Leverage Doesn’t Create Upside — It Amplifies Downside

In Fighting the Last Battle, I pointed out that March 9 marked the anniversary of the 2009 market low, the end of the financial crisis bear market. What followed was one of the longest equity bull markets in history.

But every cycle leaves psychological scars.

After 2008, investors became conditioned to fight the last war: excessive caution, persistent skepticism, and an underweight posture toward equities. That mindset dominated the early years of the recovery.

Over time, the opposite dynamic emerged.

Confidence replaced caution. Risk controls loosened. Leverage quietly crept back into portfolios.

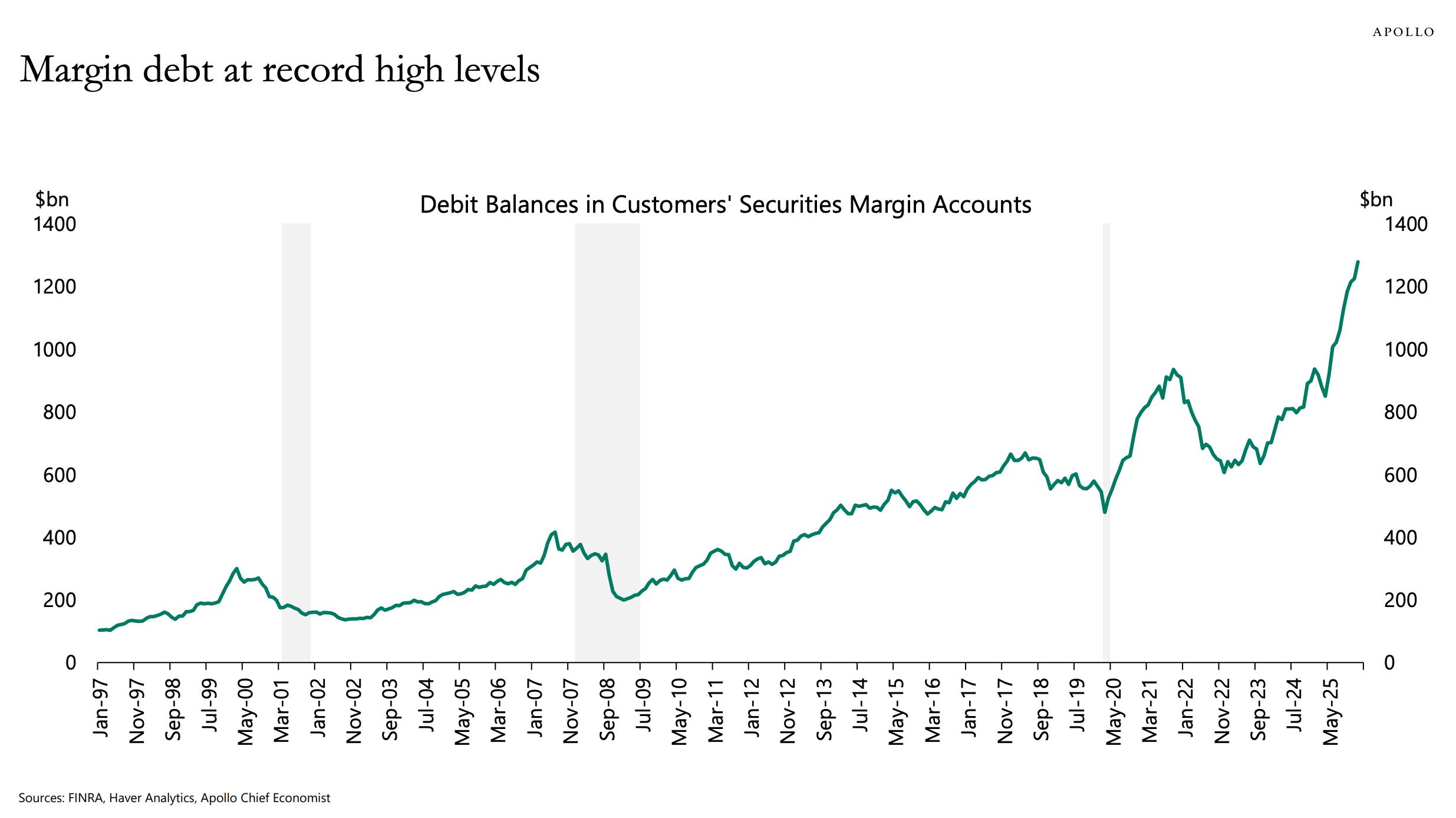

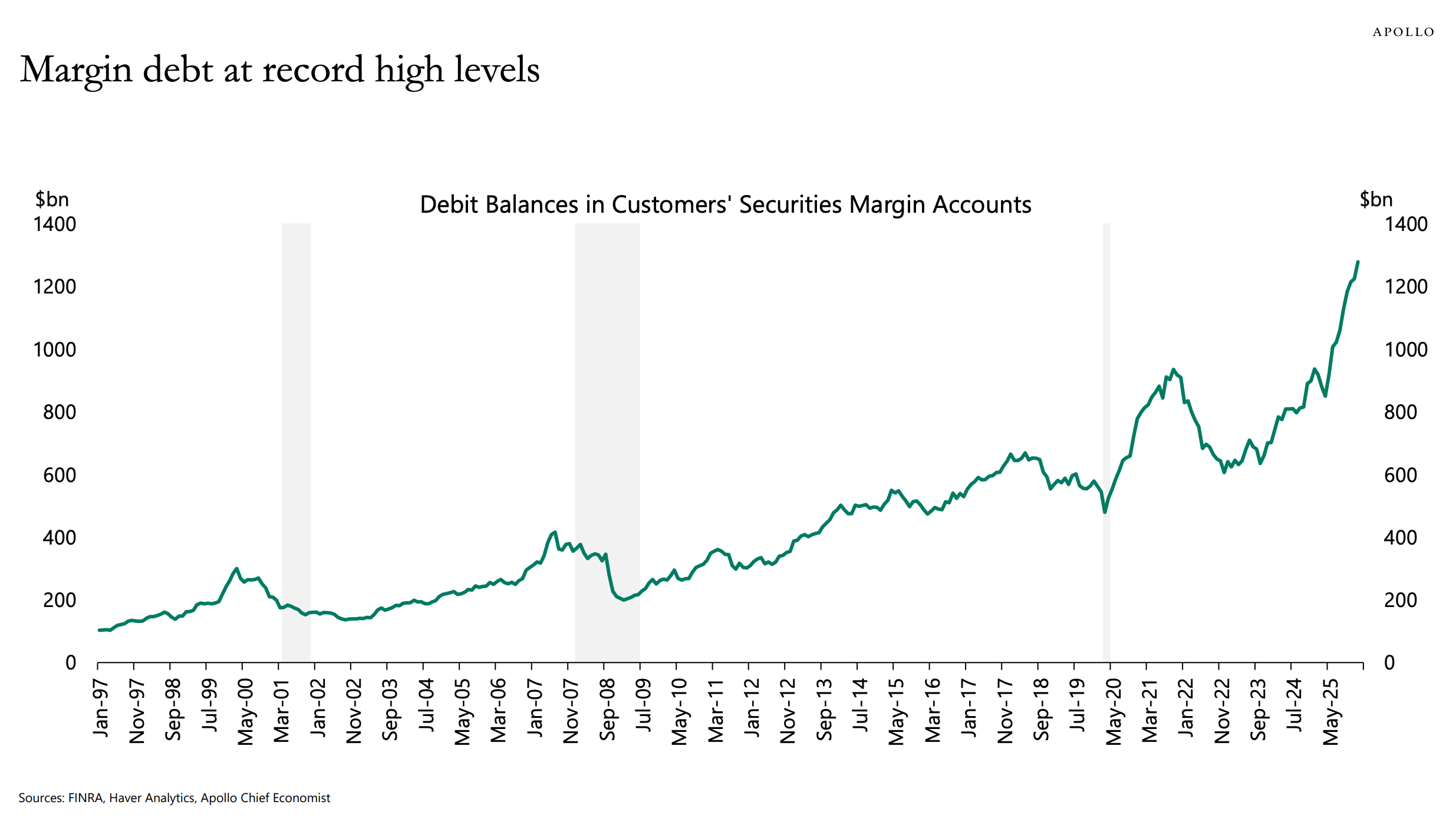

Now margin debt has reached record levels.

This matters because leverage changes how markets decline.

When investors buy stocks on margin, they are not simply buying assets. They are introducing a second constraint into the system: collateral requirements. If prices fall far enough, positions are no longer optional. They must be reduced.

Selling becomes mechanical.

The chart illustrates this dynamic.

Debit balances in margin accounts have risen steadily over the past decade, accelerating into recent highs. That growth reflects a structural increase in borrowed capital supporting equity exposure.

As long as markets trend upward, leverage appears benign.

But leverage introduces convex downside risk into the system.

When prices decline, equity in margin accounts shrinks. Brokers issue margin calls. Investors must either add capital or liquidate positions. If prices keep falling, more accounts breach collateral thresholds. Additional forced selling occurs.

This creates a feedback loop:

Price declines → margin calls → forced selling → further price declines.

The important point isn’t that leverage exists. It’s that leverage concentrates risk at the same time across many participants.

When positioning becomes crowded and financed with borrowed capital, liquidity becomes fragile. Selling pressure can propagate faster than most investors expect.

In practice, many market corrections are not driven by new information. They’re driven by balance sheet constraints.

That’s why leverage often turns ordinary pullbacks into sharper dislocations.

For investors responsible for meaningful capital, the lesson is structural rather than predictive.

The objective isn’t forecasting the next correction. It’s recognizing how leverage changes the shape of market risk.

Portfolios that rely on borrowed capital increase their sensitivity to volatility. Portfolios that define downside risk in advance retain optionality when markets become disorderly.

That distinction becomes critical when liquidity disappears.

Margin debt doesn’t cause market declines. But it often determines how far and how fast those declines travel.

Understanding that asymmetry is part of managing capital with discipline.

Mike Shell is the founder and chief investment officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.