The First Loss Is Different After a Liquidity Event

A 20% drawdown in your investment portfolio is always uncomfortable.

But after a liquidity event, it’s something else entirely.

Before the event, losses are measured against future earning capacity. Capital can be rebuilt. Time and income act as shock absorbers. The system is resilient because it’s replenishable.

After the event, that changes.

The capital you have is the capital you have.

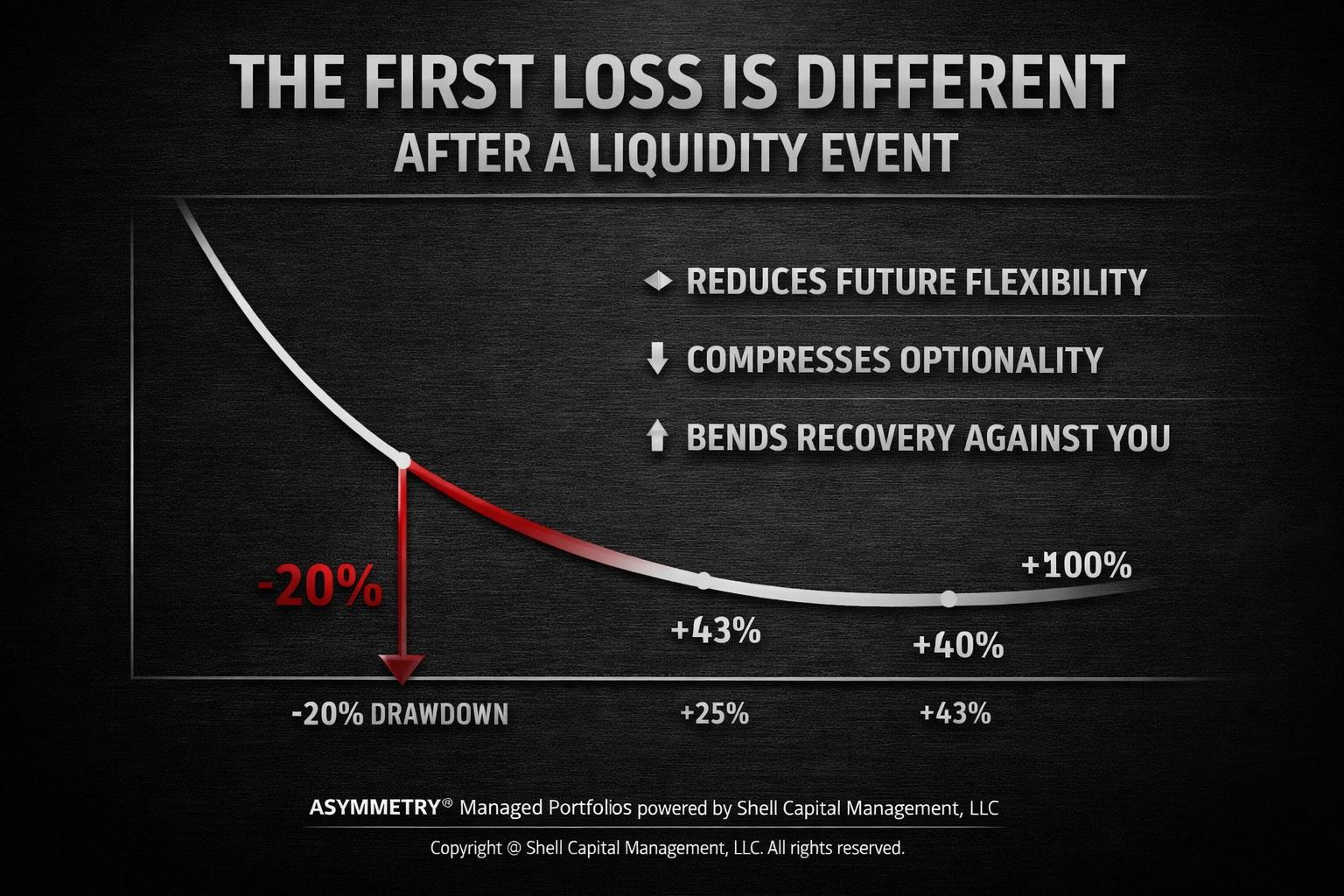

A 20% loss is no longer just a temporary decline. It’s a permanent impairment unless recovered—and recovery isn’t just a function of return, it’s a function of time and sequence.

This is where most frameworks break.

From a mathematical standpoint, losses and gains are not symmetric.

A -10% loss requires +11% to recover. A -20% loss requires +25%. A -30% loss requires +43%. A -50% loss requires +100%.

The curve bends against you.

But the real issue isn’t just the math.

It’s the context.

Before a triggering event, recovery is supported by ongoing income. Capital can be replenished. Time works in your favor.

After the event, recovery depends on the capital itself—often while it’s being drawn down for lifestyle, taxes, or reinvestment.

Now the base is shrinking while you’re trying to rebuild it.

This is sequence risk.

Returns don’t occur in isolation. The order matters. A negative sequence early—immediately following a triggering event—has an outsized impact because it reduces the capital base before it has a chance to compound.

Same average return. Different outcome.

That’s the asymmetry most portfolios ignore.

From an ASYMMETRY® perspective, this is where convexity becomes non-negotiable.

If downside isn’t defined, you’re exposed to outcomes that require increasingly improbable recoveries.

If downside is defined in advance—through position sizing, exit discipline, and dynamic exposure management—you change the structure:

Losses are contained. Recovery requirements stay within a manageable range. Optionality is preserved.

The objective isn’t to avoid losses entirely.

It’s to avoid losses that change the trajectory of the portfolio.

Because after a triggering event, the margin for error is smaller than it appears.

A 20% drawdown isn’t just a number.

It’s a reduction in future flexibility. It’s a compression of optionality. It’s time you may not want to spend recovering.

Boundary conditions matter.

This isn’t about eliminating risk. It’s about recognizing that the same level of volatility produces different consequences depending on the structure behind it.

If the portfolio assumes recovery is always available, it’s implicitly assuming time, income, and stability—all of which may no longer be present in the same way.

That’s the disconnect.

For operators transitioning to managing capital, this is the shift:

You’re no longer optimizing for average returns.

You’re managing the path those returns take.

Because the first loss after a triggering event doesn’t just reduce capital.

It changes what’s required to move forward.

Mike Shell is the founder of Shell Capital Management, LLC, a registered investment adviser built specifically for business owners approaching a liquidity event. As a fiduciary—and a business owner for over two decades—he operates on the same side of the table, representing the owner’s interests, not the transaction. That distinction becomes critical when the difference isn’t just valuation, but how much of that value you actually keep, control, and compound after the exit.

Shell Capital was built on advising owners through exit planning, orchestrating liquidity events, and then managing the capital that follows with a family office mindset—focused on downside protection, optionality, and long-term control of wealth. Because the capital you realize becomes the capital we manage, our incentives are fully aligned: we don’t get paid for a deal—we get paid for what happens after it.

Most owners only exit once. The margin for error is small, and the cost of getting it wrong is permanent. If you’re within range of a potential exit, this is the phase where outcomes are decided.