The Asymmetry Problem With Selling Volatility

Selling volatility still works—until it doesn’t. The real issue isn’t whether the volatility risk premium exists, but where it’s been competed away, how capital concentration changes the payoff geometry, and why most investors are selling convexity without being paid for it.

What this is really about

Public debate frames volatility selling as a binary question: is the volatility risk premium gone, or does it still exist?

That framing misses the point.

The real issue is asymmetry. Specifically, how the payoff profile of selling volatility has deteriorated as capital, products, and institutional mandates have crowded into the same expressions of the trade.

Vol selling isn’t “dead.” But in many implementations, it has quietly flipped from mildly asymmetric to outright unfavorable.

The misconception

The common belief is that selling volatility is like selling insurance: steady income most of the time, punctuated by occasional losses that are manageable if you size correctly.

That belief rests on two flawed assumptions.

First, that the volatility risk premium is uniform across strikes and expiries. Second, that the downside can be diversified away through time.

The data no longer supports either.

What actually changed

Over the past decade, volatility selling moved from niche to industrial.

ETFs, bank QIS strategies, pension allocations, and institutional overlays have poured capital into short-volatility programs, particularly in short-dated, near-the-money options. As flows increased, the easiest-to-access premium was competed away exactly where most strategies operate.

Risk.net’s reporting highlights two structural shifts.

The first is flow concentration. Capital has not entered the options market evenly. It has clustered in specific maturities and strikes, compressing compensation in the most crowded contracts while leaving other areas less affected.

The second is payoff geometry. Selling volatility is structurally short convexity. Gains are capped by premium collected. Losses arrive through jumps, gaps, and volatility-of-volatility regimes that do not scale linearly.

That asymmetry matters far more than average returns.

The uncomfortable data

Nomura’s work, referenced in the article, shows that risk-adjusted returns from selling options vary dramatically by strike and expiry. Near-the-money options—where many “income” strategies live—have delivered materially worse Sharpe ratios than further out-of-the-money structures.

In other words, where you sell matters more than whether you sell.

The idea of a universal volatility risk premium is a myth. It comes and goes. It migrates. And when too much capital chases it, it disappears right where it’s easiest to implement.

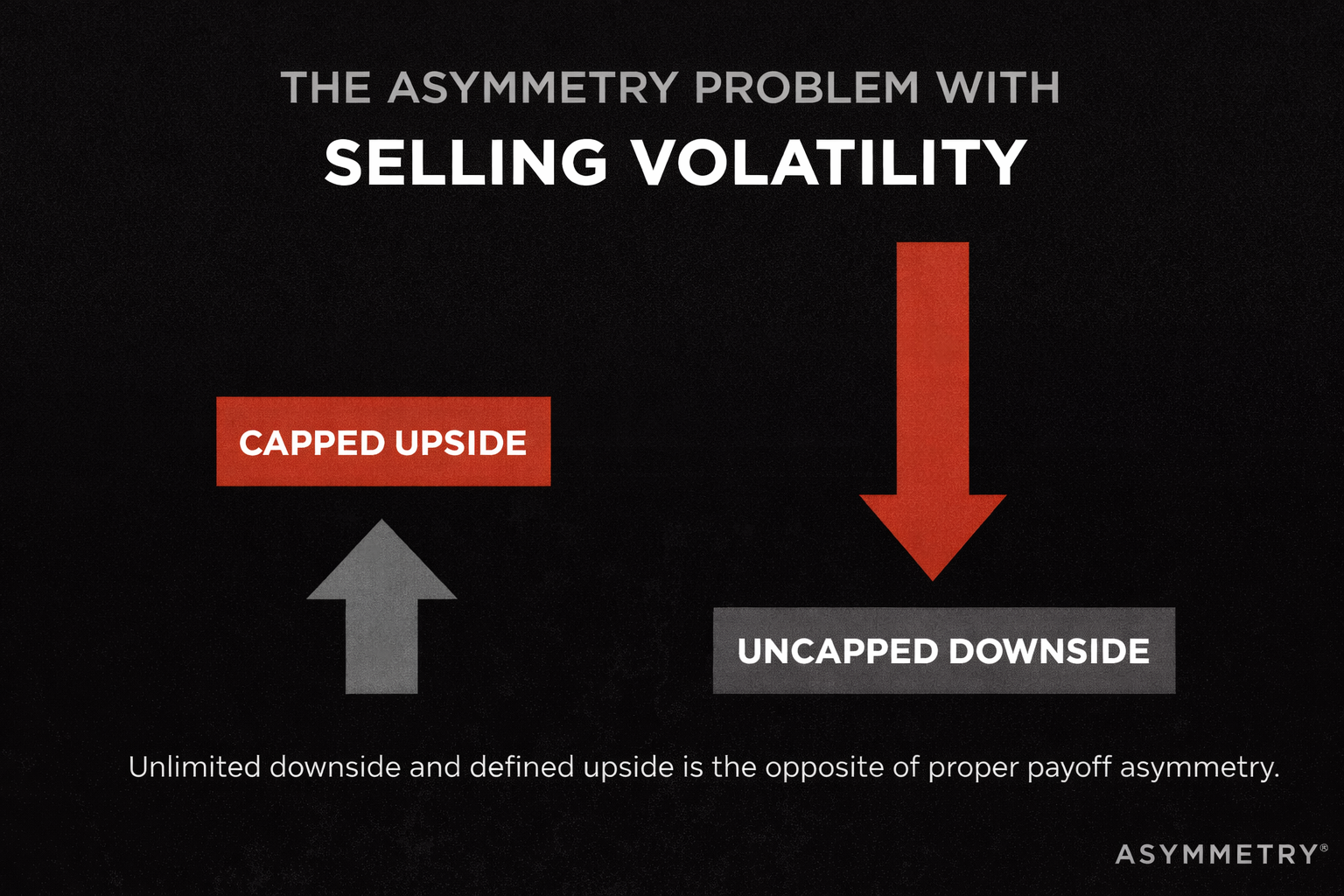

Why this is an asymmetry problem

Selling volatility offers limited upside and conditional, regime-dependent downside.

That is the opposite of convexity.

In calm markets, short-vol strategies feel stable. Dealer gamma dampens price movement. Volatility compresses. Income accrues. The trade reinforces itself—until a jump occurs.

When volatility spikes, losses are fast, correlated, and nonlinear. Liquidity thins. Hedging costs explode. What looked like a smooth income stream reveals itself as a negative convexity position that was underpaid for the risk it carried.

The asymmetry was always there. Crowding just made it worse.

What sophisticated capital is doing differently

The article hints at an important distinction.

Institutions that still engage in volatility selling increasingly treat it as tactical, not structural. They adjust strikes, expiries, instruments, and even asset classes. Some favor selling calls over puts. Others move away from equities altogether. Many insist on defined-risk structures rather than open-ended exposure.

That shift is an admission, whether stated or not, that the old “systematic income” story no longer holds.

The ASYMMETRY® perspective

From an ASYMMETRY® lens, the key question is never “does it work?”

It’s “what’s the downside geometry?”

Selling volatility without strict downside definition is a short-convexity bet dressed up as income. It may improve cash flow in benign regimes, but it degrades portfolio asymmetry precisely when protection is most valuable.

If volatility selling exists in a portfolio at all, it must be

- Explicitly sized as a risk position, not an income sleeve

- Implemented with defined downside

- Paired with convex exposures elsewhere

- Treated as opportunistic, not permanent

Otherwise, the portfolio becomes structurally exposed to the exact risks investors believe they are being paid to absorb.

The takeaway

Volatility selling isn’t broken.

But its asymmetry often is.

When capital concentration compresses compensation and the downside remains nonlinear, the trade stops being about harvesting a premium and starts being about assuming risk without being paid for it.

The edge isn’t in selling volatility.

It’s in knowing when not to.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.