Valuation Extremes and the Compression of Asymmetry

When valuations move to statistical extremes, the forward return distribution shifts.

That’s the core issue.

Multiple long-term measures — market cap to GDP, CAPE, price-to-sales, mean reversion composites — are currently more than +2 standard deviations above trend. That doesn’t tell us when prices will decline. It tells us the starting point.

And starting point matters.

Valuation is not a timing tool. It’s a distribution tool. High starting multiples tend to compress future return potential and expand downside tail exposure. Low starting multiples tend to expand upside convexity and compress left-tail risk.

That’s asymmetry.

At elevated valuation levels, the margin of error narrows. You are paying more today for the same stream of future cash flows. That reduces expected forward returns as a mathematical function, not as an opinion.

This is what that distribution shift looks like empirically.

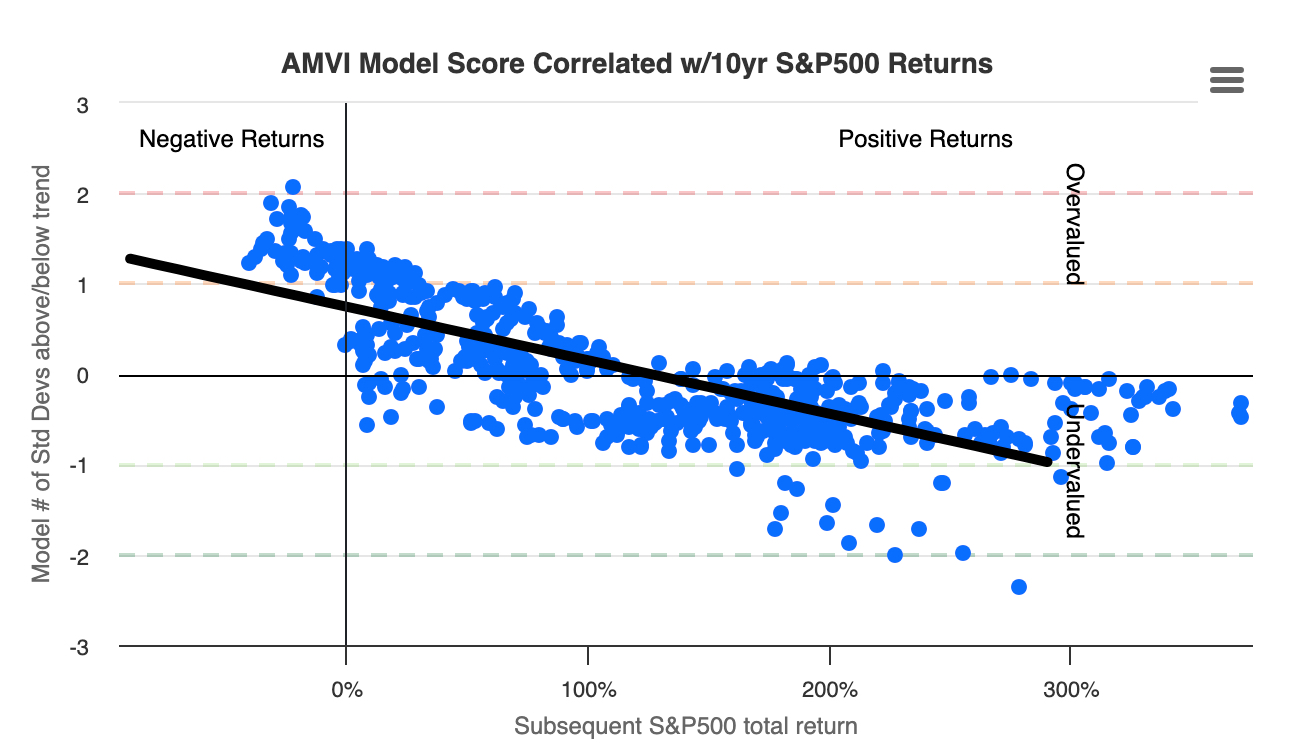

The current market valuation scatterplot plots a composite valuation measure against subsequent 10-year S&P 500 returns. Every instance of negative 10-year returns occurred when starting valuations were materially above trend. Conversely, deeply undervalued starting points were followed by strong forward returns. With an R² near 0.58, valuation explains a meaningful portion of long-horizon return variance.

That does not mean overvaluation triggers immediate decline. Trend, liquidity, and behavioral momentum operate on shorter clocks. Markets can remain extended for longer than models suggest.

But over long horizons, gravity asserts itself.

Notice something more subtle: the strongest forward returns did not come from extreme undervaluation. They came from modest undervaluation. Markets rarely offer “perfect” entry conditions. Capital often must be deployed when asymmetry improves — not when it looks pristine.

For families and business owners managing capital with consequences, the implication is structural.

When valuation asymmetry deteriorates:

Upside convexity compresses. Left-tail exposure expands. Return expectations should moderate.

The response isn't a prediction. It is portfolio management.

Define the downside in advance. Size exposure relative to volatility and regime. Monitor portfolio risk as a percentage of total equity. Allow trends to persist, but do not assume permanence.

Extreme valuation doesn't equal imminent decline. It equals thinner margins of safety.

Overvaluation doesn’t tell you when. It tells you how much risk you are being compensated to take.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.