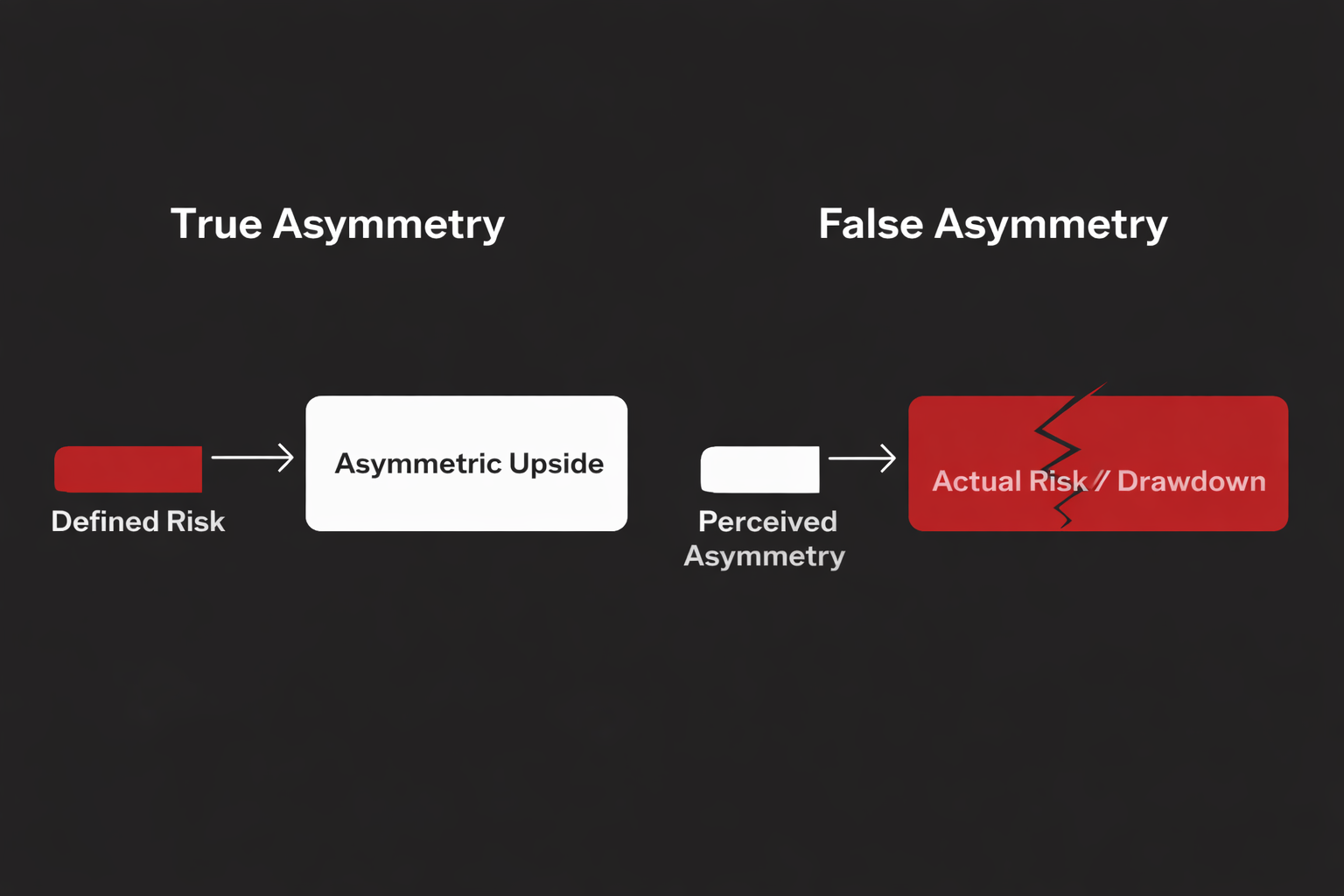

Not all asymmetry is created equal.

Some strategies look asymmetric. Others are.

The difference isn’t marketing. It’s geometry.

False asymmetry usually starts with a comforting story:

- High probability of success

- Small, steady gains

- “Defined risk” on paper

It feels conservative. It feels smart. It feels controlled.

Until it isn’t.

False asymmetry is what happens when downside is underestimated, not eliminated. When risk is capped in theory but not in reality. When losses are rare — but devastating.

That’s not asymmetry. That’s deferred risk.

True asymmetry works in the opposite direction.

True asymmetry begins with explicitly defined downside — known in advance, sized intentionally, and survivable by design. From there, upside is left open, uncapped, and allowed to compound when conditions align.

Small risk. Large optionality. No illusions.

This distinction matters more than most investors realize.

Many strategies confuse probability with asymmetry. They win often, until they don’t. They feel safe, until volatility expands. They monetize calm, and implode under stress.

True asymmetry doesn’t depend on being right frequently. It depends on never being wrong in a way that matters.

That’s the difference between strategies that survive full market cycles — and those that disappear when conditions change.

For investors who already have “enough,” this distinction is critical.

At that point, the objective isn’t squeezing out incremental return. It’s avoiding catastrophic loss while maintaining exposure to meaningful upside.

True asymmetry respects that.

False asymmetry ignores it — until markets enforce the lesson.

This is why we obsess over payoff structure, not narratives. Why we define risk before seeking return. Why we’re skeptical of anything that looks smooth, stable, and “too consistent.”

Because in markets, the most dangerous risks are often the ones that don’t show up until it’s too late.

True asymmetry isn’t exciting every day. But it endures.

And over time, endurance is the edge that matters most.

__________

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. The content is not intended to provide a complete description of Shell Capital’s investment process or strategies and should not be relied upon in making investment decisions.

Securities, charts, indicators, formulas, or examples referenced are illustrative in nature and are not intended to represent actual client holdings or recommendations. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal.

Any opinions expressed are subject to change without notice as market conditions evolve. All information is believed to be reliable but is not guaranteed and should be independently verified. Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement.

This material is not intended as an offer or solicitation for advisory services in any jurisdiction where such offer or solicitation would be unlawful.