What Stanley Druckenmiller Actually Means by "Rate of Change" — And Why It's the Foundation of Asymmetric Risk Management

Most investors watch price and call it analysis. More sophisticated investors watch momentum. Very few monitor the change in momentum itself — the acceleration, the second derivative, the variable that often shifts before price confirms anything.

That distinction isn’t academic. It’s structural. It separates reactive capital from anticipatory capital — and it’s often the difference between participating in markets and managing risk through them.

What Druckenmiller Is Actually Doing

When investors hear Stanley Druuckenmiller talk about “rate of change,” the common assumption is that he’s simply tracking direction in economic data. Growth up is good. Growth down is bad.

That’s not the edge.

In a public interview, Druckenmiller was specific about what he uses:

“The charts we use… because it used second derivative rate of change, these things will often bottom a year to a year and a half before the fundamentals, so they’ll give you time to study the thesis.”

Read that carefully.

He isn’t describing prediction in the usual sense. He isn’t claiming to forecast GDP or earnings with precision. He is describing acceleration — the second derivative, the change in the rate of change — and a framework that can identify inflection before fundamental data visibly confirm it.

That is a structural advantage embedded in how markets reprice expectations.

He’s not trading the level. He’s trading the inflection in force.

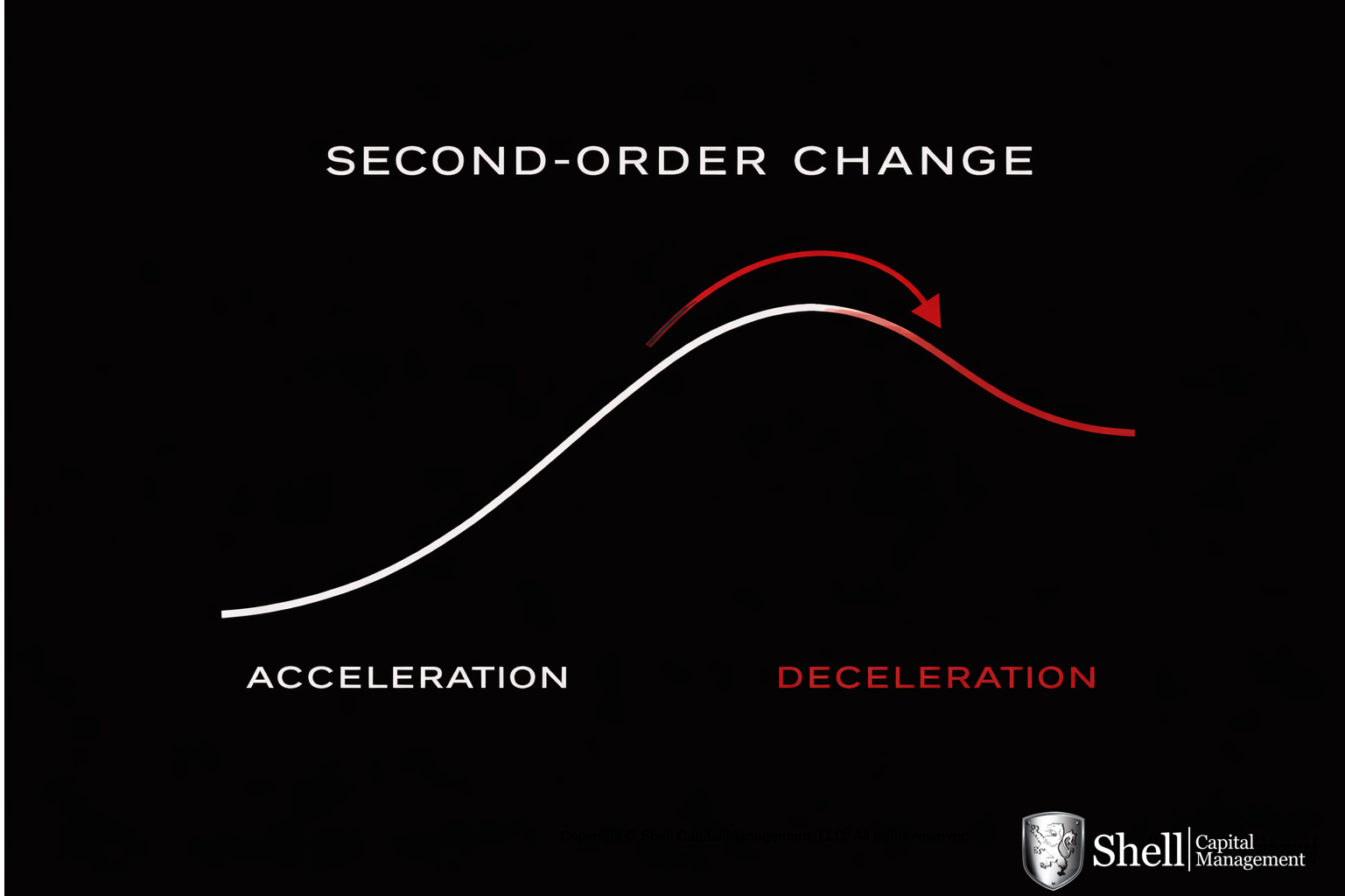

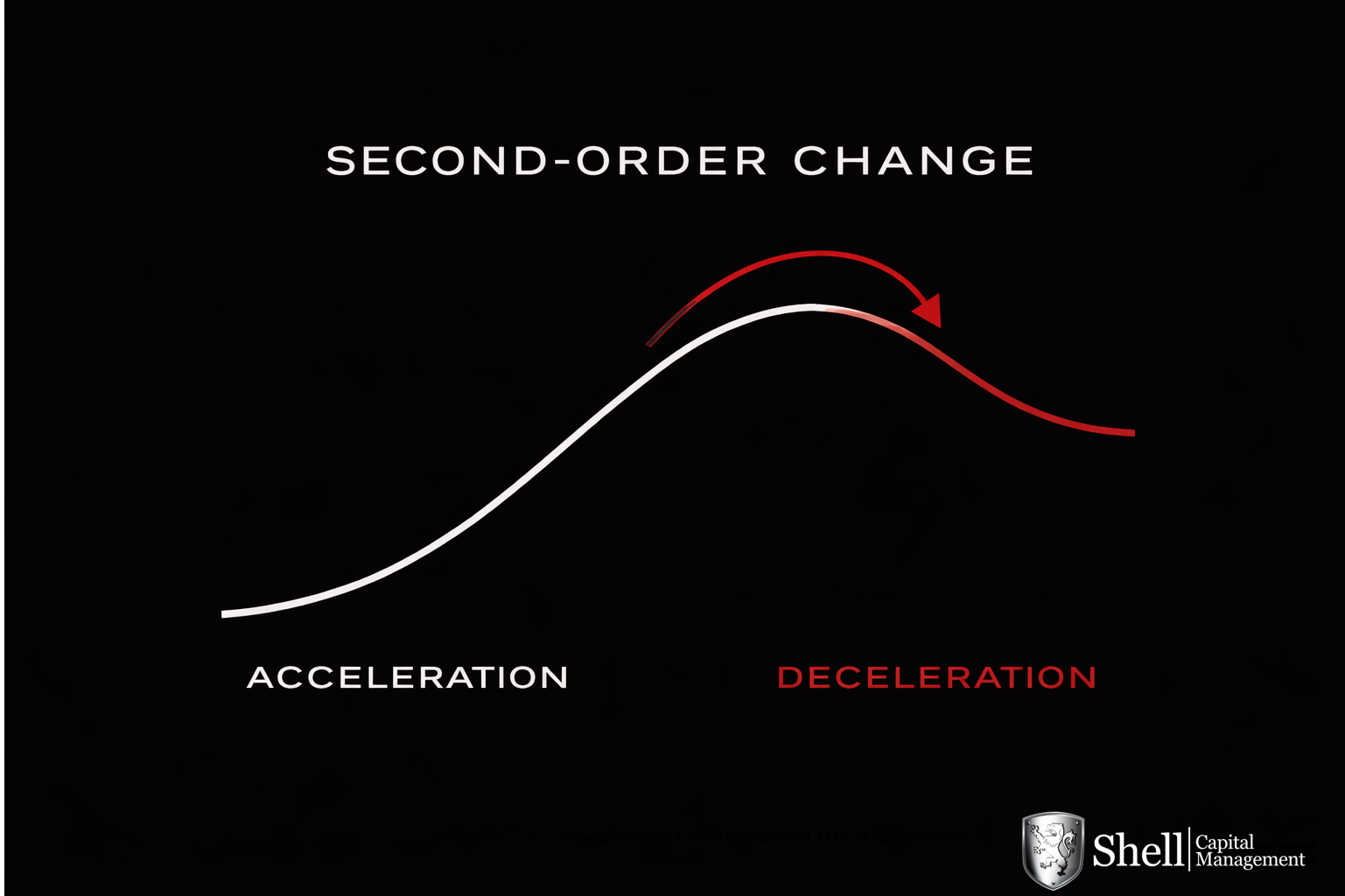

First-Order vs. Second-Order

First-order change tells you direction: Growth is rising. Inflation is falling. Earnings are improving.

Second-order change tells you whether that direction is strengthening or weakening: Is growth still rising — but at a slower pace? Is inflation falling faster — or beginning to flatten? Are earnings expanding — but with diminishing momentum?

The difference matters because markets are forward-looking auction systems. Capital reallocates based on expectations, not current conditions. When improvement decelerates, the marginal buyer becomes less aggressive. Buying enthusiasm moderates. Risk premiums begin adjusting quietly, before headlines turn.

By the time the data visibly roll over, price has often already moved.

This isn’t theoretical. In prior cycles, fundamental aggregates remained “acceptable” even as acceleration had already peaked and turned. In those cases, second-order change preceded broad consensus by enough time to matter — and enough time to act.

Second-order analysis captures that shift earlier — not because the information is secret, but because the variable being tracked is different.

The Physics of Markets

Think of market structure in terms of motion.

Price is position: where the market is. Momentum is velocity: how fast it’s moving. Second-order change is acceleration: whether that velocity is increasing or fading.

Markets rarely reverse from maximum strength. They reverse after strength begins to decelerate. That deceleration is where the probability distribution quietly widens — often while price still appears stable, while the headlines are still constructive, while confidence is still high.

The wave can look strongest just before it breaks.

Acceleration shifts first. Expectations adjust next. Price follows.

That sequence is structural, not theoretical. It repeats across asset classes, time frames, and market cycles because it reflects how participants — responding to changing fundamentals and changing confidence — reposition capital.

What Acceleration Looks Like in Practice

The principle manifests in measurable ways.

RSI, properly understood, isn’t simply an overbought/oversold label. It’s an asymmetry measure: RS equals average gain divided by average loss over a lookback period. Above 50, buying demand dominates selling pressure. Below 50, losses dominate gains.

But the absolute level isn’t the earliest signal.

The earlier signal is whether that dominance is strengthening or fading. Whether RSI is accelerating into a gain-dominant regime — or rolling over while price still appears strong. Whether trend force, as measured by ADX, is expanding, confirming organized demand — or compressing as momentum quietly loses conviction. Whether volatility is contracting beneath orderly price action — or beginning to expand beneath sideways price that looks calm on the surface but masks growing disagreement.

A healthy, sustainable uptrend typically shows: Sustained gain dominance in RSI (buyers in control) Rising ADX (trend force expanding, not exhausting) Contained volatility (organized, directional movement)

Before reversals, what changes first is not price. It’s velocity.

Gains shrink relative to losses. Retracements deepen. ADX compresses as trend force fades. Volatility begins expanding while price lingers near highs — the market disagreeing internally before that disagreement shows on the tape.

That’s the second derivative turning. Instability building beneath apparent stability. The structural fingerprint of a regime preparing to shift.

Second-order change doesn’t predict direction with certainty. It signals transition. And transitions are where asymmetric opportunity can exist — for those positioned to recognize them early.

Why This May Have Genuine Predictive Power

Structure precedes outcome.

Participants driving price respond to changing fundamentals, changing positioning, and changing confidence. When economic acceleration slows, informed capital often repositions quietly. When momentum in market structure decelerates, active managers may reduce risk before the obvious signal appears.

By the time a breakdown is confirmed, repricing is frequently already underway. The investor waiting for price to break is not exiting at the turn — they’re exiting after the repricing has progressed.

Monitoring acceleration doesn’t manufacture certainty. It provides earlier evidence — when decisions are still relatively inexpensive, when exposure can be reduced at cost rather than at crisis.

That asymmetry in timing is one of the structural advantages.

The Limits of Second-Order Thinking

Intellectual honesty requires stating boundary conditions plainly.

Deceleration can persist for extended periods in low-trend, sideways environments. Low-ADX regimes can produce false breaks. Volatility expansion can resolve in either direction. Second-order change does not predict the exact path forward — it indicates that the prior regime’s assumptions are weakening and that the distribution of potential outcomes is widening.

The edge isn’t prediction. It’s recognizing when the probability distribution is widening — and structuring exposure to reflect that broader range of outcomes rather than anchoring to the prior regime’s parameters as though they still hold.

That is structural engineering. Not forecasting. Not “market timing” in the pejorative sense. Disciplined response to structural evidence.

What This Means for Capital with Consequences

The largest drawdowns rarely begin at moments of obvious weakness. They begin when strength quietly loses acceleration.

For founders, physicians, executives, and families stewarding meaningful capital — wealth built over decades that cannot be easily rebuilt — this has consequences that compound. A 40% loss requires a 67% gain just to recover. That mathematics is unforgiving. And the behavioral cost of enduring a severe drawdown — decisions made under stress, anchoring to prior highs, paralysis when action is most needed — can be as damaging as the financial loss itself.

Monitoring second-order change supports a more institutional approach:

Reduce exposure when momentum decelerates and volatility expands. When the fingerprints of deceleration are visible — RSI rolling, ADX compressing, volatility beginning to widen — the probability distribution has already shifted. Reducing exposure at that stage isn’t guessing direction. It’s responding to evidence while the cost of doing so is still manageable.

Avoid oversizing into decelerating trends. Investors often increase conviction precisely when trends feel strongest — often when underlying acceleration is already fading. The trend can feel most certain just as it becomes most fragile. Second-order analysis corrects that bias by revealing what price alone can conceal.

Increase convex exposure when re-acceleration begins. The same framework that identifies deterioration can also identify renewal. When volatility compresses after turbulence and momentum begins rebuilding with expanding ADX, a new expansion regime may be forming. The asymmetric opportunity is sizing up before the breakout is obvious — when the structural evidence is present but consensus has not yet confirmed it.

The ASYMMETRY® Perspective

Druckenmiller’s framework — in his words, signals that “will often bottom” well ahead of fundamentals — isn’t magic. It’s a logical consequence of tracking a variable many participants ignore.

Edge doesn’t come from knowing the future better than everyone else. It doesn’t come from superior forecasting, better data, or faster news. It comes from recognizing when the internal force of the system is changing — and adjusting exposure before that change becomes consensus.

Most investors react to levels. More sophisticated investors track momentum. The structural advantage lives one layer deeper: acceleration.

Acceleration shifts first. Expectations adjust next. Price follows.

Druckenmiller said his framework could provide time to “study the thesis” before fundamentals visibly confirm the turn. That window is not a promise and not a prediction. It’s an opportunity to reassess exposure while markets still offer liquidity and before consensus reprices risk.

The last signal is the one everyone can see. By then, the cost of waiting has already compounded.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.