Why Record Demand for 30-Year Treasuries Matters

Summary: Record demand for 30-year U.S. Treasuries signals how sophisticated capital views inflation, growth, and risk. Here’s why it matters for long-term portfolio construction and asymmetric risk management.

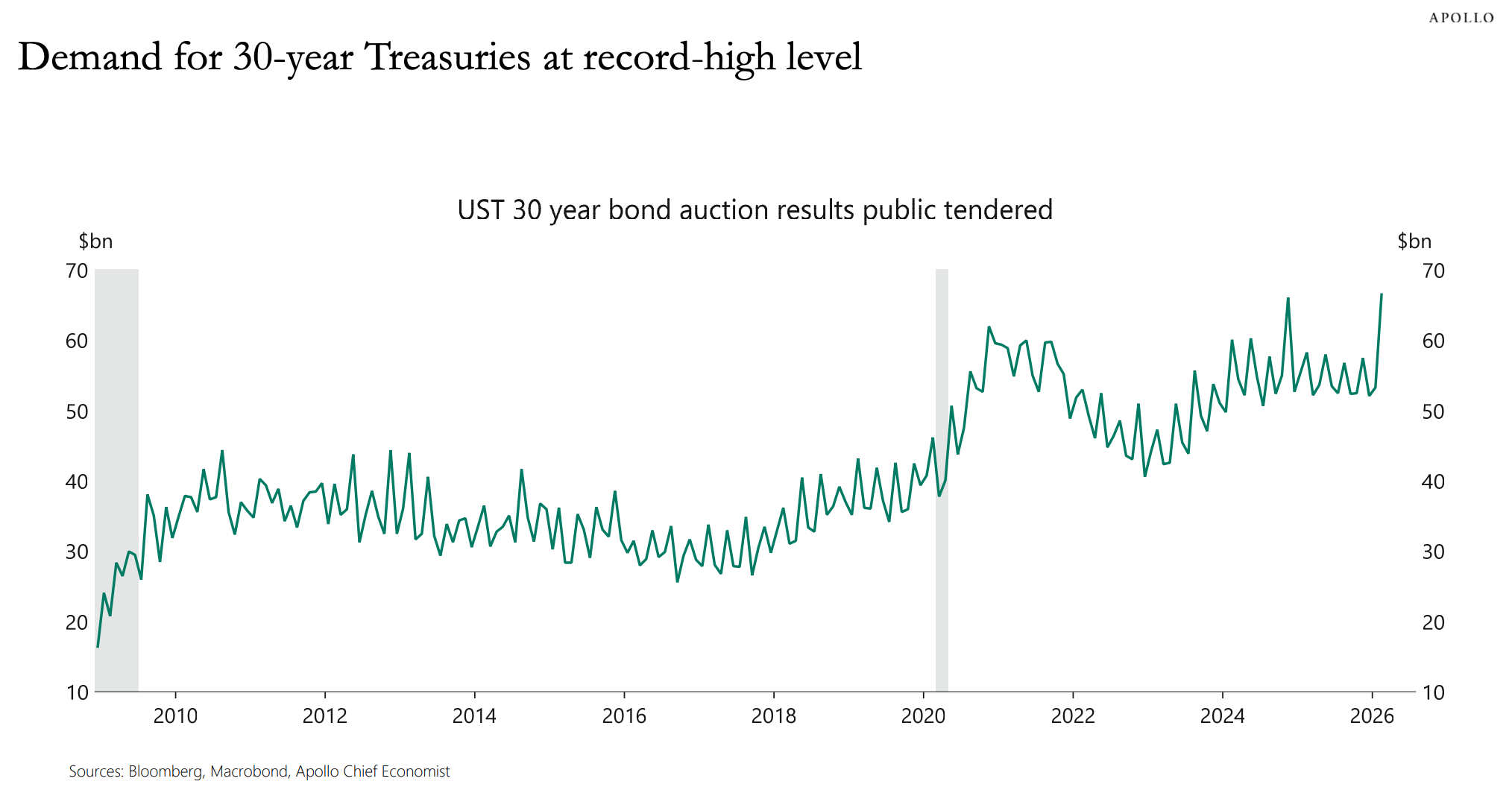

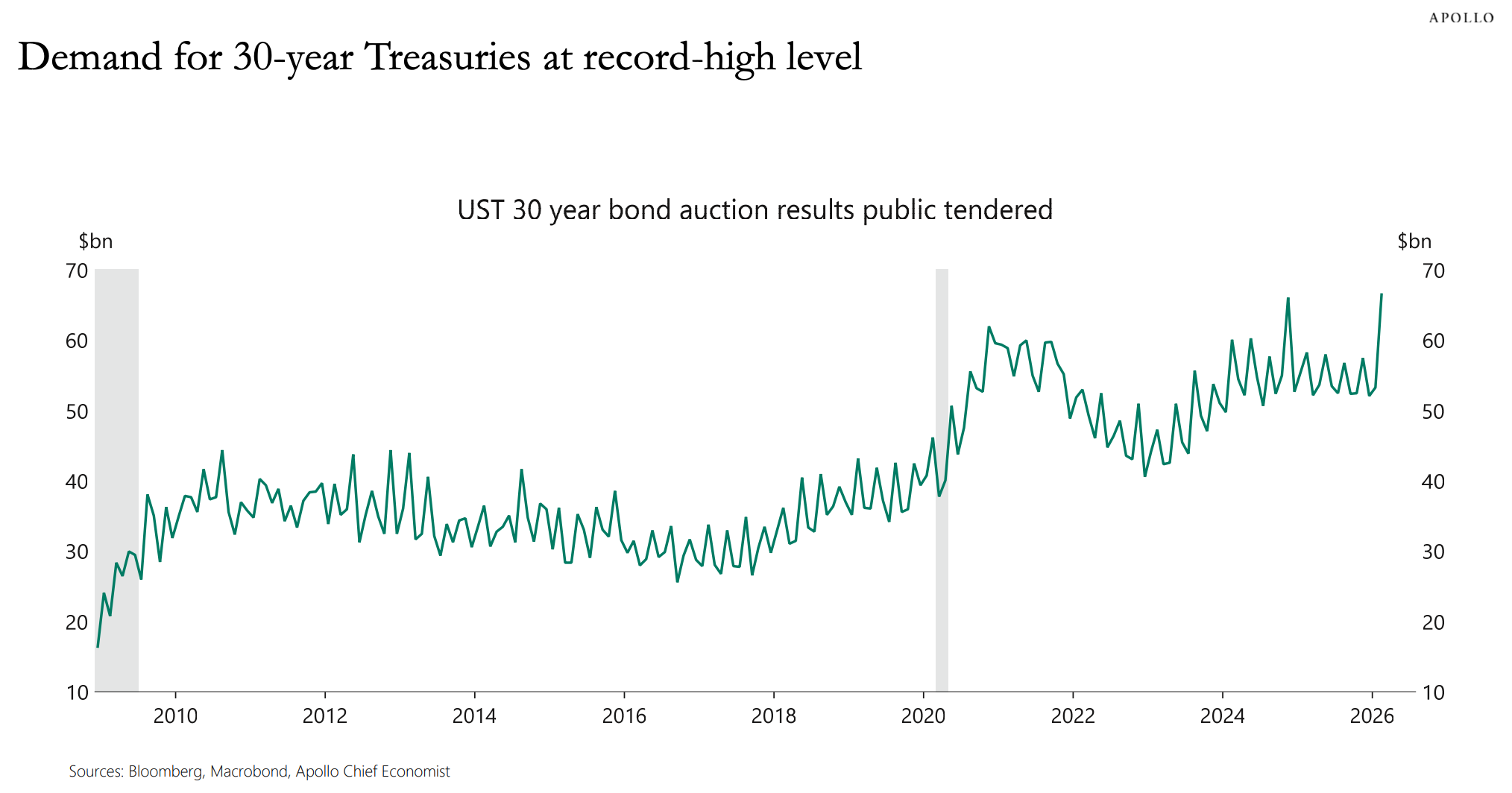

The U.S. government just saw record demand for its 30-year bonds.

That’s not a technical footnote. It’s a message about how sophisticated capital is positioning for the next decade.

When investors commit money for 30 years, they’re making a statement about inflation, growth, and risk. They’re saying, “At these yields, this is acceptable protection.”

That matters because the 30-year yield anchors almost everything else. Mortgage rates. Corporate borrowing costs. Private equity discount rates. Equity valuations. Long-term planning assumptions.

If demand at the long end remains strong, it helps prevent disorderly spikes in long-term rates. That stabilizes financial conditions. And stability in long-term rates supports asset pricing across public and private markets.

The common narrative is that large deficits must push long-term yields much higher. But markets don’t move on narratives. They move on clearing prices. If supply increases and demand rises alongside it, the system absorbs the pressure.

Strong demand also tells us something deeper about regime.

The 30-year bond embeds expectations for inflation and growth over decades. If large allocators are comfortable locking in yields for that long, it suggests inflation expectations are not spiraling higher. It suggests long-term growth expectations may be moderating. Or it suggests the yield itself now compensates adequately for those risks.

For families with meaningful capital at stake, this connects directly to portfolio construction.

Long-duration Treasuries are one of the few assets that can provide convexity in a deflationary or risk-off shock. In equity drawdowns, long bonds have historically provided positive asymmetry when growth expectations fall and yields decline.

If structural demand is returning to that part of the curve, it may be because institutions want that convexity back in their portfolios.

This isn’t about predicting rates. It’s about observing behavior.

When sophisticated capital commits for 30 years at record levels, it tells us something about how risk is being priced.

And risk pricing at the long end influences everything else.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.