Disability Income Planning Is Harder for Families With Meaningful Capital Than It Appears

Disability planning can be frustrating for high earners.

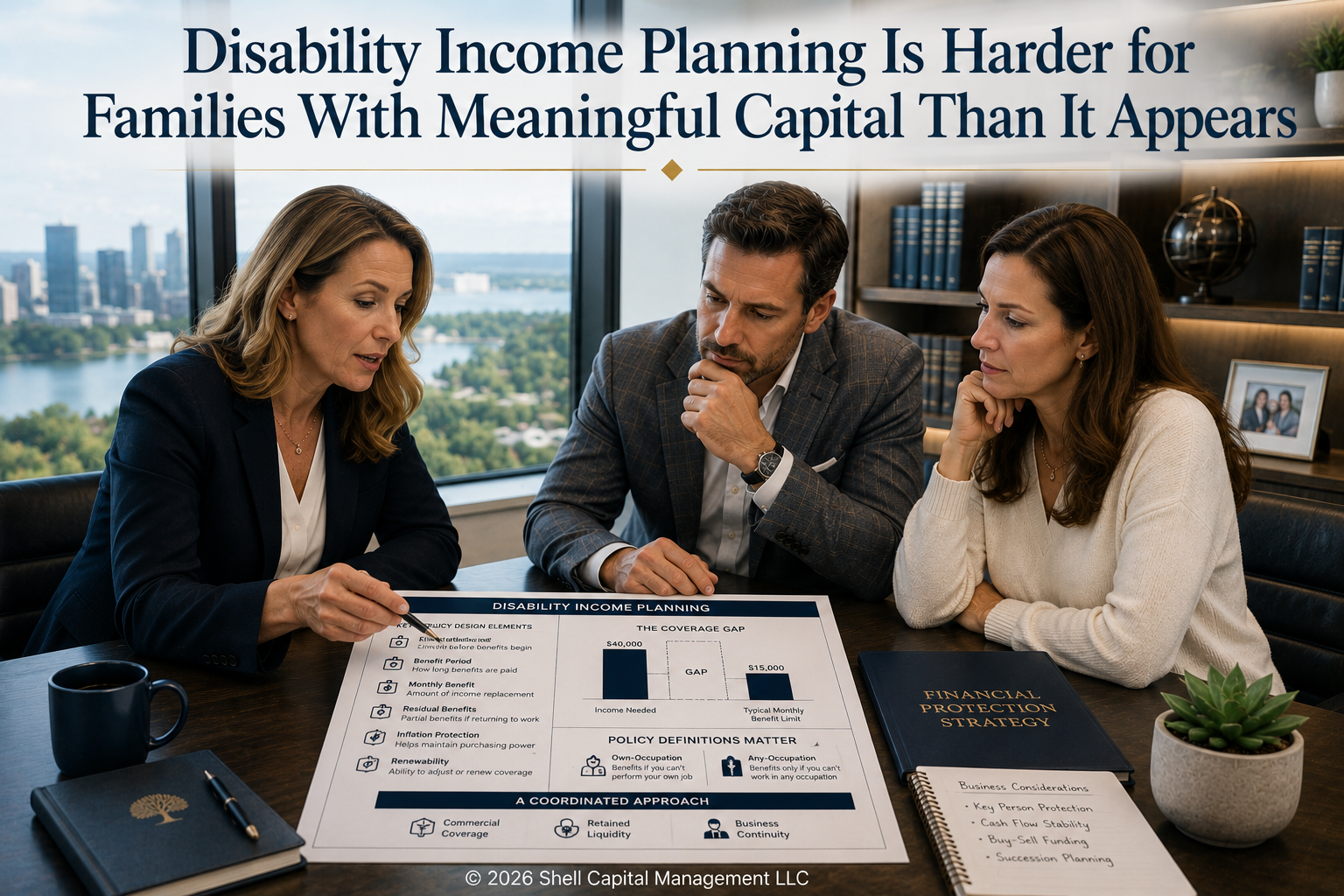

The financial risk is meaningful, but the coverage available may fall short of expectations.

That disconnect exists for several reasons. Individuals with substantial assets or investment income may already possess alternative sources of cash flow, which can reduce the insurer’s view of economic need. At the same time, carriers frequently cap monthly benefits below the amount required to fully maintain an existing lifestyle.

Definitions then become decisive.

An any-occupation standard is generally more restrictive because benefits may not be paid if the insured remains capable of working in another reasonable role. An own-occupation definition is often more valuable for specialists whose earning power depends on a highly specific skill set.

Other design variables shape the practical outcome.

The elimination period determines how long the insured waits before benefits begin. The benefit period establishes how long payments may continue. Monthly indemnity affects the amount of replacement income available. Residual benefits, inflation adjustments, and renewability provisions may materially influence how effective the coverage becomes over time.

There is also a business dimension.

Companies may use disability coverage to protect cash flow against the disability of a founder, senior executive, or key revenue producer. In some situations, disability funding may also support buy-sell obligations among owners.

For many families with meaningful capital at stake, the final structure is not purely insurance or purely self-insurance.

It is often a coordinated blend of commercial coverage, retained liquidity, and realistic expectations regarding what the policy can and cannot accomplish.

That combination is often more durable than relying on one tool alone.

Written by Christi Shell, CWS®, AAMS®, BFA™, CETF®, Managing Director and Private Wealth Strategist at Shell Capital Management, LLC.

To speak with Christi about your financial situation, request a private consultation.

Shell Capital Management, LLC is a registered investment adviser. This material is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Advisory services are only offered to clients or prospective clients where Shell Capital Management, LLC is properly registered or exempt from registration. Any views are as of the date published and may change. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.