When ETF Arbitrage Fails: What SLV's Record Discount Reveals About Market Structure

When Arbitrage Fails, Velocity Moves from the Metal to the Plumbing

In Asymmetry vs. Velocity in Gold and Silver, I said the distinction wasn’t about which metal was “better.” It was about how asymmetry actually shows up.

Gold trends like a regime asset. Its asymmetry is slow, structural, and policy-driven. It absorbs stress over time.

Silver doesn’t.

Silver expresses asymmetry through velocity and constraint. Its upside is episodic, liquidity-driven, and reflexive. When tightness builds, it can move violently. And when those constraints loosen, the unwind is just as fast — often faster.

Last week didn’t contradict that observation. It completed it.

What changed wasn’t silver. What changed was where the stress showed up.

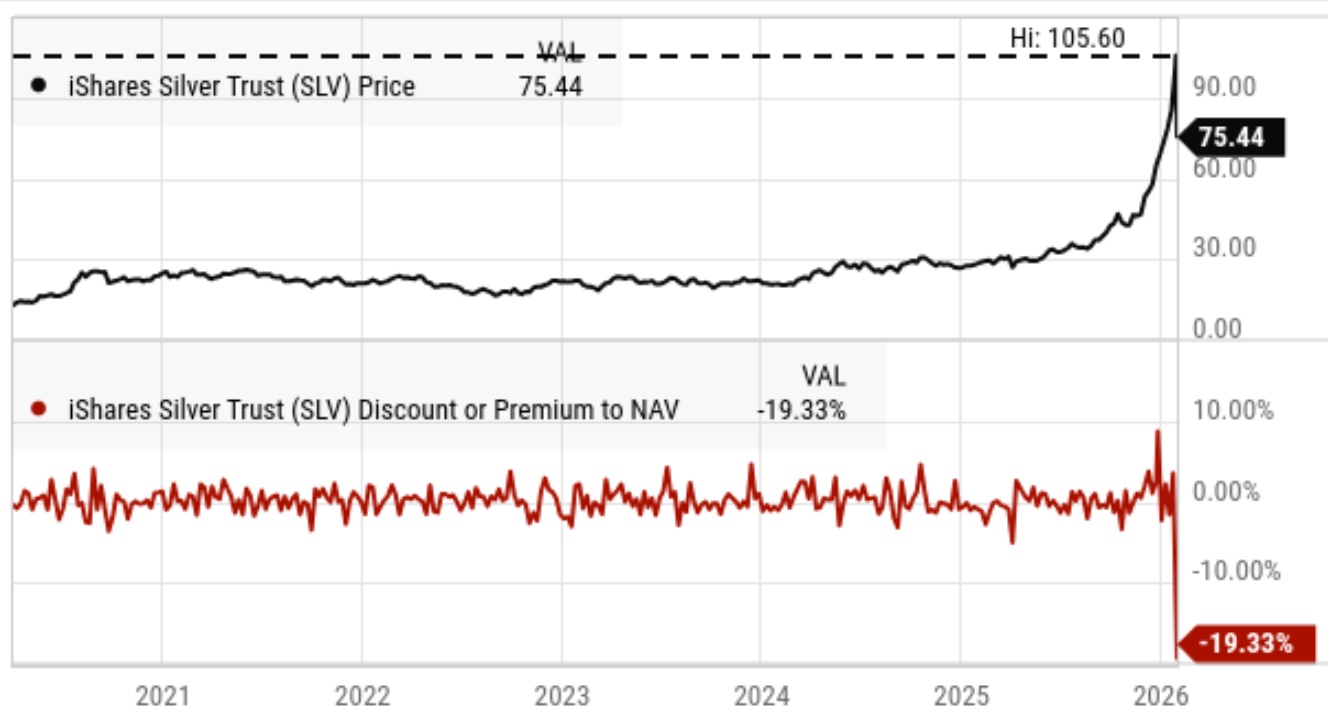

SLV appeared to close at nearly a 19% discount to its published net asset value — the most extreme discount print data services have recorded since the height of the Global Financial Crisis in October 2008, when market structure was under acute stress and balance-sheet capacity disappeared across the system.

That number matters. But it also requires a mechanical qualifier.

SLV’s official NAV is calculated using the daily London silver benchmark, which is fixed earlier in the day and then published after the U.S. market close. On a session when silver prices collapse late in U.S. trading, the reported NAV can be temporarily stale relative to the 4:00 p.m. market. In those conditions, the published discount can appear far larger than the true same-time economic gap.

Adjusted for timing, the actual dislocation was likely smaller than 19%.

But that adjustment doesn’t change the signal. It clarifies it.

This chart from YCharts shows SLV’s reported premium/discount to its published NAV over time. The abrupt ~-19% print reflects a temporary breakdown in arbitrage enforcement during extreme velocity — not a valuation error.

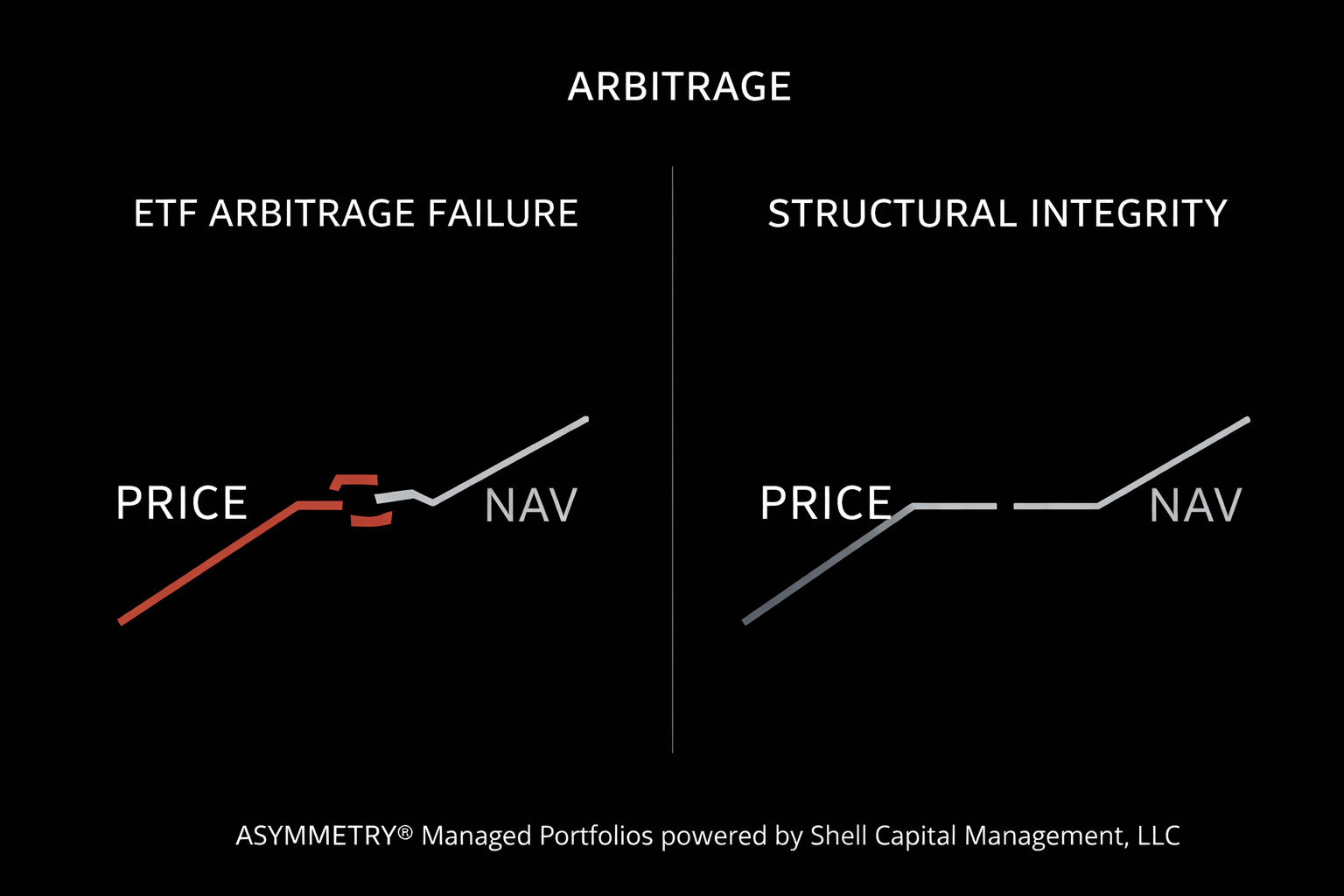

That matters, because extreme ETF discounts don’t come from disagreement. They come from failed enforcement.

The Misconception

The common assumption is that a large discount to NAV means price is wrong.

It doesn’t.

It means the mechanism designed to force convergence has stepped aside.

Markets don’t break because prices move fast. They break when the systems that enforce alignment stop functioning.

What Actually Failed

SLV is designed to track physical silver through a creation and redemption mechanism operated by authorized participants — large banks and professional market makers.

Under normal conditions, this mechanism is ruthless.

If price deviates from value, arbitrage capital steps in. Premiums collapse. Discounts disappear. Opinion doesn’t matter.

I’ve been trading ETFs since they first began trading and was an early adopter of tactical ETF strategies precisely because of this structure. The transparency, liquidity, and built-in enforcement made ETFs one of the most elegant market innovations of the modern era.

But that mechanism is not unconditional.

When volatility spikes, leverage unwinds, and liquidity providers face balance-sheet, funding, and operational constraints, arbitrage stops being opportunity and starts being risk.

Capital doesn’t rush in to fix the gap. It steps back to preserve itself.

That’s what last week exposed.

The silver market didn’t fail. The arbitrage mechanism temporarily withdrew.

Why Velocity Matters More Than Valuation

Silver is a constraint-driven market. Its asymmetry is created by tightness, leverage, and flow — not by slow policy shifts or reserve accumulation.

When silver moves slowly, ETF plumbing works quietly in the background.

When silver moves violently, the risk migrates.

Not into valuation. Into structure.

At that point, investors are no longer primarily exposed to silver’s convexity. They’re exposed to the willingness and ability of liquidity providers to warehouse risk, source metal, and process redemptions under stress.

That’s a very different exposure than most investors think they own.

What a Record Discount Is Actually Signaling

A large, persistent ETF discount is not a price signal. It’s a diagnostic.

It tells you that arbitrage capital is constrained or unwilling. That balance sheets are being protected, not deployed. That liquidity is being rationed, not provided.

In other words, the enforcing mechanism that normally keeps price and value aligned has stepped aside — not because it’s broken, but because carrying the trade has become asymmetric in the wrong direction.

This is velocity expressing itself through plumbing.

Connecting the Dots

In Asymmetry vs. Velocity in Gold and Silver, the core insight was that gold absorbs stress through time, while silver expresses stress through speed.

This observation shows what happens next.

When silver’s velocity accelerates far enough, the asymmetry doesn’t stay confined to the metal. It propagates outward — into spreads, liquidity, and the ETF wrapper itself.

Gold’s asymmetry trends like a regime. Silver’s asymmetry trends like a constraint.

And when constraints bind, even the plumbing bends.

The Asymmetry That Actually Matters

The mistake investors make is focusing on whether price is “right.”

The professional question is whether convergence is still being enforced.

When arbitrage functions, volatility is noise. When arbitrage steps aside, volatility becomes structure.

That’s the difference between a tradable drawdown and a system-level event.

Bottom Line

Extreme ETF discounts don’t tell you where value is. They tell you where risk can no longer be carried.

They reveal where leverage was hidden, where liquidity was assumed, and where asymmetry suddenly flipped from opportunity to vulnerability.

And in markets driven by velocity rather than regime, knowing when the plumbing matters more than the metal is the edge.

Monday, February 2, 2026: We've published a follow-up with new information: When Arbitrage Opts Out: More on What Happened to the Silver ETF SLV.

Mike Shell is the Founder and Chief Investment Officer of Shell Capital Management, LLC, a registered investment adviser. He serves as portfolio manager of ASYMMETRY® Managed Portfolios, a separately managed account program with trade execution and custody provided by Goldman Sachs Custody Solutions.

ASYMMETRY® Observations are provided for general informational and educational purposes only. They do not constitute investment advice, a recommendation, or an offer to buy or sell any security or investment strategy. The content is not intended to be a complete description of Shell Capital’s investment process and should not be relied upon as the sole basis for any investment decision.

Any securities, charts, indicators, formulas, or examples referenced are illustrative and are not intended to represent actual client portfolios, recommendations, or trading activity. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal.

Opinions expressed reflect the judgment of the author at the time of publication and are subject to change without notice as market conditions evolve. Information is believed to be reliable but is not guaranteed, and readers are encouraged to independently verify any information before making investment decisions.

Shell Capital Management, LLC provides investment advisory services only to clients pursuant to a written investment management agreement and only in jurisdictions where the firm is properly registered or exempt from registration.