The Geometry of Asymmetry

Asymmetry isn’t a feeling. It isn’t optimism. It isn’t a story about why something should work.

It’s geometry.

Every investment decision draws a shape in space. That shape defines how much you can lose, how much you can make, and how outcomes compound over time. Most investors never look at the shape. They focus on narratives, forecasts, and averages. The geometry quietly does the damage.

Asymmetry starts with a simple question: What does the payoff look like if I’m wrong versus if I’m right?

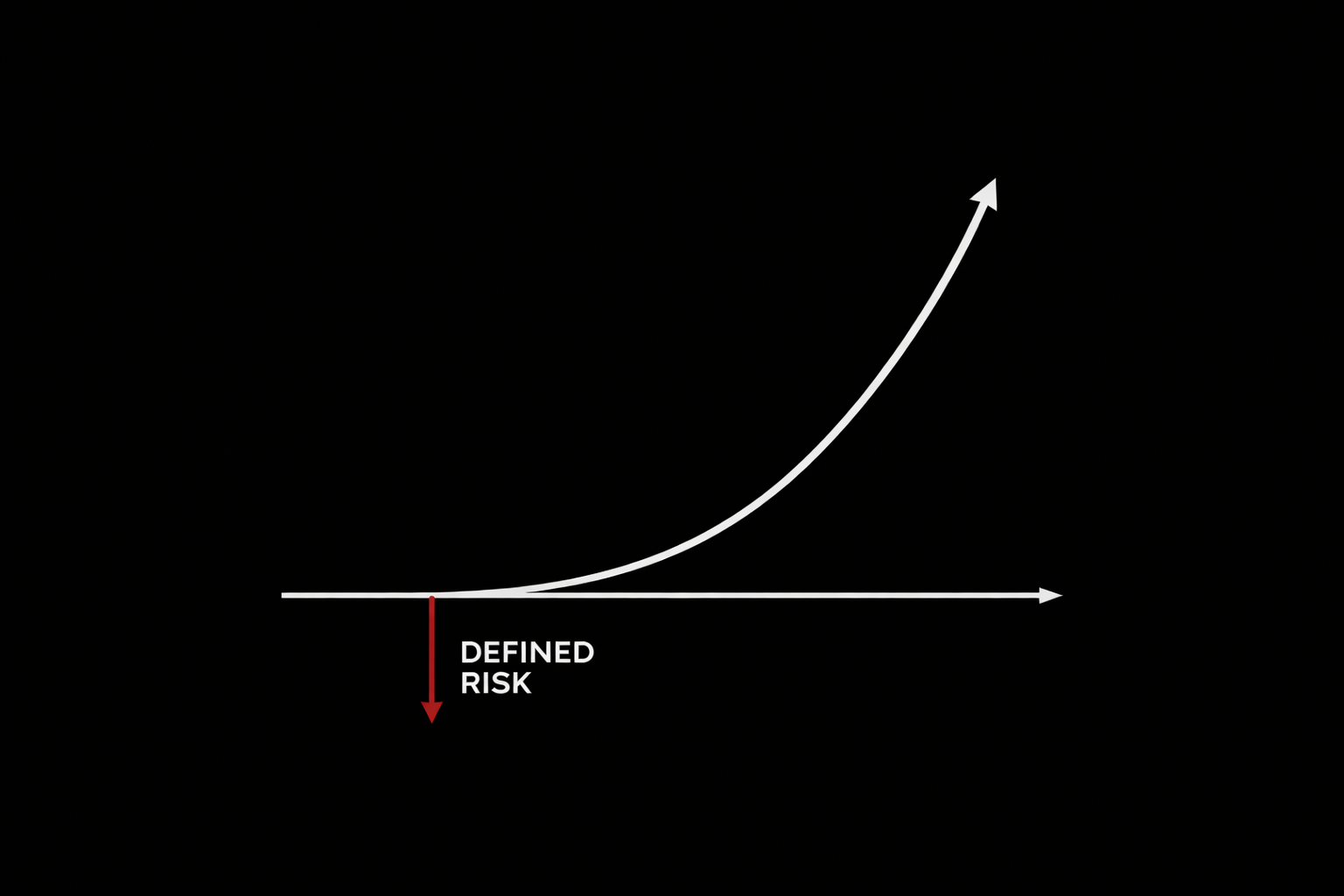

In asymmetric setups, downside is predefined and contained. Upside is open-ended or at least meaningfully larger than the loss. That imbalance isn’t philosophical—it’s mathematical. The slope of gains is steeper than the slope of losses. Over time, that geometry compounds in your favor.

Symmetric trades look harmless. They often feel “reasonable.” But their geometry is unforgiving. A 50% loss requires a 100% gain just to get back to even. That’s not bad luck. That’s math. The shape works against you even if you’re right half the time.

This is why forecasts don’t matter nearly as much as exits. The exit defines the left side of the geometry. If the left side is undefined, vertical, or ignored, the trade isn’t asymmetric—no matter how compelling the upside story sounds.

Great asymmetric decisions share a few geometric properties:

Losses are small, known, and survivable. Gains are larger, variable, and allowed to run. Position size is determined by the downside, not the upside. Time works with the position, not against it.

When those conditions are present, you don’t need to be right often. You need to be wrong small and right big. The distribution does the heavy lifting.

This is also why most portfolios quietly fail. They’re built on expected returns and correlations, not payoff geometry. They assume stability. They assume time smooths outcomes. But volatility doesn’t average out—it compounds. Bad geometry compounds faster than bad luck ever could.

Asymmetry is the discipline of refusing bad shapes.

It’s choosing structures where errors don’t kill you and success doesn’t have a ceiling. It’s designing portfolios where survival is automatic and opportunity is optionality.

When you understand the geometry, behavior changes. You stop chasing certainty. You stop needing forecasts to be precise. You stop mistaking activity for edge.

You focus on the shape. Because in markets, the shape always wins.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions. The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. The content is not intended to provide a complete description of Shell Capital’s investment process or strategies and should not be relied upon in making investment decisions. Securities, charts, indicators, formulas, or examples referenced are illustrative in nature and are not intended to represent actual client holdings or recommendations. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal. Any opinions expressed are subject to change without notice as market conditions evolve. All information is believed to be reliable but is not guaranteed and should be independently verified. Shell Capital Management, LLC, provides investment advisory services only to clients pursuant to a written investment management agreement. This material is not intended as an offer or solicitation for advisory services in any jurisdiction where such offer or solicitation would be unlawful.