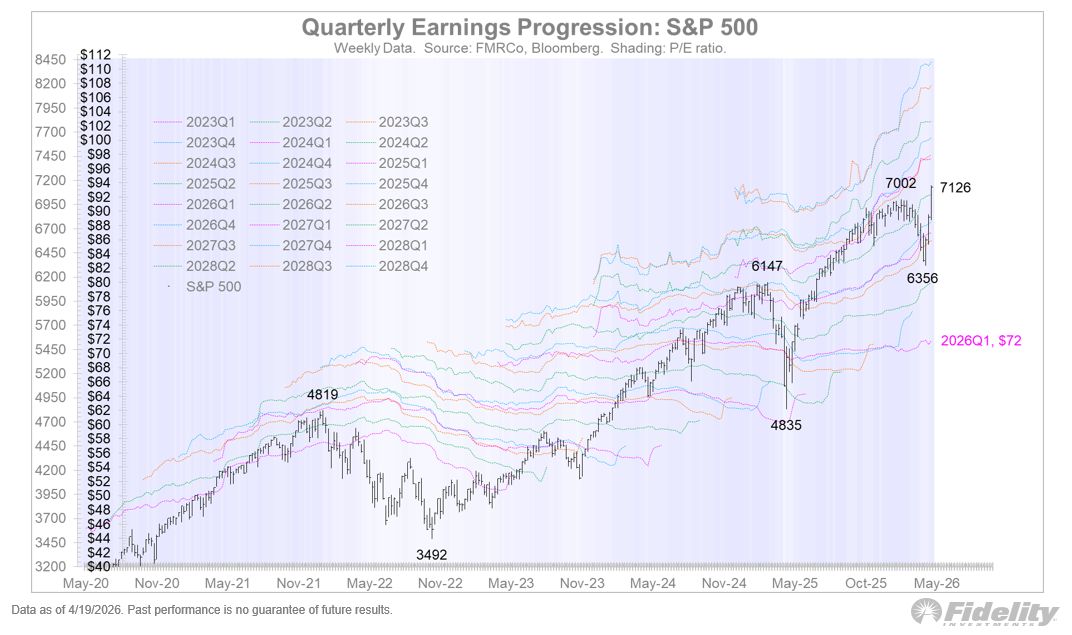

Valuation Compresses Faster Than Earnings Break

There’s a recurring mistake investors make during drawdowns: they assume price weakness means fundamentals are deteriorating.

Sometimes that’s true. But not always.

Right now, the data suggests something more specific is happening.

The market isn’t reacting to collapsing earnings. It’s repricing valuation.

The misconception

When the S&P 500 declines, most assume earnings expectations must be falling with it. That’s the intuitive narrative: price follows fundamentals.

But markets don’t move on earnings alone. They move on what investors are willing to pay for those earnings.

That’s valuation.

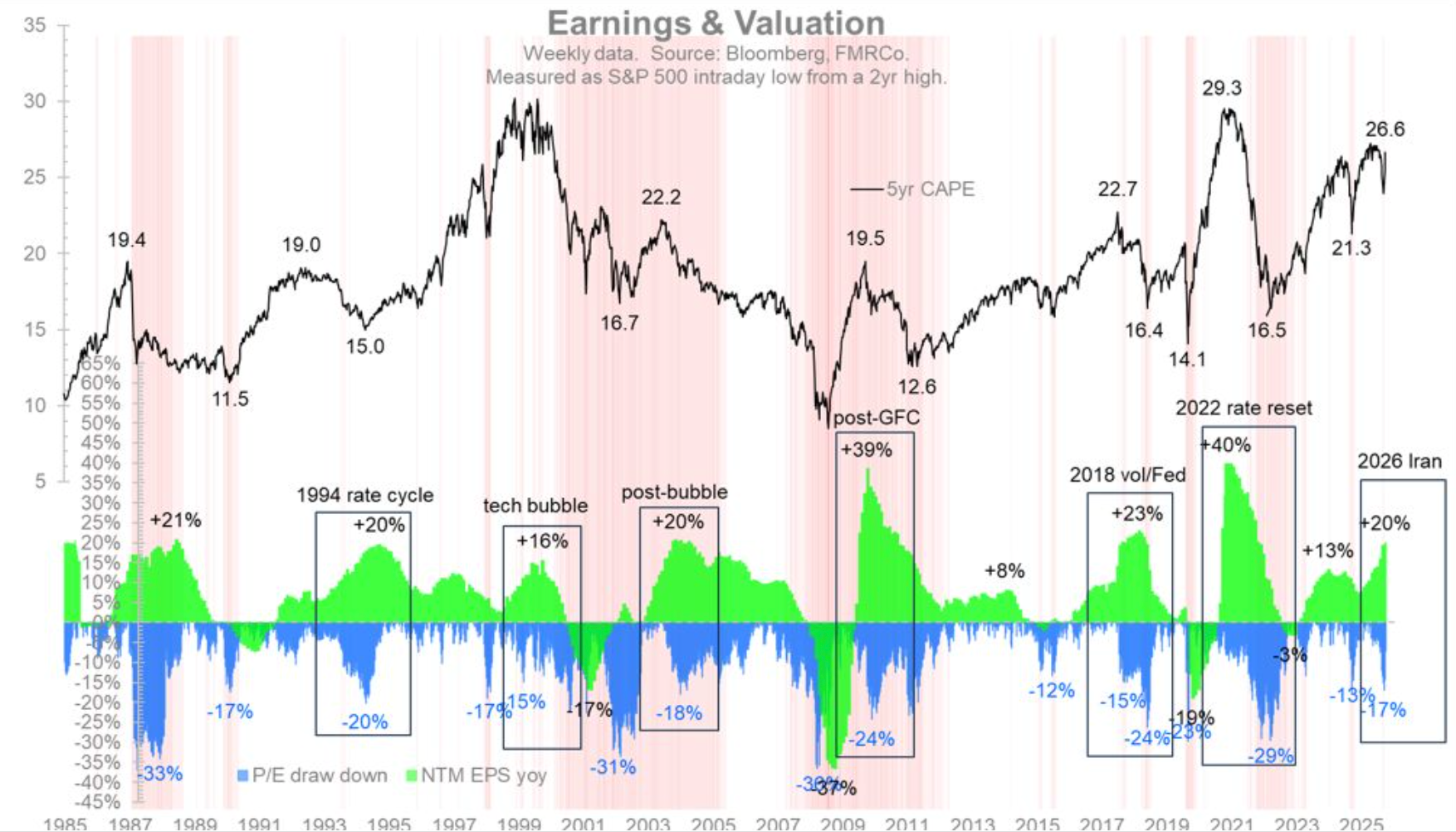

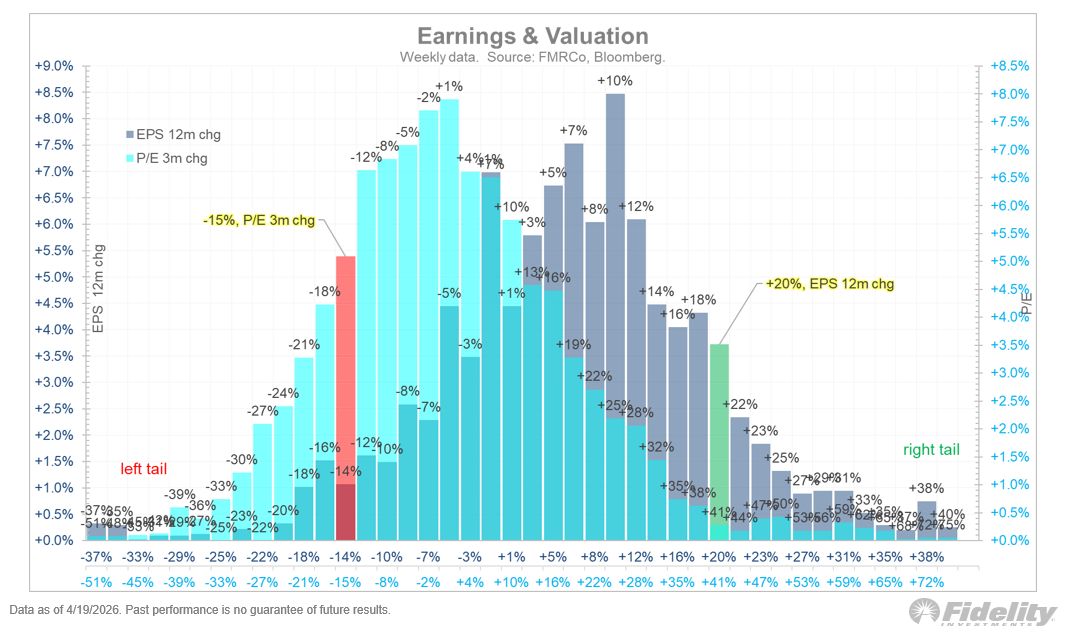

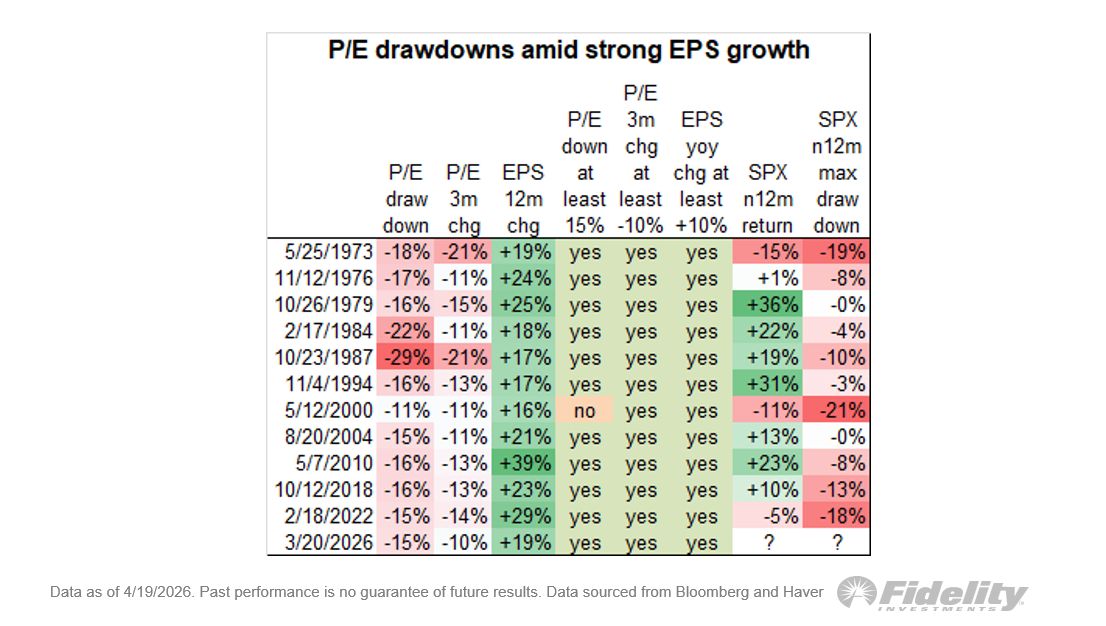

What the data shows

Historically, there have been several periods when:

- P/E multiples contracted by roughly -10% to -20%

- Earnings were still growing roughly +10% to +20%

That’s the current tension.

Valuation is in the left tail of its distribution, while earnings growth remains in the right tail.

That’s not a normal alignment. It’s a statistical mismatch between what price is doing and what earnings are doing.

Put differently: this is a right-tail earnings regime colliding with a left-tail valuation shock.

Why this matters

When valuation compresses while earnings remain intact, the forward return distribution changes.

Historically, this condition has produced positive forward 12-month returns more often than not—roughly 70% of the time in the historical sample referenced by Fidelity.

But that doesn’t mean the signal is clean.

The path is still volatile. Dispersion is wide. Downside still exists.

That’s the part investors tend to miss.

A positive base rate doesn’t eliminate risk. It changes the payoff structure.

The failure mode

The worst historical misses weren’t random.

They tended to occur when the signal appeared early in a cyclical bear market.

That matters because earnings often lag price.

In those regimes, valuation compresses first, price falls, and earnings haven’t fully caught down yet. The data can still look fundamentally resilient right before the earnings cycle deteriorates.

That’s the boundary condition.

If earnings growth rolls over from strength into contraction, the regime shifts.

Then this is no longer a valuation reset inside an earnings expansion. It becomes an earnings contraction with valuation already under pressure.

That’s a different market.

What actually drives the next move

From here, one of two things likely resolves the gap:

- Multiples stabilize and price begins to realign with earnings

- Earnings deteriorate and fundamentals catch down to price

The difference is critical.

In the first case, the right tail expands. In the second, downside risk remains open.

This is why the setup shouldn’t be reduced to “bullish” or “bearish.”

It’s more precise than that.

It’s a regime with positive expectancy, meaningful drawdown risk, and high outcome dispersion.

Implications for capital with consequences

This isn’t a prediction problem. It’s a portfolio management problem.

The edge isn’t calling direction.

The edge is structuring exposure.

That means defining downside in advance, sizing positions relative to that downside, and maintaining participation if the right tail starts to express.

This is where ASYMMETRY® functions as an operating system.

Not by assuming the market must recover.

Not by pretending risk has disappeared.

But by recognizing when risk and reward have started to redistribute.

Closing perspective

Price can fall even when earnings are strong.

But when price falls faster than earnings break, the return profile can become more asymmetric.

Not because downside goes away.

Because the market may have already repriced a meaningful amount of risk before the fundamental trend has failed.

That’s the distinction.

And it’s where disciplined portfolio management matters most.

In my own process, this is the type of environment I pay close attention to—not because it’s automatically bullish, but because the relationship between valuation and earnings starts to shift. When price declines faster than fundamentals, the question isn’t where the market goes next. It’s whether downside is becoming more defined relative to the remaining upside. That’s where position sizing, exit discipline, and portfolio risk control matter most.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.