The Hidden Risk in a Portfolio That Looks Diversified

Most portfolios that appear diversified aren’t actually diversified.

They’re simply holding multiple assets that trend the same way when it matters most.

Different tickers.

Different sectors.

Different labels.

But the same underlying exposure.

That distinction becomes obvious the moment volatility rises.

When liquidity tightens or risk appetite shifts, many assets that previously seemed independent suddenly begin to trend together. Correlations converge. The portfolio that once looked diversified reveals a single dominant driver.

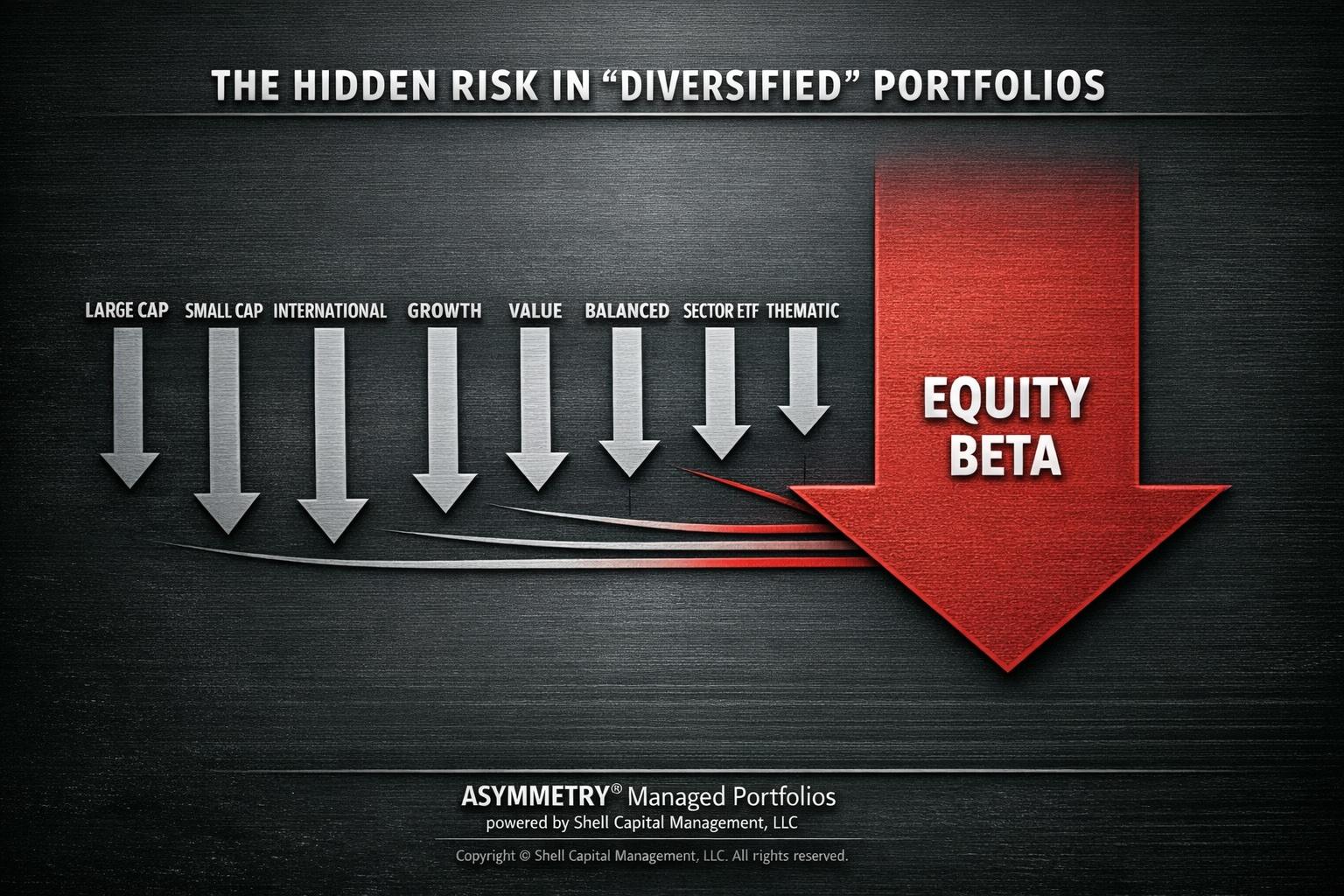

Equity beta.

It’s one of the most common structural risks in modern portfolios.

Large cap stocks, small cap stocks, international equities, growth funds, value funds, thematic ETFs, and even many “balanced” strategies ultimately share the same sensitivity to the same economic variable: the direction of the equity market.

When that dominant factor trends higher, the illusion holds.

Everything appears diversified because everything is rising.

But diversification only reveals itself during stress. When markets rotate or reprice risk, portfolios built around a single return driver experience synchronized downside.

What looked like diversification was simply concentration disguised by labels.

Real diversification requires something different.

- Different return drivers.

- Different market regimes.

- Different sources of asymmetry.

That means exposures that behave differently when conditions change, not just assets that carry different names on a statement.

True diversification is structural, not cosmetic.

It comes from combining strategies with different sources of return, different volatility profiles, and different reactions to liquidity, momentum, and market structure.

In other words, the goal isn’t to hold many assets.

The goal is to hold exposures that don’t all trend the same way at the same time.

For families responsible for meaningful capital, this distinction matters.

Because portfolio risk isn’t defined by how many positions are held.

It’s defined by how those positions behave together when markets move.

A portfolio can contain twenty funds and still have one dominant risk factor.

And when that factor trends against you, the entire structure moves with it.

That’s the hidden risk inside portfolios that appear diversified.

They aren’t diversified across outcomes.

They’re diversified across labels.

Understanding that difference is where asymmetric portfolio management begins.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.