When the Hedge Stops Hedging

For decades, investors have been told that diversification solves the problem.

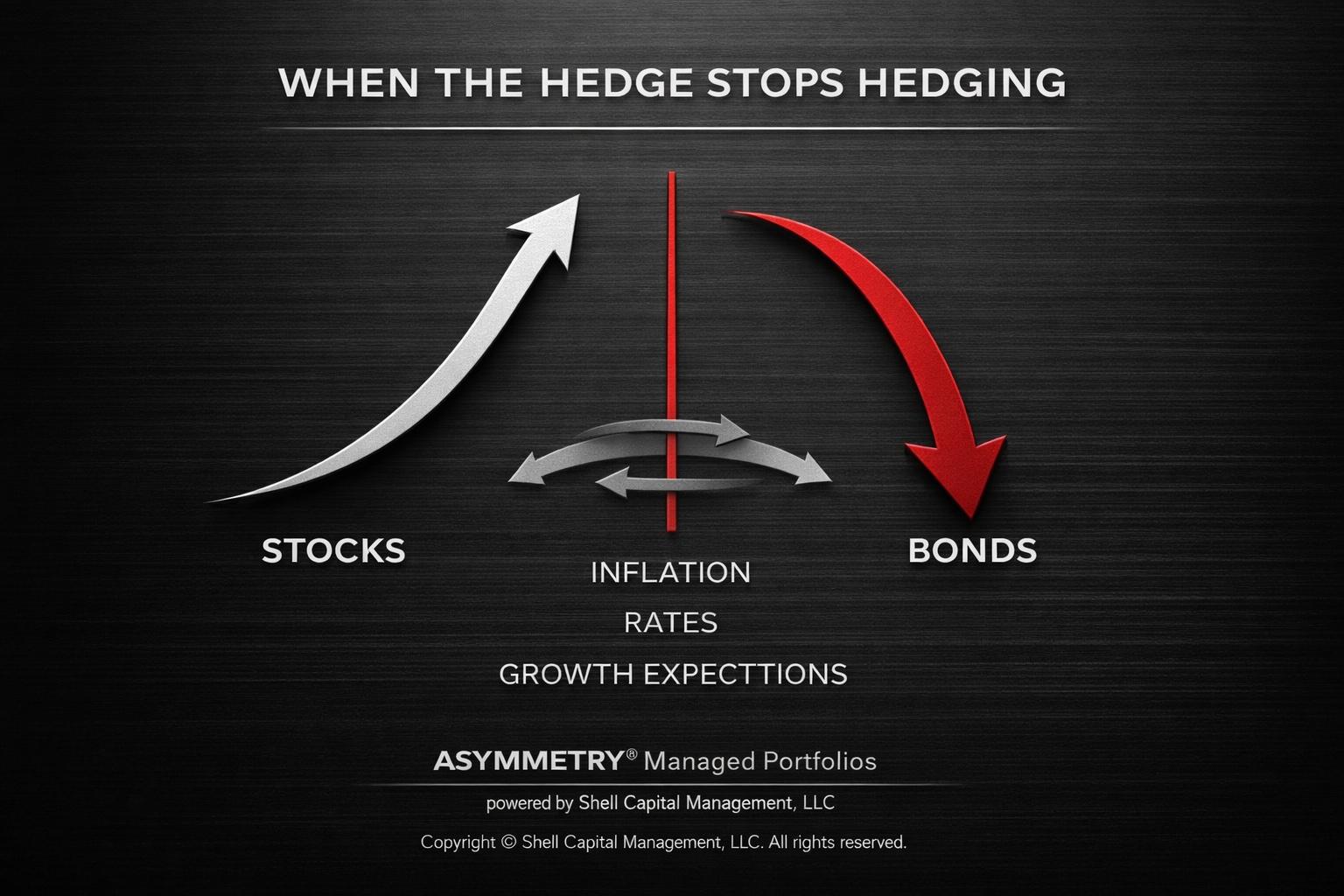

Stocks provide growth.

Bonds provide protection.

When equities decline, bonds are supposed to cushion the fall.

But that relationship isn’t a law of nature. It’s a regime.

And regimes change.

Recent cross-asset research from Goldman Sachs highlights a subtle but important shift: the sensitivity of equities to real interest rates and inflation expectations has turned sharply negative.

That may sound technical, but the implication is simple.

The forces moving the bond market are increasingly the same forces moving equities.

When that happens, the hedge investors rely on can quietly stop working.

The Assumption Behind the Classic Portfolio

Most portfolios are built on a simple premise.

Stocks and bonds tend to move differently.

When growth weakens and equities fall, central banks cut rates. Bond prices rise. Losses in equities are partially offset.

That relationship powered the classic 60/40 portfolio through decades of declining inflation and falling interest rates.

But that environment was historically unusual.

When inflation and policy expectations dominate the macro regime, both asset classes can respond to the same shock.

And when they do, diversification becomes more fragile than investors expect.

When Correlations Change

The recent repricing in policy expectations has been one of the sharpest hawkish shifts in more than two decades.

Markets have rapidly adjusted expectations for central bank policy across major economies.

But growth expectations have not repriced to the same degree.

That creates a tension inside portfolios.

If policy expectations drive both rates and equity valuations, the traditional offset between stocks and bonds weakens.

Bonds may still move, but not enough to provide the buffer investors assume.

The result is subtle but important.

The structure of the portfolio becomes more exposed than it appears.

The Risk Most Portfolios Don’t Measure

Most investors think risk is volatility.

But volatility isn’t the real problem.

Correlation is.

Two assets can look diversified on paper, yet behave similarly when the underlying driver of returns changes.

When inflation, rates, and policy expectations become the dominant market forces, the distinction between “risk assets” and “defensive assets” can blur.

That’s why some of the largest portfolio drawdowns occur when correlations shift unexpectedly.

The hedge doesn’t disappear overnight.

It slowly weakens until the moment investors need it most.

What This Means for Families With Meaningful Capital

For business owners, founders, and families responsible for preserving significant wealth, the lesson isn’t to predict the next Fed decision.

It’s to recognize that portfolio management matters more than forecasts.

Markets constantly move between regimes.

Growth-driven regimes.

Inflation-driven regimes.

Liquidity-driven regimes.

The relationships between assets change with them.

Managing capital in that environment requires more than static diversification.

It requires actively monitoring trends, volatility, liquidity, and correlations — and adjusting exposures when the regime shifts.

Because the most dangerous risk in a portfolio is often the one hidden inside the assumptions it was built on.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.