Volatility Becomes a Liability After a Triggering Event

Volatility is often framed as a feature.

A necessary tradeoff for higher returns. A source of opportunity. Something to be endured in pursuit of long-term growth.

That framing works—until the structure changes.

After a triggering event, volatility stops behaving like a feature.

It becomes a liability.

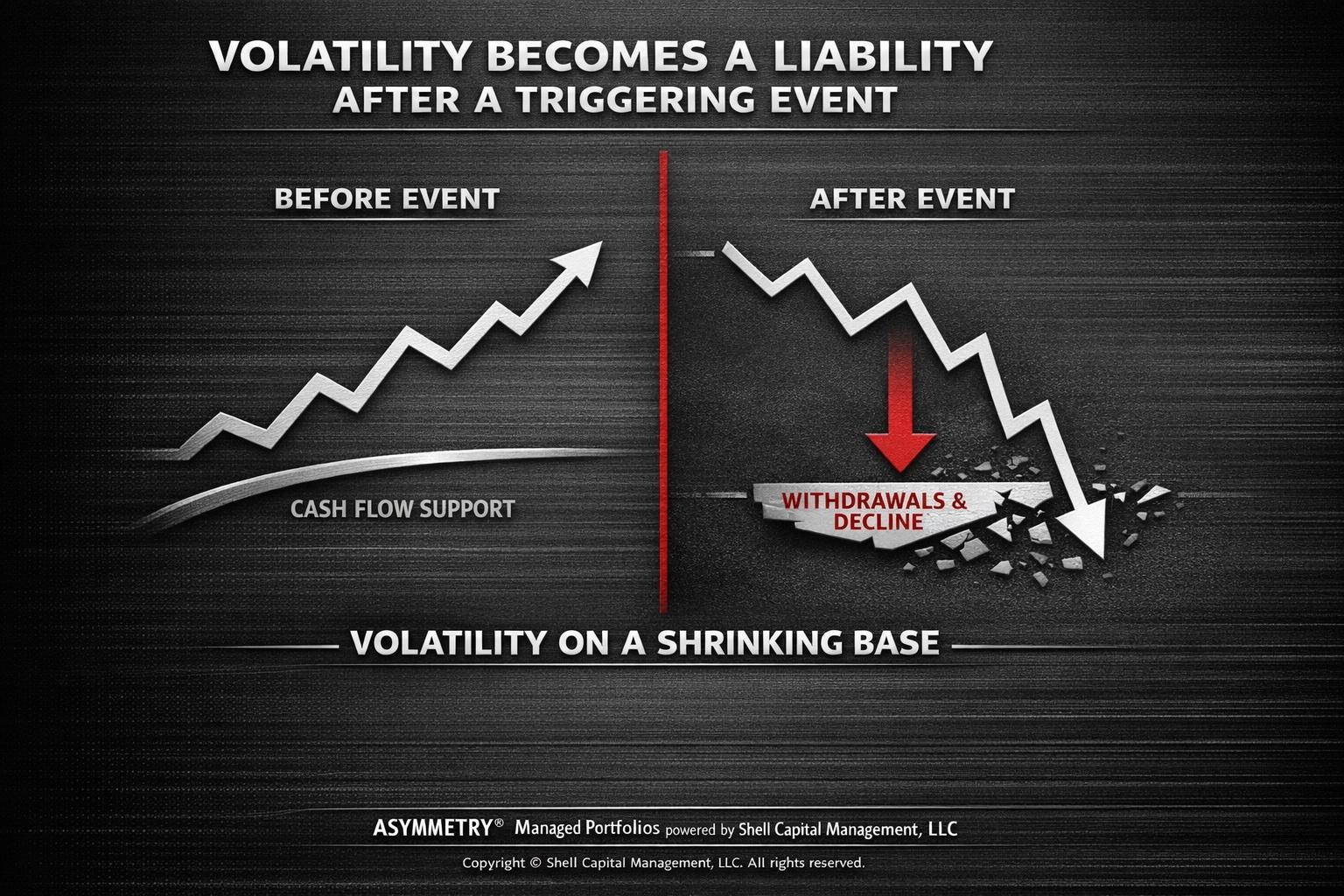

Before the event, fluctuations in portfolio value are buffered by time and income. Drawdowns can be tolerated because capital is still being replenished. Volatility is uncomfortable, but it’s survivable.

After the event, that buffer is gone.

The portfolio is no longer being supported by external cash flows in the same way. In many cases, it’s being drawn from.

Now volatility interacts directly with the capital base.

And that interaction is where the problem emerges.

From a first-principles perspective, volatility isn’t just movement—it’s dispersion of outcomes.

The wider the dispersion, the greater the probability of large deviations from the expected path.

In an accumulation phase, those deviations are manageable.

In a post-triggering-event phase, they carry asymmetric consequences.

Because volatility increases the likelihood of drawdowns—and drawdowns, when combined with withdrawals, create a compounding drag on recovery.

This is often misunderstood.

It’s not volatility alone that creates risk.

It’s volatility applied to a shrinking base.

If a portfolio declines while capital is being withdrawn, the recovery requirement increases at the same time the capital available to recover is decreasing.

That’s a structural headwind.

Same average return. Worse outcome.

This is why volatility tolerance and risk capacity diverge after a triggering event.

Someone may still feel comfortable with market swings—but the portfolio can no longer absorb them in the same way.

That distinction is critical.

From an ASYMMETRY® perspective, unmanaged volatility introduces negative convexity.

Losses expand faster than gains can recover them. The distribution of outcomes skews against the investor—not because the expected return changed, but because the path did.

If downside isn’t defined, volatility determines outcomes.

If downside is defined, volatility can be managed, contained, and in some cases even used as a source of optionality.

That’s the difference.

Boundary conditions matter.

This isn’t about eliminating volatility. That’s neither realistic nor necessary.

It’s about controlling how much volatility the portfolio is exposed to—and under what conditions.

What level of drawdown is acceptable? How does the portfolio behave during volatility expansion? What happens if volatility clusters rather than mean-reverts?

If those questions aren’t answered in advance, the portfolio is implicitly exposed to outcomes that may not be tolerable.

After a triggering event, the objective shifts.

It’s no longer about riding through volatility.

It’s about ensuring volatility doesn’t dictate the outcome.

That requires:

- defining downside at the position level

- managing portfolio risk continuously

- adjusting exposure as volatility regimes change

- maintaining liquidity to preserve optionality

Because volatility isn’t inherently good or bad.

But after a triggering event, unmanaged volatility becomes one of the fastest ways to turn temporary declines into permanent consequences.

And that’s a risk most portfolios aren’t built to handle.

Mike Shell is the founder of Shell Capital Management, LLC, a registered investment adviser built specifically for business owners approaching a liquidity event. As a fiduciary—and a business owner for over two decades—he operates on the same side of the table, representing the owner’s interests, not the transaction. That distinction becomes critical when the difference isn’t just valuation, but how much of that value you actually keep, control, and compound after the exit.

Shell Capital was built on advising owners through exit planning, orchestrating liquidity events, and then managing the capital that follows with a family office mindset—focused on downside protection, optionality, and long-term control of wealth. Because the capital you realize becomes the capital we manage, our incentives are fully aligned: we don’t get paid for a deal—we get paid for what happens after it.

Most owners only exit once. The margin for error is small, and the cost of getting it wrong is permanent. If you’re within range of a potential exit, this is the phase where outcomes are decided.