You Either Have an Edge — Or You’re Someone Else's

You Either Have an Edge — Or You’re Someone Else's

In every market transaction, someone has a structural advantage—and someone else is on the other side of it, often without realizing it.

That difference usually isn’t intelligence, effort, or credentials. It’s whether the portfolio is built around a repeatable, disciplined edge, or whether it’s reacting to markets as they unfold.

Most investors believe they have an edge. Very few actually do.

What an Edge Really Is

An edge isn’t a prediction. It isn’t a hot tip, a strong opinion, or a conviction about what markets will do next.

A real edge is structural. It’s hard to replicate, grounded in economic or behavioral reality, and systematic enough to execute across full market cycles—not just the good parts.

At Shell Capital, our ASYMMETRY® framework looks at potential advantages through three simple lenses:

Positive Expectation: Does the approach have a rational, mathematical foundation that supports favorable outcomes over full market cycles—not just during strong markets?

Causal Foundation: Is it based on identifiable economic or behavioral forces, or is it just correlation dressed up as insight?

Real-World Execution: Can it actually be implemented once you account for volatility, drawdowns, costs, and the reality that investors are human?

If an approach doesn’t pass these tests, it may sound compelling—but it isn’t a durable investment discipline.

What a Durable Edge Looks Like In Business, Trading, and Investing

One useful way to think about edge comes from institutional research that studies why most strategies fail:

Useful Work: Markets reward participants who provide something of value—like liquidity during stress, risk absorption when others pull back, or discipline when emotions are running high.

Difficult Execution: If a strategy feels easy, comfortable, or emotionally satisfying in real time, it usually isn’t an edge. Edges tend to require doing things that feel uncomfortable—and sticking with them longer than most people can.

Execution Discipline: Finding a potential advantage isn’t the hard part. Capturing it consistently, across changing market regimes and under pressure, is.

That’s where most approaches break down.

Why Most Investors Struggle

Most investors don’t operate with a defined investment discipline.

They chase what’s worked recently, abandon their process mid-cycle, and make decisions based on comfort rather than expectancy. Behavioral tendencies like recency bias, loss aversion, and capitulation during volatility aren’t random—they’re systematic.

And without a disciplined framework, portfolios often end up providing liquidity to more systematic participants, especially when markets are under stress.

Why This Matters for Business Owners and Physicians

We've been advising business owners and physicians since the 1990s. If you’re a business owner or a physician, you’re usually not short on intelligence or effort—you’re short on time, attention, and tolerance for avoidable mistakes.

You’ve already taken concentrated risk to build what you have. Your wealth often isn’t the product of “average” decisions—it’s the product of a few big ones that worked. That’s also why the biggest threat usually isn’t missing the next rally.

It’s letting a meaningful portion of what you’ve earned get handed back through unmanaged drawdowns, forced decisions at the wrong time, or a portfolio that only works when markets cooperate.

Most high-income professionals don’t need more complexity. They need a portfolio that’s built around a simple reality: markets don’t send warnings before volatility expands, correlations converge, and the plan you thought you had gets tested.

That’s where disciplined risk management stops being academic and starts being personal.

The ASYMMETRY® Philosophy

At Shell Capital, everything starts with one idea: risk mitigation comes first.

Do no harm.

We don’t rely on forecasts or market calls. We manage risk systematically.

That means:

Defined Risk: Before Return Capital preservation and drawdown control come before return objectives.

Process Over Prediction: We manage portfolios across volatility regimes instead of guessing what markets will do next.

Portfolio-Level Risk Management: Risk is managed at the total portfolio level, not just position by position.

Systematic Exits: Every position has predefined exit criteria. Decisions are made before emotion enters the picture—not after.

Risk-Based Position Sizing: Capital is allocated based on risk, not conviction or narrative strength.

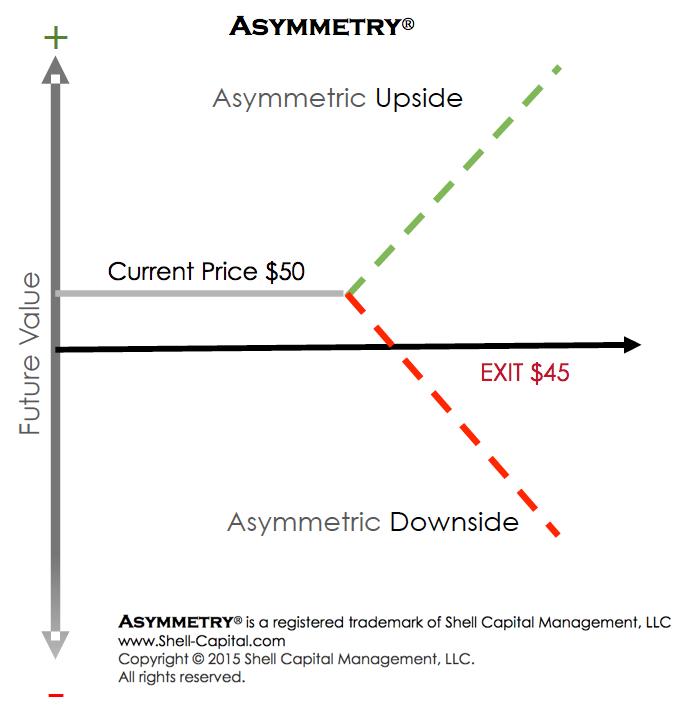

Our goal isn’t to outperform a benchmark in every environment. It’s to pursue favorable asymmetric, risk-adjusted outcomes over full market cycles while avoiding the kinds of losses that permanently impair capital.

Everyone Has an Exit

I’ve been saying this since the 1990s:

Everyone has an exit.

It can be predefined and disciplined—or it can happen when the pain becomes too much and you tap-out.

Either way, the exit comes.

Portfolios without defined risk management don’t avoid exits. They just wait until markets or emotions force the decision.

We think that’s the wrong way to do it.

Discipline Beats Hope

Markets don’t reward hope, conviction, or comfort. They reward preparation, discipline, and risk awareness.

Investors either operate with a systematic, risk-managed approach—or they’re taking more risk than they realize, especially when market conditions change.

At Shell Capital, our trademark ASYMMETRY® isn’t a slogan.

It’s a disciplined framework built around managing risk first and opportunity second.

Everything we do revolves around ASYMMETRY®; whether it's exit planning to help an owner sell a business or managing the proceeds for retirement income, it's all about the asymmetry of limiting the downside to unleash the upside.

That discipline, applied consistently over time, is what we believe makes the difference.

___________________________

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. The content is not intended to provide a complete description of Shell Capital’s investment process or strategies and should not be relied upon in making investment decisions.

Securities, charts, indicators, formulas, or examples referenced are illustrative in nature and are not intended to represent actual client holdings or recommendations. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal.

Any opinions expressed are subject to change without notice as market conditions evolve. All information is believed to be reliable but is not guaranteed and should be independently verified. Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement.

This material is not intended as an offer or solicitation for advisory services in any jurisdiction where such offer or solicitation would be unlawful.