Engineering Bitcoin into an Asymmetric Risk/Reward Investment and Managing Cryptocurrency Risk

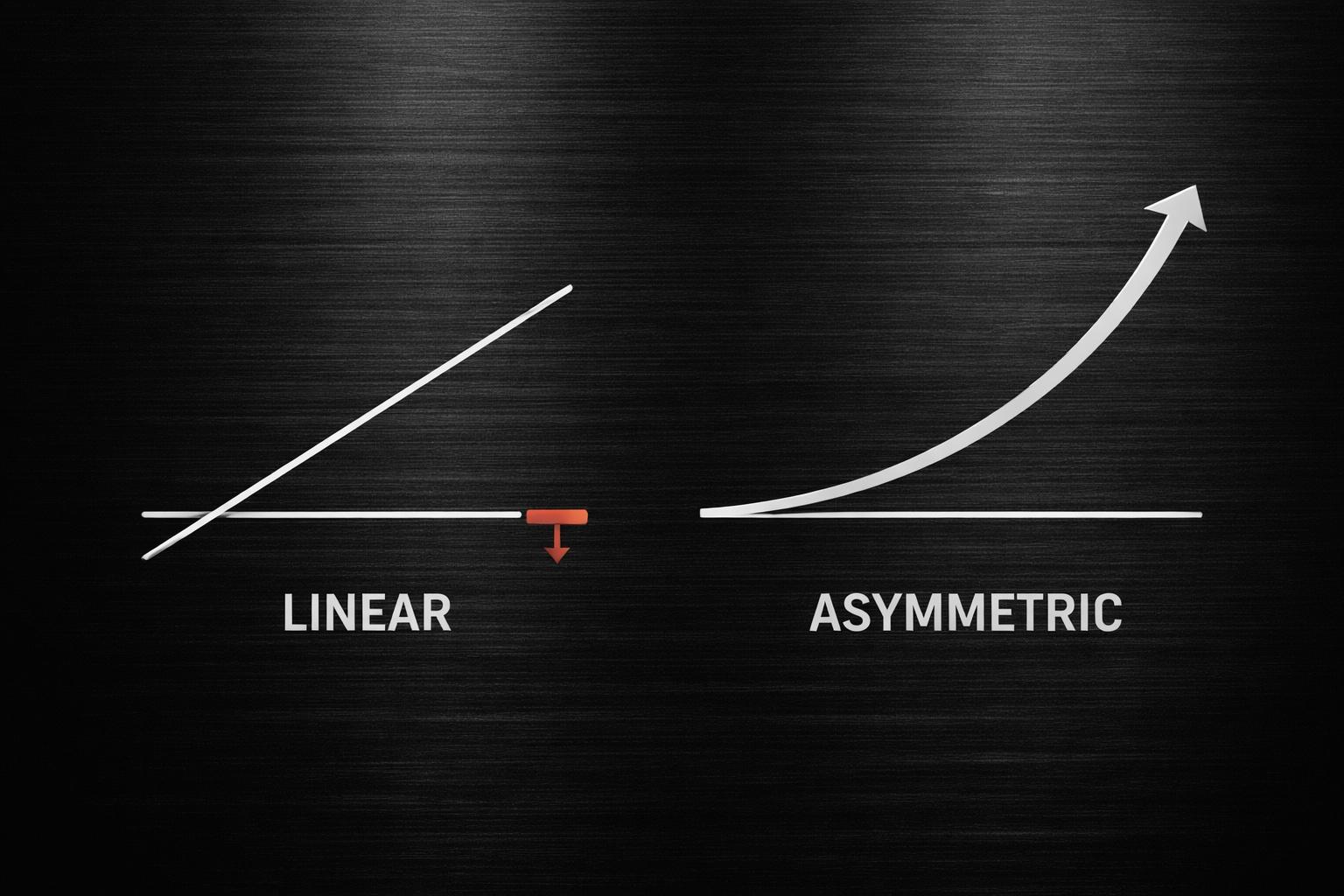

In " Why Bitcoin Itself Lacks Asymmetric Risk/Reward," we said that spot Bitcoin isn’t inherently asymmetric. It’s basically a straight-line payoff: you participate in gains and losses with no built-in loss limiter.

Bitcoin is a very risky asset. Yes, it's also very volatile, but we define risk in real, absolute terms: drawdowns. As evidenced by YCharts, Bitcoin has spent much of its trend in deep drawdowns as high as -83%.

Cryptocurrencies like Bitcoin aren't for buy-and-hold, unless you're willing to risk it all, or at least -83%, and wait (and hope) for a recovery.

An 80% drawdown requires a 400% gain to get back to breakeven.

You can probably see the asymmetry and potential for an edge if we implement drawdown controls to limit the downside, and then try to capture the upside.

Here’s an idealized example of the fix. Let's make it asymmetric.

We don’t get asymmetry from the asset. We create it by engineering two things:

- A line that defines your downside

- A line that lets you stay in the trade if the upside trends

That’s exactly what the chart is doing. And by the way, Bitcoin is currently in a -23% drawdown from its high, as you can see. The good news is, it's attempting to form a new uptrend of higher lows and higher highs. That's why I'm stalking it.

The red dots are a volatility stop-loss. Think of them as a “risk fence” that adapts to how wild the market is. When volatility expands, the fence moves farther away, so you don’t get shaken out by noise. When volatility contracts, it tightens, so you don’t give back as much.

The white line is anchored VWAP. That’s not magic. It’s just the average price paid since a specific event or anchor point, weighted by volume. In plain English: it’s where the crowd’s cost basis tends to cluster.

Now connect the dots.

If the price is above the anchored VWAP, buyers are in control, and the average participant is in profit. That’s a tailwind.

If the price is below the anchored VWAP, the average participant is underwater. That’s a headwind.

So here’s how we could turn spot Bitcoin into asymmetry:

- We only take the trade when the price is above the anchored VWAP

- We define the downside with the volatility stop (the red dots)

- We let winners run as long as the price stays above VWAP and the stop keeps ratcheting up

That structure changes the geometry.

Your maximum loss is no longer …“it can go to zero.”

Your maximum loss is the distance from entry to the volatility stop, which is defined the moment you enter.

That’s the asymmetry: defined downside, uncapped upside.

And the combination matters.

Anchored VWAP is your regime filter. It answers: Should we even have exposure right now?

The volatility stop is your risk limiter and exit rule. It answers: if we’re wrong, where do we get out?

Put together, you’re no longer relying on a belief about Bitcoin. You’re running a rule set.

One more point that makes this powerful.

The stop is trailing. That means if Bitcoin trends higher, your defined risk shrinks over time. The trade can move from “risk on” to “house money” as the stop rises. That’s how a linear instrument can behave like it has convexity over a full cycle: you cut losses fast, and you hold winners longer than feels comfortable.

This is why most people never get the asymmetry they claim.

- They buy spot without a regime filter.

- They hold through drawdowns without a predefined exit.

- They turn volatility into a lifestyle.

The asymmetric version is the opposite.

- Filter the regime with anchored VWAP.

- Define risk with the volatility stop.

- Let the upside be uncertain, but the downside be known.

That’s the real distinction.

Bitcoin itself doesn’t provide asymmetry. Structure does.

When the downside is explicitly defined and enforced, and the upside is allowed to compound without prediction, the payoff changes shape. What was once a volatile, linear exposure becomes a controlled asymmetric opportunity. Not because the asset changed, but because the risk management did.

Asymmetry is engineered, not assumed

Asymmetry isn’t found. It’s built. We engineer it, then manage it.

Bitcoin doesn’t magically deliver asymmetric risk/reward. Left unmanaged, it’s just volatile spot exposure with no predefined downside.

The asymmetry emerges only when risk is engineered first.

By filtering exposure with anchored VWAP and defining exits with a volatility-based stop, downside becomes known while upside remains uncertain. Losses are constrained. Winners are allowed to compound. Over time, that process reshapes the payoff from linear to asymmetric.

The asset didn’t change.

The structure did.

That’s the difference between owning volatility and engineering asymmetry.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.