When Arbitrage Opts Out: More on What Happened to the Silver ETF SLV

Following up on When ETF Arbitrage Fails: What SLV's Record Discount Reveals About Market Structure:

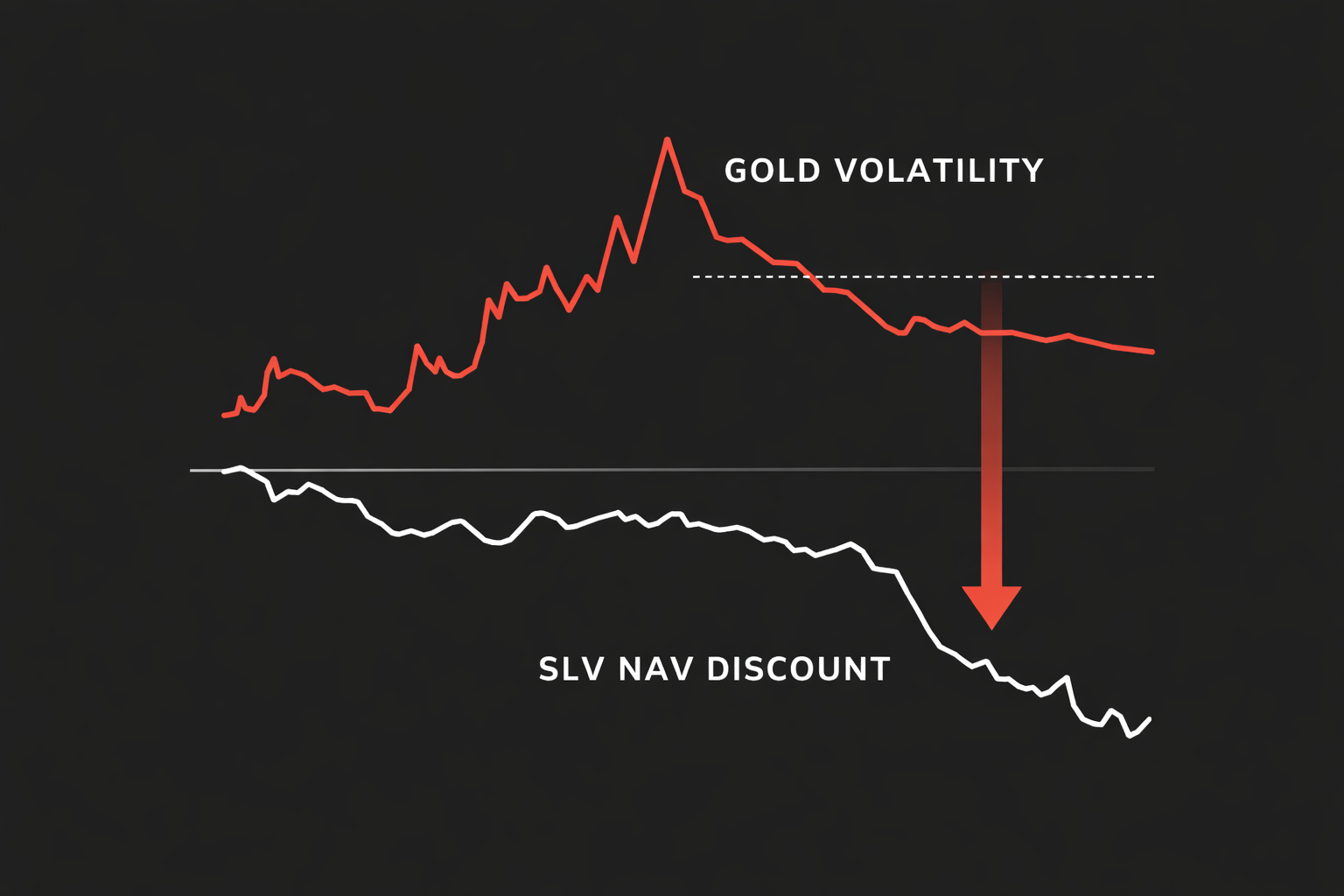

When SLV blew out to a record discount, many rushed to frame it as a temporary dislocation—a “technical” divergence between price and NAV that would close quickly. But post-mortem research from JPMorgan and Goldman Sachs shows something else entirely: a breakdown in the very mechanisms that are supposed to keep these structures functional. Arbitrage didn’t fail. It stepped away.

JPMorgan’s Delta One desk reports a significant imbalance in positioning going into the selloff. Retail demand for long metals exposure via ETFs and short-dated calls outpaced what market makers could delta-hedge. Meanwhile, GS confirms what the price action hinted at: short-dated gold volatility exploded to levels not seen since the pandemic. GLD accounted for 8% of total U.S. ETF notional volume—an extraordinary stat for a commodity ETF. There wasn’t a macro catalyst. There was too much positioning, too much leverage, and not enough liquidity to absorb the unwind.

Silver, in particular, was vulnerable. JPM points out the absence of a structural buyer. Gold has central banks accumulating on weakness. Even Tether is now among the top holders. Silver has none of that. When liquidity vanished, there was no natural bid. SLV’s discount wasn’t a market inefficiency—it was a warning. Arbitrage requires functioning pipes and willing counterparties. When both disappear at once, the structure isn’t just impaired. It’s inverted.

Goldman’s cross-asset team highlights another layer: precious metals decoupled from their usual macro anchors. The dollar fell. Real yields were stable. But metals still collapsed. Price action wasn’t a reflection of fundamentals. It was flow-driven, mechanically amplified, and structurally unarbitrageable. These aren’t accidents. They’re signals of what happens when too many players try to exit through the same ETF door at once.

SLV didn’t break. It revealed the limits of market structure under stress. There’s no edge in knowing that. The edge is in recognizing when price no longer reflects value because the plumbing can’t support it. That’s not inefficiency. That’s asymmetry.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.