When Return Drivers Concentrate: The Hidden Risk Inside “Diversified” Trend Portfolios

I often say, "It doesn't matter how much the return is if the drawdown is so high you tap out before it's achieved." That simple truth applies to every investment strategy. And the same can be said for broad diversification—even inside a systematic, trend-following trading system.

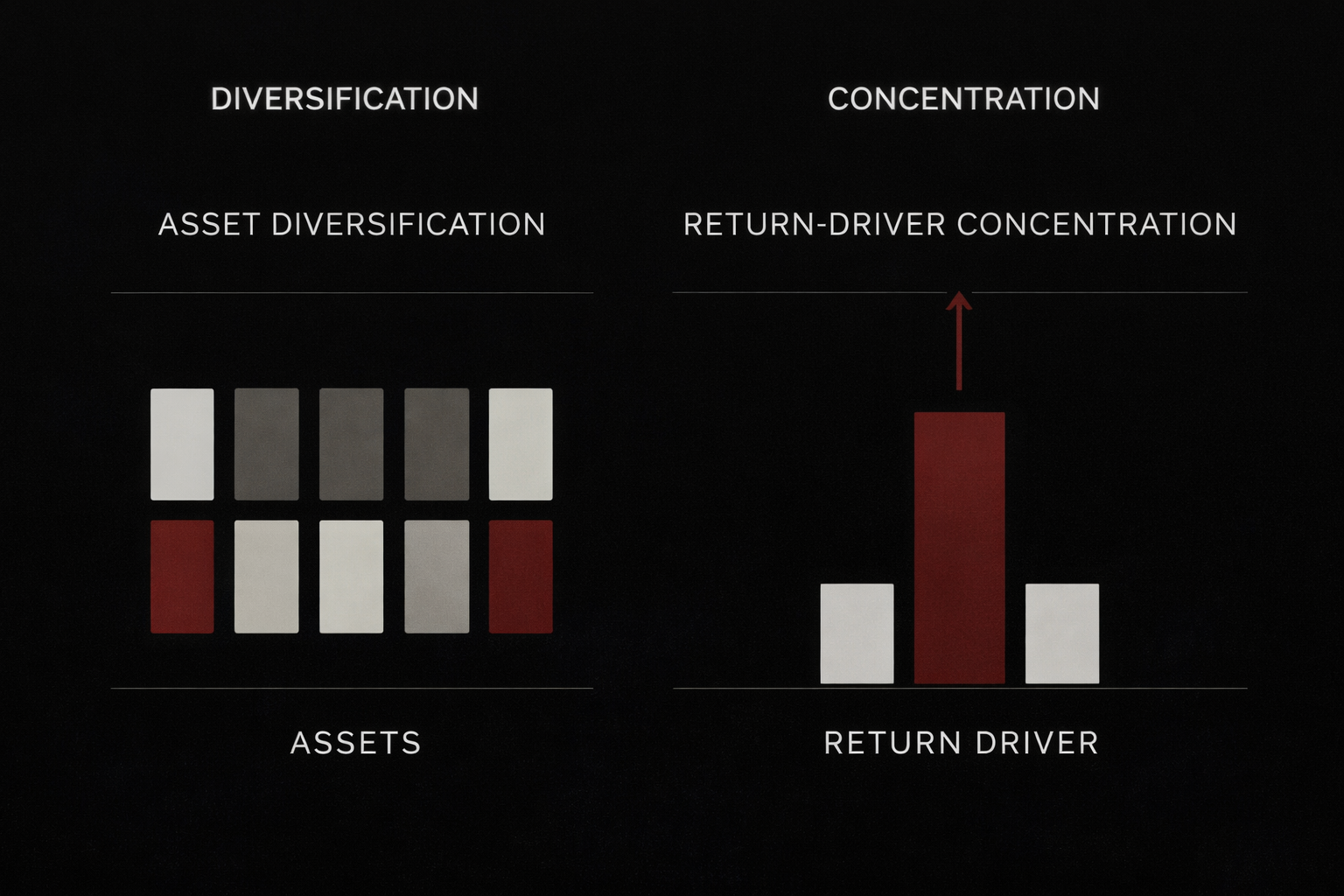

Diversification is often treated as a form of risk control. More markets. More assets. More lines in the portfolio. The assumption is that breadth itself limits drawdowns.

But diversification by asset count doesn’t control risk when return drivers concentrate.

Trend-following systems don’t allocate risk evenly across assets. They allocate risk to what is trending. When multiple markets are responding to the same underlying force — liquidity, inflation expectations, policy shifts, currency trends — the portfolio may look diversified while being structurally exposed to a single return driver.

That’s exactly what Friday’s drawdown revealed.

The portfolio wasn’t broadly wrong. It was locally concentrated.

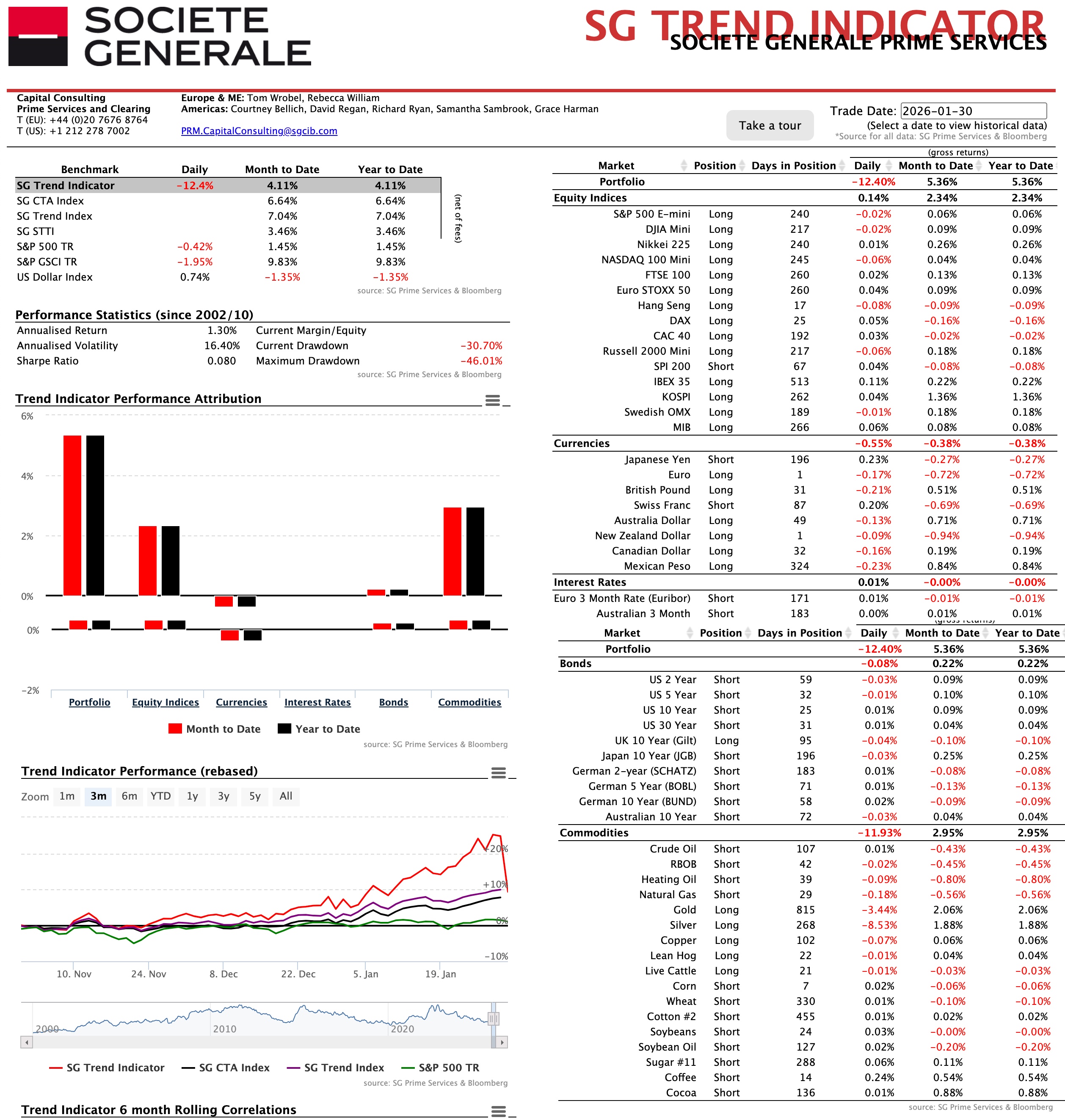

On Friday, Societe Generale’s SG Trend Indicator fell -12.40% in a single day.

On Friday, Societe Generale’s SG Trend Indicator fell -12.40% in a single day.

At first glance, that looks impossible. The model is diversified across equities, currencies, rates, bonds, and commodities. Dozens of markets. Longs and shorts. Different geographies. Different instruments.

And yet, it still experienced a violent one-day drawdown.

That wasn’t a diversification failure. It was a return-driver concentration event.

The Trend Indicator is not diversified by asset count. It’s diversified by trend. And when trends cluster, so does risk.

The dominant return driver that day was long precious metals, specifically gold and silver. Both had been long-duration positions — gold for over two years, silver for nearly a year. Those positions weren’t incidental. They were core contributors to the model’s recent gains.

When that return driver reversed sharply, the losses overwhelmed the rest of the portfolio.

Gold fell hard. Silver fell harder. Everything else barely mattered.

Equities were slightly positive. Rates were flat. Currencies were mixed. Energy shorts helped, but not enough. The book wasn’t broadly wrong — it was locally exposed.

This is the part most investors miss.

Trend systems don’t diversify risk evenly across assets. They allocate risk to what is trending. When multiple markets express the same underlying force — inflation, liquidity, currency debasement, real-rate compression — diversification collapses at the driver level, not the asset level.

Gold and silver weren’t two different bets. They were the same bet, expressed twice, with silver carrying higher velocity.

That’s why the drawdown was sharp.

It’s also why this isn’t an indictment of trend following.

This is how trend systems are supposed to behave. They accept episodic convex losses in exchange for long-duration asymmetry. They don’t smooth returns. They surface regime shifts violently.

But it does expose the real risk investors take when they think diversification is about the number of line items instead of the geometry of exposure.

For high-net-worth portfolios, the lesson isn’t “avoid trend.” It’s “understand your return drivers.”

If multiple positions depend on the same macro force, policy regime, or liquidity condition, your portfolio is not diversified — no matter how many markets you hold.

Asymmetry isn’t about always being right. It’s about knowing where you’re exposed when you’re wrong.

That’s what Friday revealed.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.