Why Most Portfolios Are Built for Average Markets, Not Adverse Ones

Most portfolios are designed around what usually happens.

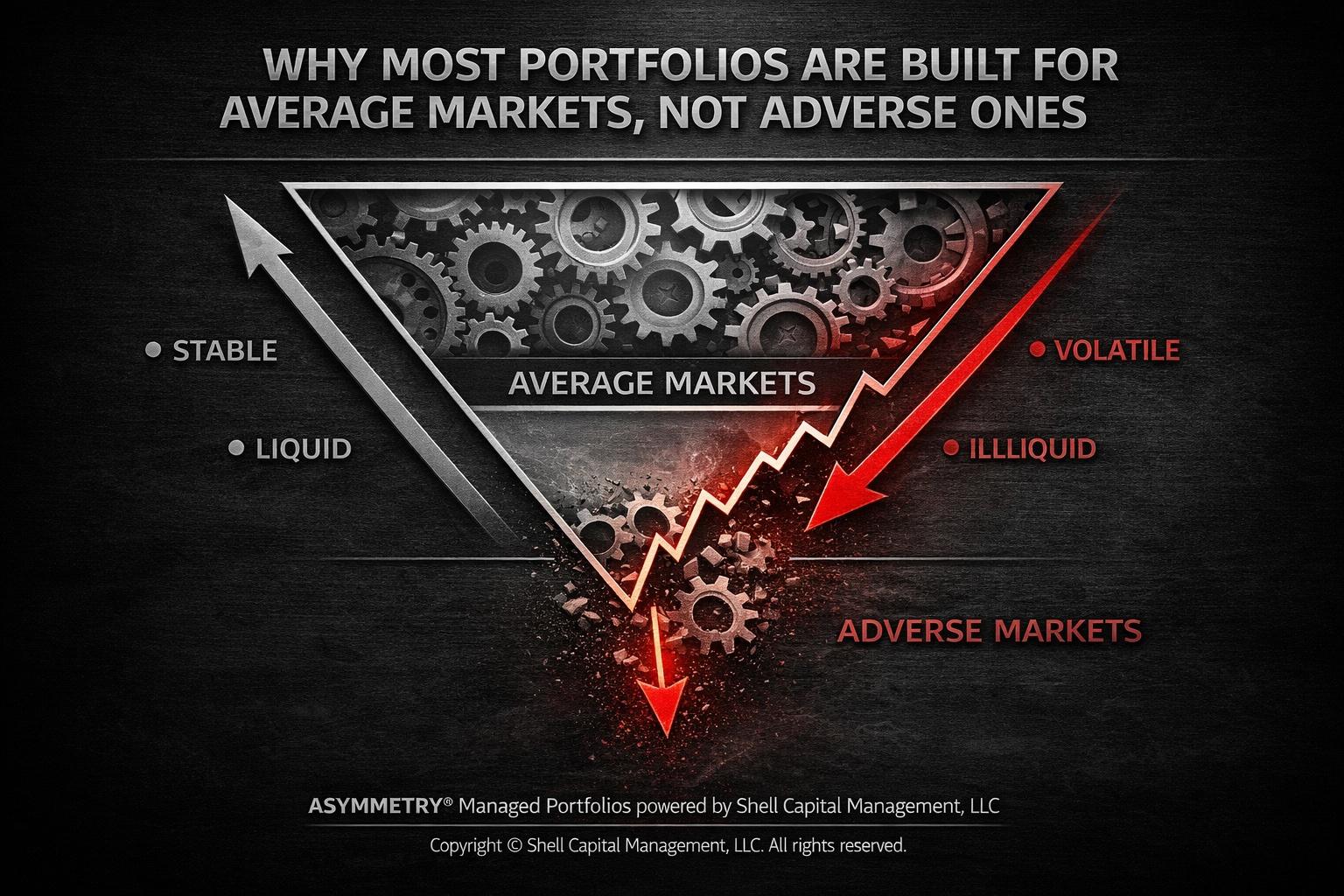

Stable growth. Moderate volatility. Diversification across asset classes that don’t move in perfect sync.

On paper, it looks balanced.

In practice, it’s conditional.

And who wants to "balance" profit and loss? We want less of one and more of the other.

Because the assumptions behind most portfolios only hold in average environments.

Correlations remain low. Liquidity is available. Volatility is contained. Buyers show up when prices fall.

But adverse markets don’t operate that way.

That’s the disconnect.

The misconception is that diversification protects against risk.

It doesn’t.

It protects against normal variation—not structural stress.

From a first-principles perspective, most portfolios are optimized for expected outcomes, not extreme ones.

They assume:

- correlations remain stable

- volatility is mean-reverting

- liquidity is continuous

- drawdowns are temporary

Those assumptions break precisely when they matter most.

In adverse conditions, correlations don’t diversify—they converge.

Assets that appeared independent begin to move together. Risk compresses into a single direction. What looked like multiple return drivers becomes one concentrated exposure.

At the same time, liquidity thins.

Spreads widen. Forced sellers emerge. Price becomes a function of urgency, not value.

Volatility expands—not as noise, but as a structural shift in behavior.

This is where asymmetry turns against static portfolios.

Because the downside is no longer defined by historical averages—it’s defined by current conditions.

From an ASYMMETRY® lens, the issue isn’t that portfolios decline.

It’s that they decline more than expected under conditions that weren’t explicitly accounted for.

That’s a design flaw.

If downside isn’t defined in advance, then risk is being outsourced to the environment.

And the environment doesn’t stay stable.

This is especially relevant after a triggering event.

Because the consequences of adverse markets are no longer abstract.

A portfolio built for average conditions may perform acceptably most of the time—but it can experience disproportionate damage during the exact periods when recovery capacity is most constrained.

That’s where sequence risk and structural fragility intersect.

Boundary conditions matter.

This isn’t about predicting crises.

It’s about recognizing that portfolios should be evaluated based on how they behave when assumptions fail.

What happens when correlations rise toward 1? What happens when volatility expands rapidly? What happens when liquidity disappears?

If the answer is “the portfolio absorbs a large, undefined loss,” then the structure is incomplete.

From a portfolio management standpoint, the objective shifts:

Not maximizing performance in normal environments—but maintaining control in abnormal ones.

That requires:

- defining downside at the position level

- managing portfolio risk as a system, not a collection of holdings

- adjusting exposure dynamically as conditions change

- structuring for convexity so adverse conditions don’t create irreversible outcomes

Because adverse markets aren’t anomalies.

They’re part of the distribution.

And they’re the part that determines long-term outcomes.

Most portfolios are built to look efficient when conditions are stable.

Few are built to remain intact when they aren’t.

That difference is where asymmetry lives.

Mike Shell is the founder of Shell Capital Management, LLC, a registered investment adviser built specifically for business owners approaching a liquidity event. As a fiduciary—and a business owner for over two decades—he operates on the same side of the table, representing the owner’s interests, not the transaction. That distinction becomes critical when the difference isn’t just valuation, but how much of that value you actually keep, control, and compound after the exit.

Shell Capital was built on advising owners through exit planning, orchestrating liquidity events, and then managing the capital that follows with a family office mindset—focused on downside protection, optionality, and long-term control of wealth. Because the capital you realize becomes the capital we manage, our incentives are fully aligned: we don’t get paid for a deal—we get paid for what happens after it.

Most owners only exit once. The margin for error is small, and the cost of getting it wrong is permanent. If you’re within range of a potential exit, this is the phase where outcomes are decided.