Restricted Stock and RSUs: When Vesting Drives Taxes and Cash Flow

Not all equity compensation is about optionality.

Restricted stock and restricted stock units (RSUs) operate on a different axis than stock options. Instead of a right to purchase, they represent a grant—or a promise—of shares, with value tied to vesting conditions.

The defining feature is timing.

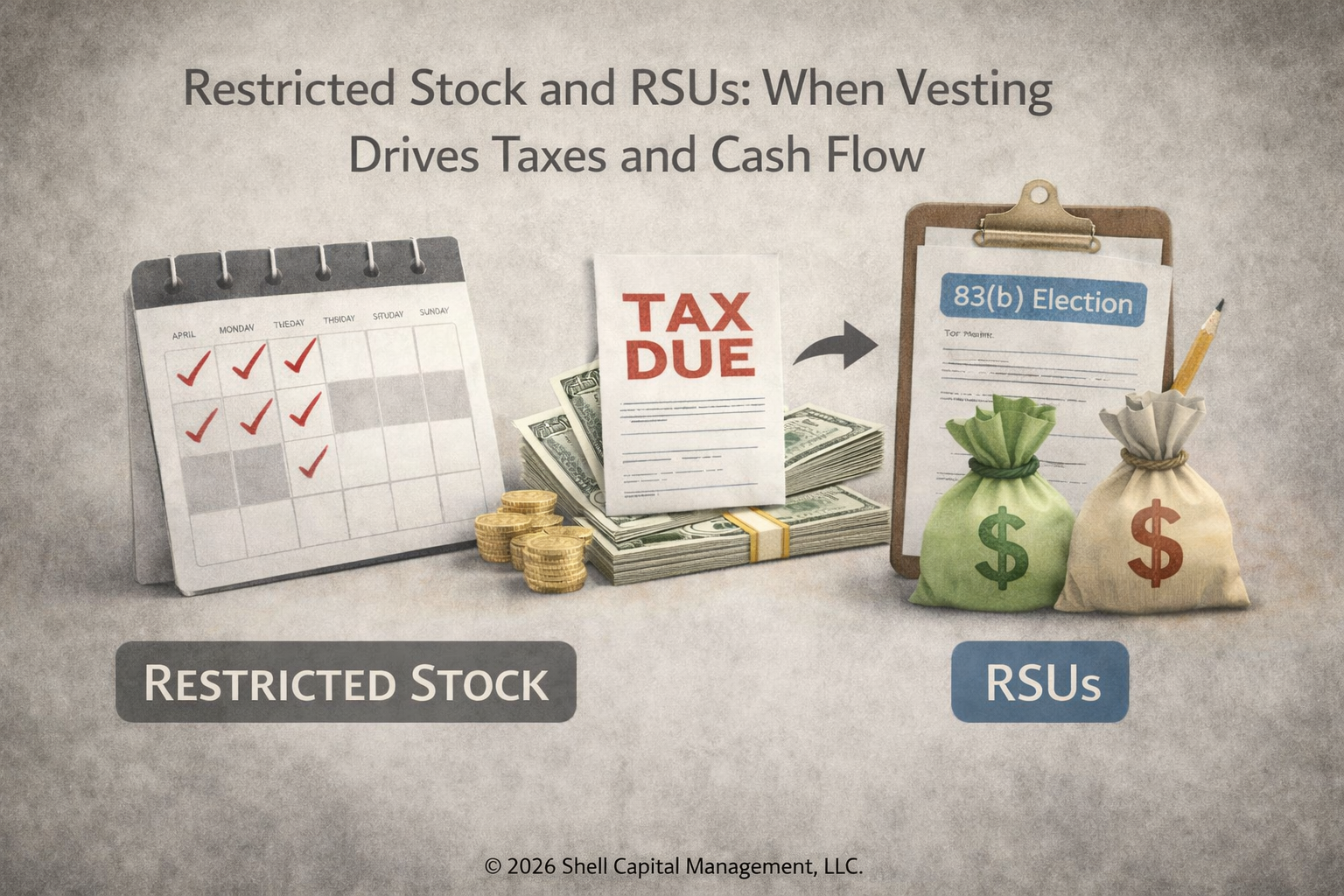

For restricted stock, taxation typically occurs when vesting restrictions lapse. At that point, the fair market value of the shares is treated as ordinary income and is generally subject to payroll taxes.

Unlike options, restricted stock does not require an exercise decision or out-of-pocket cost. The trade-off is that taxation is usually unavoidable once vesting occurs.

RSUs follow a similar economic pattern with a different structure. They represent an unfunded promise to deliver shares in the future, and taxation occurs when shares are delivered based on their value at that time.

In both cases, vesting schedules define the liquidity timeline and the tax calendar.

A central concept is “substantial risk of forfeiture.” Until vesting conditions are satisfied, the executive does not have full control of the asset, and transferability is typically restricted.

One of the few available planning levers is the Section 83(b) election.

An 83(b) election allows taxation at the time of grant rather than at vesting. This can shift the tax base to a lower initial value and allow future appreciation to be taxed at capital gains rates if holding requirements are met.

However, the election introduces defined downside.

If the stock declines or is forfeited, taxes paid at grant are not recoverable. If value does not increase meaningfully, the election can accelerate taxation without a corresponding economic benefit.

From a planning standpoint, restricted equity is schedule-driven. The key is aligning vesting-triggered tax events with liquidity structure so that taxes can be met without forced or poorly timed asset sales.

Written by Christi Shell, CWS®, AAMS®, BFA™, CETF®, Managing Director and Private Wealth Strategist at Shell Capital Management, LLC.

To speak with Christi about your financial situation, request a private consultation.

Shell Capital Management, LLC is a registered investment adviser. This material is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Advisory services are only offered to clients or prospective clients where Shell Capital Management, LLC is properly registered or exempt from registration. Any views are as of the date published and may change. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.