Direct Payments for Tuition and Medical Expenses: A Distinct Category of Family Support

Within the federal gift tax framework, certain payments are treated differently when made directly for tuition or medical expenses.

These transfers may fall outside the definition of taxable gifts when specific conditions are met, creating a unique category of financial support.

A common misunderstanding is that all support provided for education or healthcare qualifies automatically.

In practice, the structure and method of payment are critical.

Planning begins with identifying the nature of the expense.

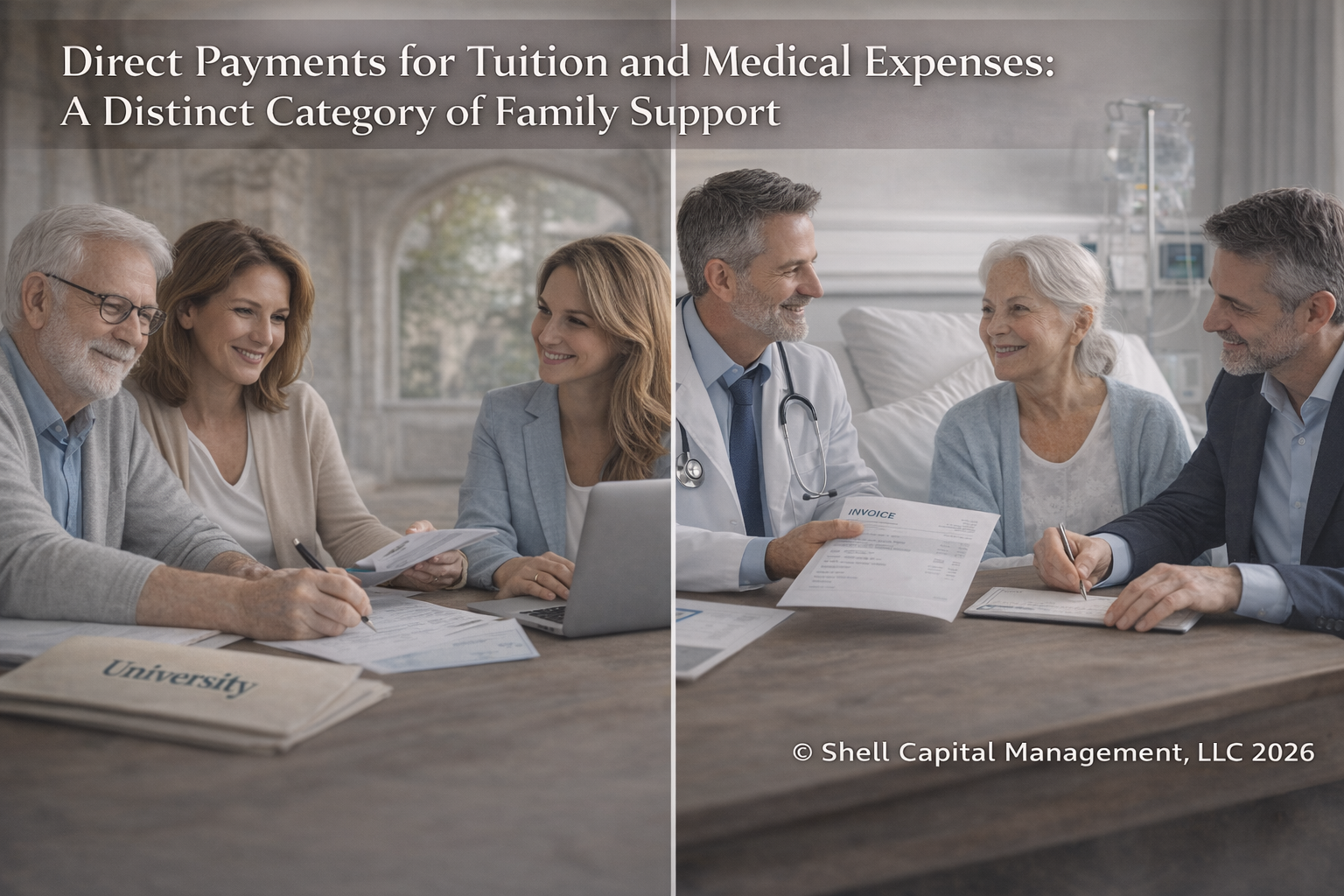

Tuition payments must generally be made directly to the educational institution. Medical expenses must typically be paid directly to the provider to qualify for exclusion from gift treatment.

Constraints arise from how payments are executed.

Reimbursements to family members may not qualify in the same way as direct payments. Timing and documentation also influence how these transfers are treated.

These distinctions introduce risk considerations.

Improperly structured payments may be treated as taxable gifts. Informal reimbursements can create unintended reporting obligations and reduce the efficiency of the transfer.

Implementation requires attention to process.

Payments should be made directly to the appropriate institution or provider, with clear documentation supporting the nature of the expense. Coordination with broader gifting strategies ensures that these transfers complement, rather than replace, other planning efforts.

Monitoring remains important.

Education paths, healthcare needs, and regulatory interpretations may evolve over time. Periodic review helps ensure continued alignment with planning objectives.

Understanding this distinction allows families to support education and healthcare needs in a way that preserves flexibility within the broader gift tax framework.

Written by Christi Shell, CWS®, AAMS®, BFA™, CETF®, Managing Director and Private Wealth Strategist at Shell Capital Management, LLC.

To speak with Christi about your financial situation, request a private consultation.

Shell Capital Management, LLC is a registered investment adviser. This material is for informational and educational purposes only and does not constitute investment, legal, or tax advice. Advisory services are only offered to clients or prospective clients where Shell Capital Management, LLC is properly registered or exempt from registration. Any views are as of the date published and may change. Investing involves risk, including the possible loss of principal. Past performance is not indicative of future results.