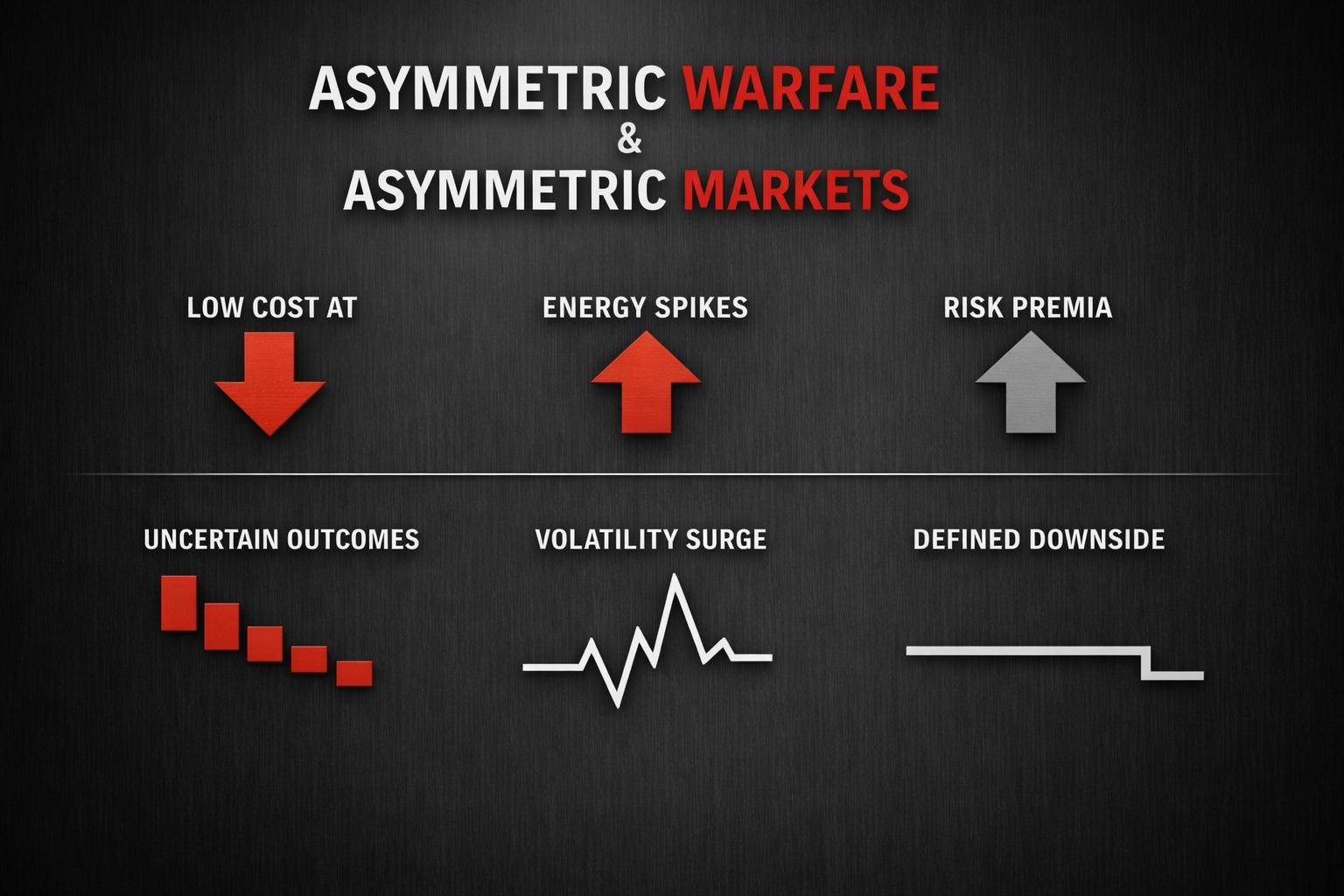

Asymmetric Warfare and Asymmetric Markets

Most investors think war risk is binary. Either it escalates and markets collapse, or it fades and markets recover.

That framing is too simple.

Modern conflicts, particularly those involving Iran, are asymmetric by design. And asymmetric conflicts rarely produce linear market outcomes. They produce pockets of convexity, volatility expansions, and selective repricing across specific return drivers.

When you manage capital with consequences, that distinction matters.

The misconception is that war equals broad equity collapse.

Historically, markets don’t trend lower simply because conflict exists. They trend based on liquidity, earnings expectations, credit conditions, and whether the conflict materially alters global cash flow systems. The S&P 500 can decline -5% to -10% on headlines and then stabilize if energy flows, shipping lanes, and credit markets remain intact.

Asymmetric warfare changes the transmission mechanism.

Iran does not attempt force-on-force dominance against the United States or Israel. It uses proxies, drones, missiles, cyber pressure, and distributed nodes to impose costs without matching conventional power. The objective isn’t battlefield victory. It’s cost asymmetry — forcing a superior adversary to spend $1 million intercepting a $20,000 drone, stretching defenses, and applying pressure at multiple points simultaneously.

That same logic shows up in markets.

When conflict is asymmetric, market impact is rarely uniform. It concentrates in specific pressure points:

Energy supply risk. Shipping lanes. Defense spending. Regional currencies. Volatility pricing.

If oil trends higher by +15% to +25% on perceived supply risk while the broad index is flat, that’s asymmetric repricing. If volatility expands from 15% to 25% while equities decline only -4%, that’s asymmetric risk transfer.

The move isn’t about headlines. It’s about where pressure concentrates.

The first principle correction is this: markets price cash flow disruption probability, not political rhetoric.

For a conflict to create systemic downside, it must impair global liquidity or durable earnings streams. That typically requires:

- Sustained energy supply disruption

- Strait of Hormuz closure risk

- Material escalation between state actors

- Credit market stress

Absent those conditions, markets often digest conflict and rotate rather than collapse.

Leadership shifts. Risk premia widen selectively. Capital rotates.

Asymmetric warfare therefore produces asymmetric market responses.

That creates two potential edges for disciplined capital allocators.

First, convexity in targeted exposures. Energy equities, defense contractors, volatility instruments, shipping, and select commodities can experience upside convexity relative to downside risk if sized intentionally and defined in advance.

Second, defined downside across the portfolio. Portfolio risk — expressed as total open risk if every position simultaneously declines to its predefined exit — must remain within tolerable consequence limits. If portfolio risk is 6.0% of capital and volatility expands, you already know your worst-case modeled drawdown under predefined exits. That clarity changes behavior.

The boundary condition is escalation.

If conflict shifts from asymmetric proxy pressure to direct state-level conventional engagement that impairs global energy transit, the regime changes. Oil trending +30% to +50% is no longer improbable. Inflation expectations shift. Rates may reprice. Equity risk premia expand.

But that scenario is a probability distribution, not a certainty.

Capital with consequences shouldn’t rely on prediction. It should rely on structure.

Business owners and families who have converted human capital into permanent financial capital operate differently. Drawdowns aren’t theoretical.

- A -20% decline requires a +25% recovery just to break even.

- A -33% decline requires +50%.

Recovery math is unforgiving.

That’s why asymmetric exposure must be intentional, not assumed.

A margin of safety alone doesn’t create asymmetry. Convexity must be structured. Downside must be predefined. Position sizing must reflect exit distance. Portfolio risk must be measured as a percentage of total equity.

Asymmetric warfare is a reminder of how modern systems absorb shocks.

Pressure distributes. Costs transfer. Risk rotates.

Markets behave the same way.

The question isn’t whether geopolitical headlines will increase. They will.

The question is whether your capital structure is built to absorb volatility while maintaining optionality when asymmetric opportunity emerges.

That’s portfolio management.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.