Why Bitcoin Itself Lacks Asymmetric Risk/Reward

Does the cryptocurrency Bitcoin offer an asymmetric risk/reward payoff?

Asymmetry isn’t a narrative. It’s a payoff function.

Crypto commentary keeps calling bitcoin “asymmetric.” Usually, the pitch is some version of limited supply, massive upside, and “you can only lose what you invest.”

That’s not asymmetry. That’s exposure.

In markets, asymmetry isn’t about how big the upside could be. It’s about whether downside is explicitly bounded ex-ante relative to a meaningfully larger upside. It’s geometry. It’s structure. It’s engineered before the outcome is known.

Spot bitcoin doesn’t embed that structure.

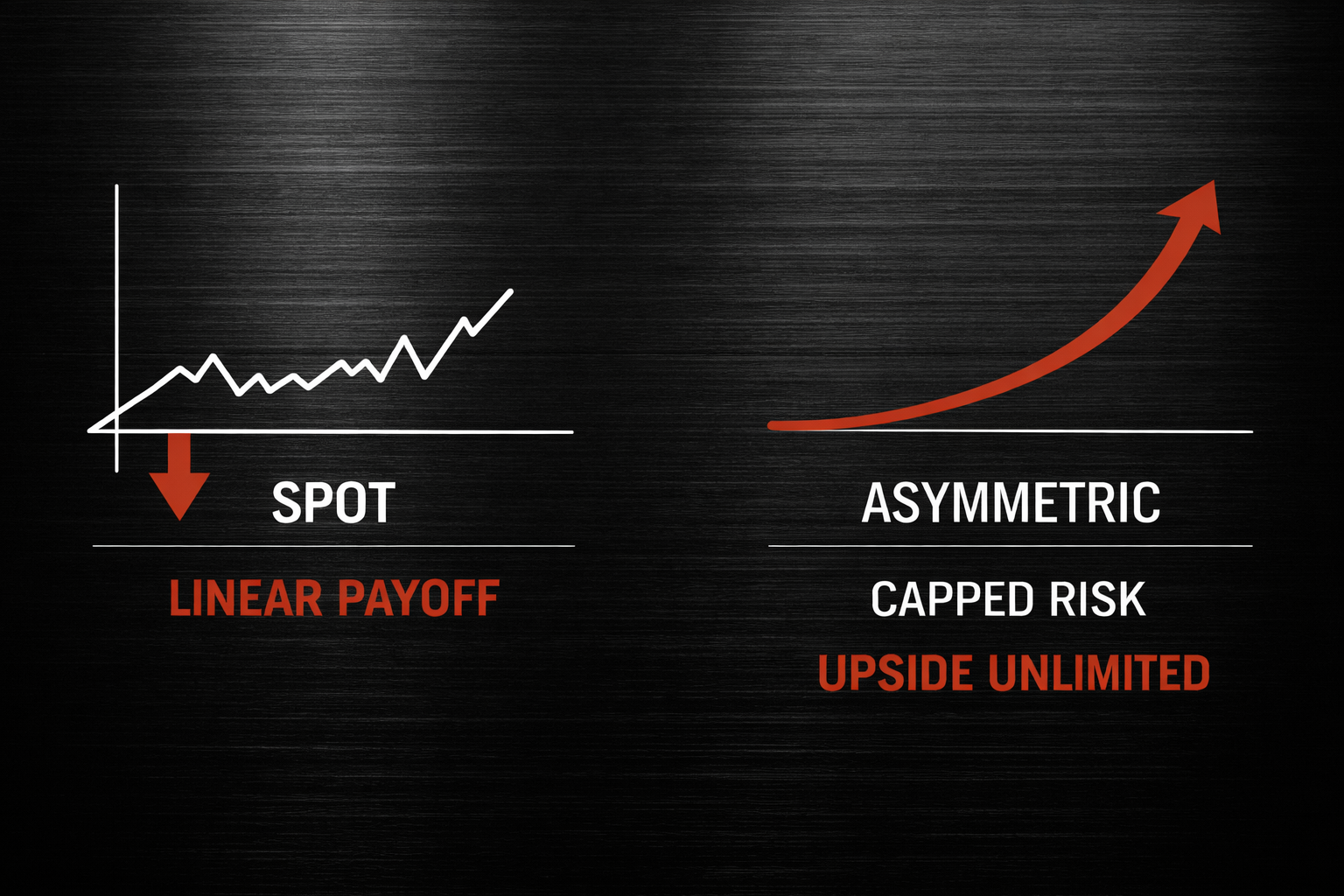

Spot exposure is essentially linear: you participate dollar-for-dollar in gains and losses, with a hard floor at zero. That “can’t go below zero” fact doesn’t create convexity. It just means the worst-case outcome is total loss. Total loss is not the same thing as defined risk.

Defined risk means you can point to the mechanism that caps losses before price moves.

A put option does this.

A structured note can do it.

A systematically enforced exit can do it (if it’s real, sized properly, and consistently executed).

Spot bitcoin by itself does not.

This is where the category error happens: people confuse skew with convexity.

Bitcoin returns can be positively skewed at times. That’s a statement about the distribution of outcomes. Convexity is a statement about payoff curvature. Convexity exists when incremental upside participation accelerates relative to incremental downside participation. Spot doesn’t do that. Spot is a straight line.

So when someone says, “Bitcoin is asymmetric because it can go up many multiples but can only go to zero,” they’re really saying the range of outcomes is wide. Wide isn’t asymmetric. Wide without loss constraints is just volatility and drawdown risk.

Asymmetry isn’t: “I can’t lose more than I put in."

Asymmetry is saying, “I’ve predefined how much I’m willing to lose, and the upside I’m targeting is not capped by that loss.”

That’s why most crypto implementations fail the asymmetry test. There’s usually no position sizing tied to a predefined exit. No volatility targeting. No loss limiter. Just a belief that the upside will outrun the pain.

Ironically, crypto can be used asymmetrically, but the asymmetry comes from the process, not the asset.

If you size it so a stop-out is small, and you actually execute it, you’ve bounded loss.

If you add convex structures (like long optionality), you’ve changed the payoff function.

If you run a risk-managed trend system that cuts losers and keeps winners, you’ve engineered a form of convexity over time.

In those cases, the asymmetry is created by risk discipline and payoff design.

Assets don’t “offer asymmetry” by existing.

Asymmetry is what you build when you define and limit the downside so you can let the upside be uncertain.

If you can’t show the line item that caps your loss, you don’t have asymmetric risk/reward.

You have a story about riding a volatility regime.

How do we engineer crypto like Bitcoin (or any other asset) to have an asymmetric risk/reward payoff?

I answer in Part 2: Engineering Bitcoin into an Asymmetric Risk/Reward Investment and Managing Cryptocurrency Risk

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.