When No One Is Short Volatility, Where Is the Convexity?

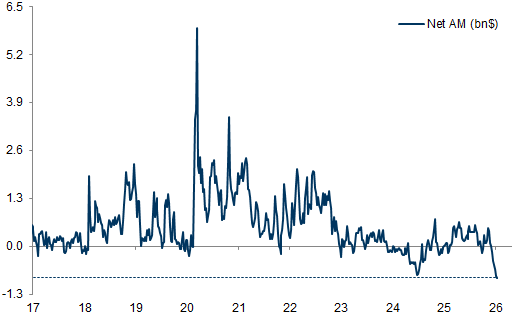

Asset managers’ net short VIX positioning has collapsed to extremely low levels. That matters because volatility spikes tend to become explosive when investors are structurally short and forced to cover. If that crowding isn’t present, the reflexive fuel for a volatility surge may be smaller. The asymmetry in tail-risk trades shifts when positioning shifts.

Asset managers' short VIX positioning has shifted down and is now extremely low.

Net positioning of asset managers, in billion $. Source: Haver Analytics, CFTC, Goldman Sachs Global Investment Research

Net positioning of asset managers, in billion $. Source: Haver Analytics, CFTC, Goldman Sachs Global Investment ResearchThis chart tracks net VIX futures positioning by asset managers using CFTC data. For years, institutional investors were structurally short volatility. It was carry. It was comfort. It was the dominant regime.

Now that short positioning has compressed toward zero — even dipping modestly long — the structure of the volatility market has changed.

The common misconception

Many investors assume low VIX equals complacency. They assume suppressed volatility automatically creates asymmetric upside in volatility.

But asymmetry isn’t about the level of an index. It’s about positioning.

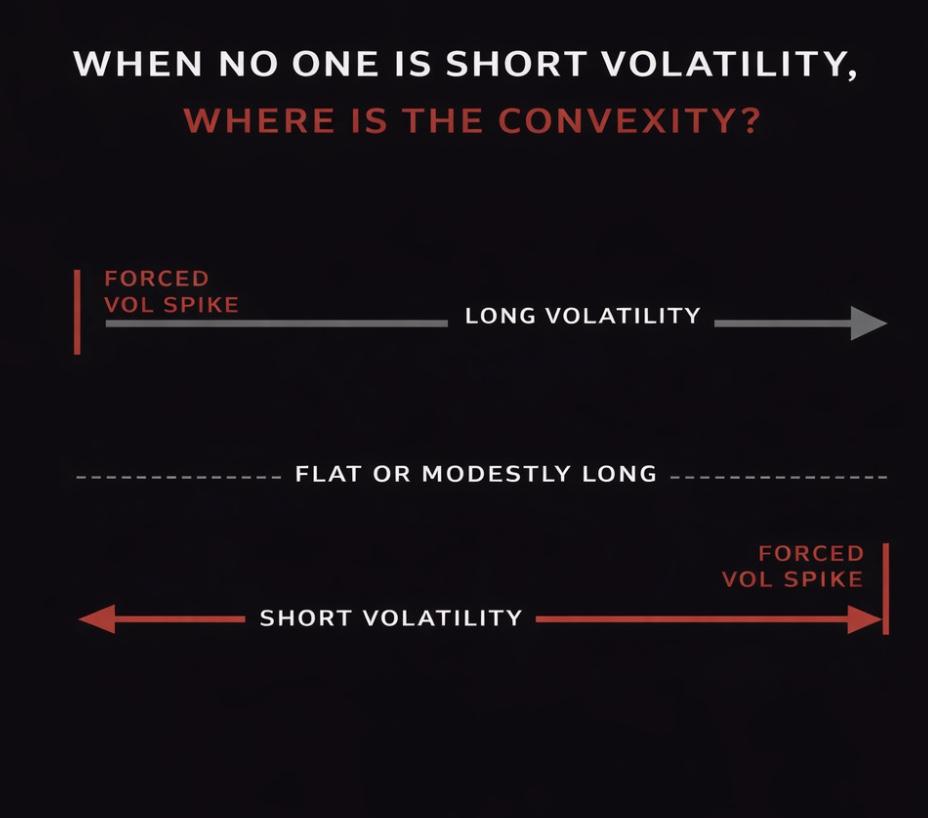

If everyone is already short volatility, you have embedded convexity. A volatility spike forces covering. Covering begets more volatility. That reflexivity is fuel.

If no one is meaningfully short, that fuel isn’t there.

First-principles correction

Volatility convexity comes from imbalance.

When asset managers are heavily net short VIX: – Short vol is consensus – Equity exposure is comfortable – A volatility spike can trigger mechanical buying

When positioning is flat or modestly long: – There is less forced-covering risk – Volatility spikes rely more on exogenous catalysts – The payoff geometry shifts

Right now, asset managers are not structurally leaning short. That removes one layer of embedded asymmetry in long-volatility trades.

This doesn’t mean volatility cannot spike. It means the structural accelerant from crowded short positioning appears smaller than in prior cycles.

Boundary conditions and failure modes

Positioning is one lens, not the only lens.

Dealer gamma, systematic volatility targeting, CTA trend exposure, and options skew all interact with VIX futures positioning. A macro shock can override positioning dynamics. Structural complacency can rebuild quickly.

But as of now, the structural short-vol consensus that defined prior regimes is not evident here.

Capital implications for families and founders

For capital with consequences, tail risk management isn’t about reacting to headlines. It’s about engineering convexity where it exists — and avoiding paying for convexity that isn’t structurally supported.

If no one is short volatility, buying volatility as a reflex may offer a different expected value profile than in a crowded short-vol regime.

This is why we don’t hedge mechanically.

We define portfolio risk first. We quantify total open risk as a percentage of equity. Then we assess whether the volatility complex offers positive expectation for convex overlays, or whether capital is better allocated elsewhere.

Asymmetry is structural. It isn’t emotional.

Conclusion

Volatility convexity is most powerful when positioning is one-sided. Today, asset managers’ VIX positioning suggests the crowd is not aggressively short.

That changes the geometry.

The question isn’t “Will volatility rise?” The question is “Where is the imbalance?”

As always, we engineer asymmetric risk/reward by aligning positioning structure, defined downside, and convex payoff potential — not by chasing fear or calm.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.