The Art of Asymmetric Investing Isn’t Balance — It’s Survival

The Art of Asymmetric Investing: When Imbalance Beats Balance

Most investors think the goal is balance. Balanced portfolios. Balanced risk. Balanced returns.

It sounds prudent. It feels responsible. And it’s often exactly how investors end up with the wrong kind of risk.

Because markets don’t reward symmetry. They punish it.

What business owner wants to balance their profit and loss?

What investor wants to balance their risk and reward?

We want the reward of profit and less risk and loss.

That's asymmetry, not symmetry. Imbalances, not balances.

That’s the paradox.

Smooth returns often hide negative skew — many small gains punctuated by occasional, devastating losses. It’s the kind of profile that feels safe, works for a while, and quietly compounds fragility.

Asymmetry works the opposite way.

It’s uneven by design. It accepts frequent small losses, boredom, and frustration in exchange for the one thing that matters: avoiding ruin while remaining exposed to outsized upside.

This is where most investors get it wrong.

Compounding is brutally asymmetric.

Large losses hurt far more than equivalent gains help. A 50% loss requires a 100% gain just to get back to even. That’s not an opinion — it’s arithmetic.

So the first job of any serious investment process isn’t maximizing returns. It’s defining and controlling downside.

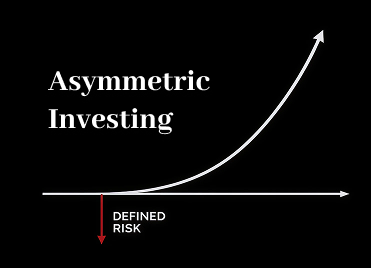

That’s the geometry of asymmetry.

Defined risk below. Open-ended upside above.

Not because we’re predicting upside — but because we’re refusing to cap it.

This is why truly asymmetric strategies often look “wrong” for long stretches.

Trend-following looks broken until it isn’t. Options with defined risk bleed until volatility arrives. Convex payoffs disappoint until the environment changes.

And when it changes, they matter — fast.

The behavioral challenge is that positive asymmetry doesn’t reward patience evenly. It pays in bursts. That makes it hard to stick with, easy to abandon, and rare to execute well.

Most investors quit right before the payoff — not because the strategy stopped working, but because it didn’t feel like it was.

That’s not a strategy problem. It’s a discipline problem.

ASYMMETRY® isn’t about chasing alternatives, complexity, or exotic investments. It’s about structuring exposure so outcomes matter more than forecasts.

We don’t need to know what will happen. We need to know what happens if we’re wrong.

Balance tries to smooth outcomes. Asymmetry tries to survive them.

And over full cycles, survival with optionality beats elegance every time.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions. The observations shared in ASYMMETRY® Observations are for general informational purposes only and do not constitute investment advice or a recommendation to buy or sell any security. The content is not intended to provide a complete description of Shell Capital’s investment process or strategies and should not be relied upon in making investment decisions. Securities, charts, indicators, formulas, or examples referenced are illustrative in nature and are not intended to represent actual client holdings or recommendations. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal. Any opinions expressed are subject to change without notice as market conditions evolve. All information is believed to be reliable but is not guaranteed and should be independently verified. Shell Capital Management, LLC, provides investment advisory services only to clients pursuant to a written investment management agreement. This material is not intended as an offer or solicitation for advisory services in any jurisdiction where such offer or solicitation would be unlawful.