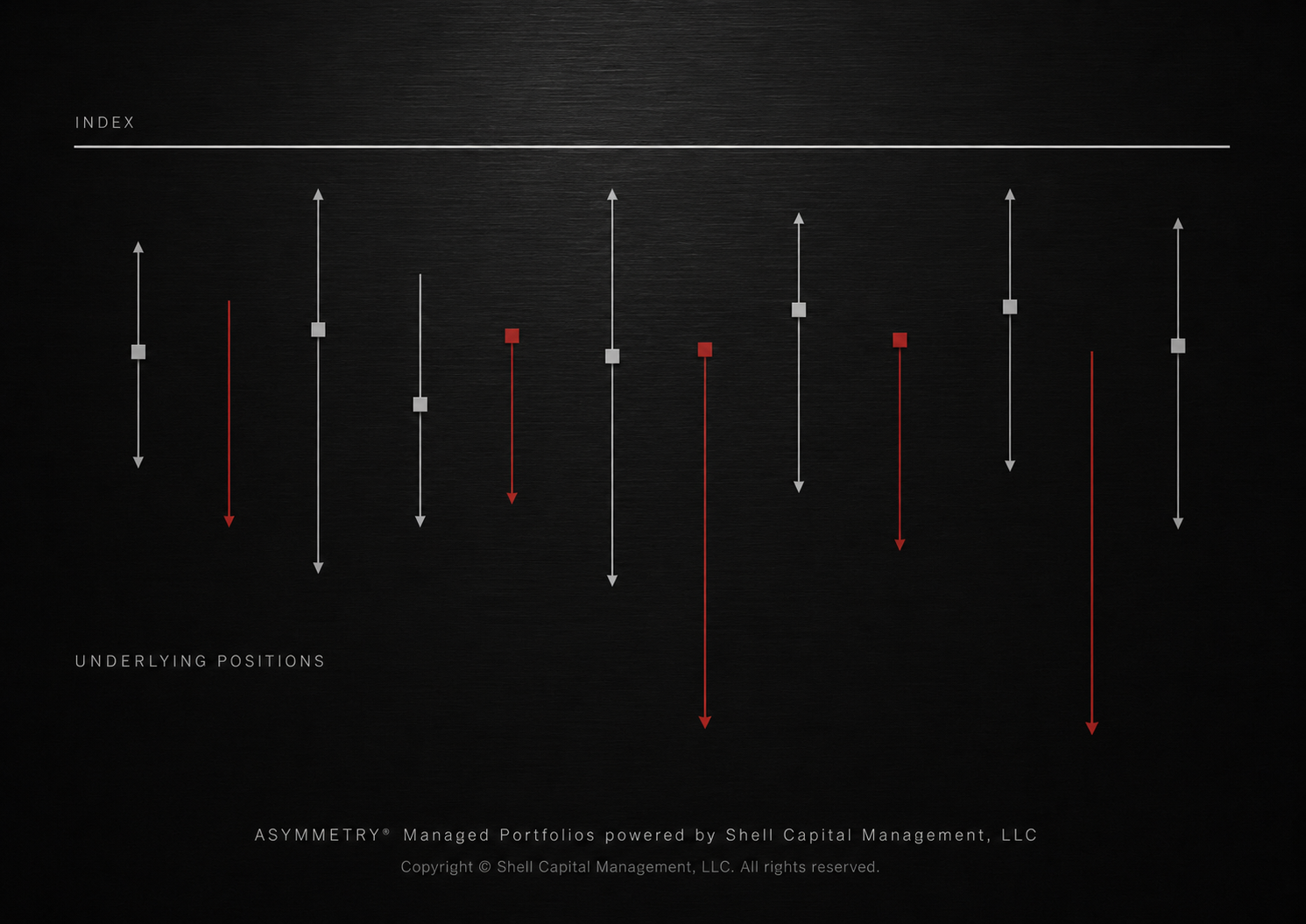

Not intentional. It’s the nature of an average. The index blends a thousand moving parts into one clean number, and sometimes that number makes the market look calmer than it is.

Sometimes the index is quiet because nothing important is happening.

Other times, the index is quiet because powerful moves underneath the surface are offsetting each other.

That second condition is the one worth understanding.

The market’s surface appears calm. But the parts inside the market are moving with unusual force. Some positions are surging. Others are being sold. Capital is concentrating aggressively into narrow leadership. The index smooths all of that into one number.

Your portfolio may not.

That smoothing hides the real condition.

When individual positions are moving violently but the index is not, dispersion is high. Dispersion is simply the gap between the movement of the parts and the movement of the whole.

That gap is where portfolio risk lives.

A portfolio can carry more risk than the index suggests when single positions are moving with high velocity. The index may appear stable, but the underlying return drivers may be unstable, crowded, extended, or highly sensitive to earnings, positioning, liquidity, or catalyst risk.

That’s why I don’t rely on market calm as a risk signal by itself.

Low volatility at the index level can mean risk is low.

It can also mean risk is being compressed, deferred, or hidden by offsetting movement underneath the surface.

Those are very different regimes.

When dispersion is extreme, some positions have already moved aggressively. That changes the math.

A position that has risen more than 100% in a short period is not the same opportunity it was before that move. The story may still be valid. The longer-term thesis may still be intact. But the entry point has changed.

Buying after the crowd has already repriced the story is not the same as buying before the move.

The payoff profile is different.

The asymmetry is different.

After extreme upside moves, short-term follow-through can be fragile. A position may need time to consolidate, digest gains, reset expectations, and shake out late buyers. That doesn’t end the opportunity. It changes the timeframe and the position size.

Momentum can remain valid while the near-term risk/reward deteriorates.

Strong positions don’t need to be abandoned. They need to be handled differently. Position size matters more. The exit needs to be defined before the next test arrives.

The same asset can be attractive over twelve months and unattractive over the next three weeks. Both can be true at once.

In high-dispersion markets, the index is telling you less than it appears to.

Index volatility is low. Single-position volatility is high. Correlation is low. Leadership is narrow. The strongest positions have already moved aggressively. Downside protection may be more valuable in some areas than the index implies.

That combination creates both opportunity and a trap.

The opportunity is that optionality can be mispriced. When correlation is unusually low, the market may be underpricing the probability that individual risks reconnect and move together. When that happens, index volatility can rise quickly, even if it looked dormant before.

The trap is reaching for the obvious trade without respecting the embedded risk.

When dispersion is extreme, many traders want to bet that it reverses. But the wrong expression can be dangerous. Shorting volatile single positions creates open-ended risk if those positions keep extending. The cleaner expression is to own defined-risk convexity tied to correlation returning, index movement increasing, or downside protection becoming more valuable.

Identify the regime. Find the expression with the better risk boundary.

Correlation is the quiet threat in markets like this.

When positions move independently, the index can stay calm while the underlying pieces move hard. That can last longer than expected. Then correlation returns quickly.

The same positions that looked independent start moving together. The calm benchmark reprices. Portfolio volatility rises. The investor who thought they had a quiet portfolio finds out they had concentrated exposure wearing different labels.

That’s usually when people start looking for protection.

Late.

After the price of protection has already changed. After volatility has already expanded. After the market has already made the risk obvious.

That’s especially relevant for business owners, founders, executives, physicians, and families with meaningful capital at stake.

A benchmark doesn’t know your life.

It doesn’t know how much capital you’ve built. It doesn’t know whether your wealth came from a business sale, years of operating risk, concentrated equity, professional income, or a lifetime of disciplined saving. It doesn’t know what a large drawdown would actually cost you.

It only reports the average.

The index doesn’t show position size. It doesn’t show concentration. It doesn’t show whether the portfolio is leaning too hard into one theme. It doesn’t show whether the strongest return drivers have already traveled too far too fast. It doesn’t show whether the downside has been defined before the market tests it.

That’s portfolio management.

The quiet surface can be misleading. The real signal is in the gap between the whole and the parts.

When that gap becomes extreme, the objective isn’t to predict every move. The objective is to manage exposure with enough precision that the portfolio can participate in valid momentum without depending on calm conditions lasting forever.

That means respecting strong trends without chasing them blindly, sizing exposure intentionally, defining exits before volatility expands, and looking for convexity before everyone else wants it.

ASYMMETRY® is built to act before the obvious moment.

The point isn’t to avoid volatility. Volatility is part of markets. It’s also where opportunity often appears.

The point is to avoid being surprised by volatility that was already building beneath the surface.

A calm index can still contain violent positions.

A strong trend can still need a better entry.

A low-volatility market can still carry rising portfolio risk.

The edge is seeing the difference before the market makes it obvious.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.