The Operator-to-Investor Transition Most People Miss

Most people assume that if they were successful building a business, they’ll be successful managing the proceeds.

That assumption is where the problem starts.

Because the skill set that creates wealth is not the same skill set required to preserve and compound it.

In many ways, it’s the opposite.

Operators are rewarded for concentration, speed, and conviction.

You allocate capital aggressively into what you know best. You reinvest. You take asymmetric bets on your own capabilities. You accept volatility because the upside justifies it—and because you can influence outcomes.

That’s how businesses are built.

But after a triggering event, the structure changes.

You’re no longer inside the system. You’re exposed to it.

You can’t control markets. You can’t accelerate outcomes through effort. You can’t recover from mistakes with the same reliability.

And yet, many portfolios are still run with an operator’s mindset.

That’s the mismatch.

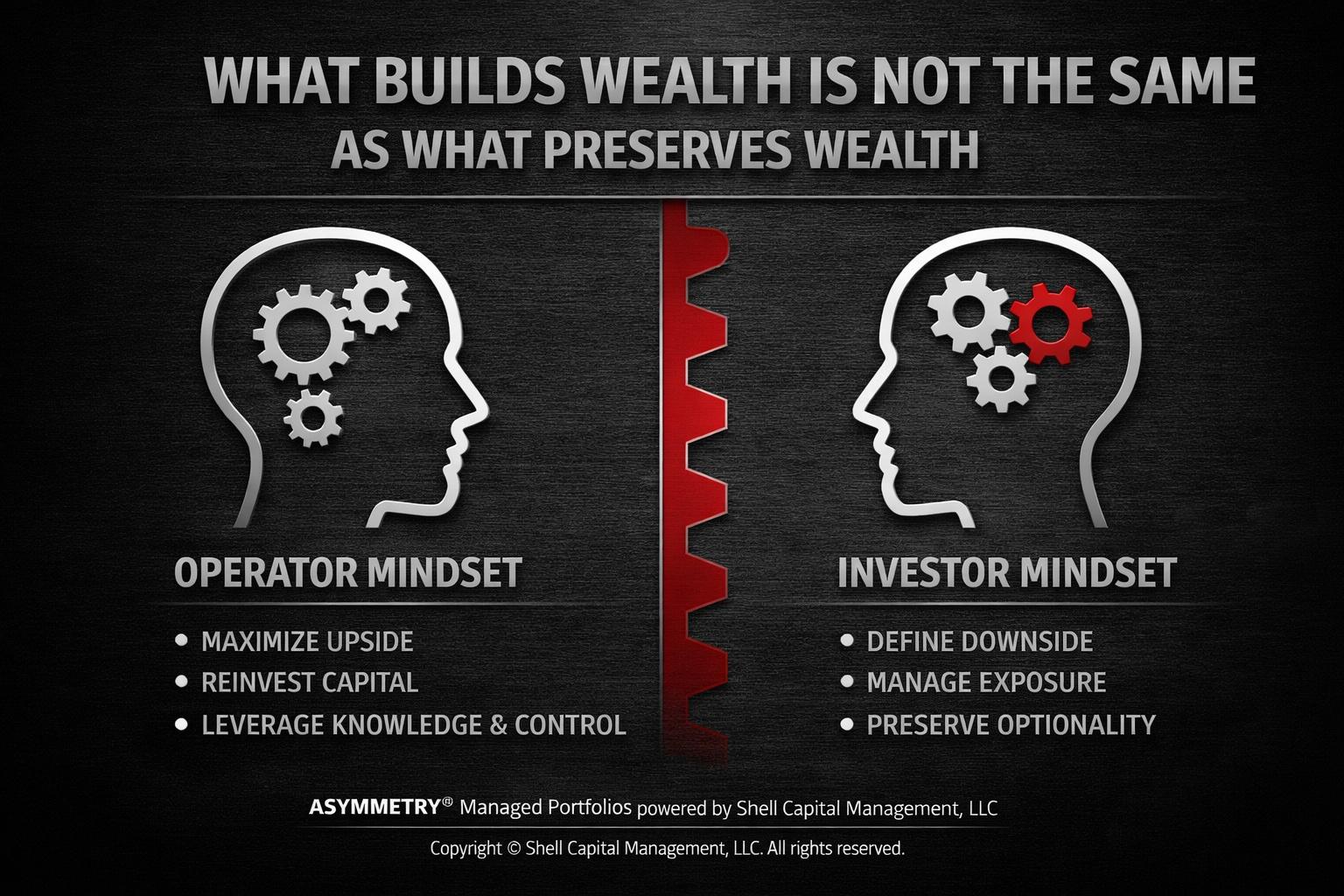

From a first-principles perspective, the operator-to-investor transition is a shift in objective function.

Before:

Maximize upside.

Reinvest capital.

Leverage knowledge and control.

After:

Define downside.

Manage exposure.

Preserve optionality.

Same capital.

Different mandate.

This is where most portfolios quietly take on more risk than intended.

An operator is conditioned to lean in when things are working. To double down. To press advantage.

In markets, that behavior often shows up as:

- concentration in a few ideas

- delayed risk reduction

- tolerance for drawdowns under the assumption of recovery

But after a liquidity event, those assumptions no longer hold in the same way.

Because the consequences have changed.

A drawdown isn’t just volatility. It’s a reduction in future flexibility. It’s time spent recovering instead of compounding. It’s optionality that may not come back.

This is where asymmetry becomes the governing principle.

From an ASYMMETRY® lens, the objective isn’t to maximize return—it’s to structure exposure so that downside is defined while upside remains open.

That requires a different discipline:

- Position sizing becomes primary.

- Exit levels are defined in advance.

- Portfolio risk is managed continuously, not periodically.

- Liquidity and volatility are monitored as core variables, not afterthoughts.

This isn’t about being conservative.

It’s about being precise.

Because the investor’s constraint isn’t a lack of opportunity.

It’s the cost of being wrong.

Boundary conditions matter.

Not every operator struggles with this transition. The ones who adapt recognize that their edge has changed.

They shift from controlling outcomes to controlling exposure.

They stop asking, “What can I make?” and start asking, “What can I lose—and is that acceptable?”

That’s the inflection point.

For physicians, business owners, executives—anyone who has converted years of effort into a pool of capital—the transition is unavoidable.

You don’t need to abandon the traits that built success.

But you do need to redirect them.

Discipline becomes risk management.

Conviction becomes position sizing.

Speed becomes decision clarity under uncertainty.

Because after a triggering event, the goal isn’t to build capital.

It’s to ensure it endures.

And that requires operating under a completely different set of rules.

Mike Shell is the founder of Shell Capital Management, LLC, a registered investment adviser built specifically for business owners approaching a liquidity event. As a fiduciary—and a business owner for over two decades—he operates on the same side of the table, representing the owner’s interests, not the transaction. That distinction becomes critical when the difference isn’t just valuation, but how much of that value you actually keep, control, and compound after the exit.

Shell Capital was built on advising owners through exit planning, orchestrating liquidity events, and then managing the capital that follows with a family office mindset—focused on downside protection, optionality, and long-term control of wealth. Because the capital you realize becomes the capital we manage, our incentives are fully aligned: we don’t get paid for a deal—we get paid for what happens after it.

Most owners only exit once. The margin for error is small, and the cost of getting it wrong is permanent. If you’re within range of a potential exit, this is the phase where outcomes are decided.