Reflexivity in Financial Markets – How Feedback Loops Drive Asymmetry

Reflexivity in Financial Markets – How Feedback Loops Drive Asymmetry

“The key to understanding market behavior is recognizing that perception and reality can influence each other.” – George Soros

Reflexivity is not just a philosophical concept—it’s a practical lens through which active investors can spot asymmetric opportunities, navigate volatility, and potentially front-run inflection points.

Let's explore what reflexivity is, why it matters in trading and investing, and how to identify it in real time.

What Is Reflexivity?

Reflexivity, in finance, describes a feedback loop between perception and fundamentals. It’s the idea that market participants' beliefs and behaviors can influence the reality they are trying to predict, especially in asset prices.

This concept was made famous by George Soros, who applied it to currency markets, equity bubbles, and credit cycles.

In a reflexive market, prices don’t just reflect reality—they shape it.

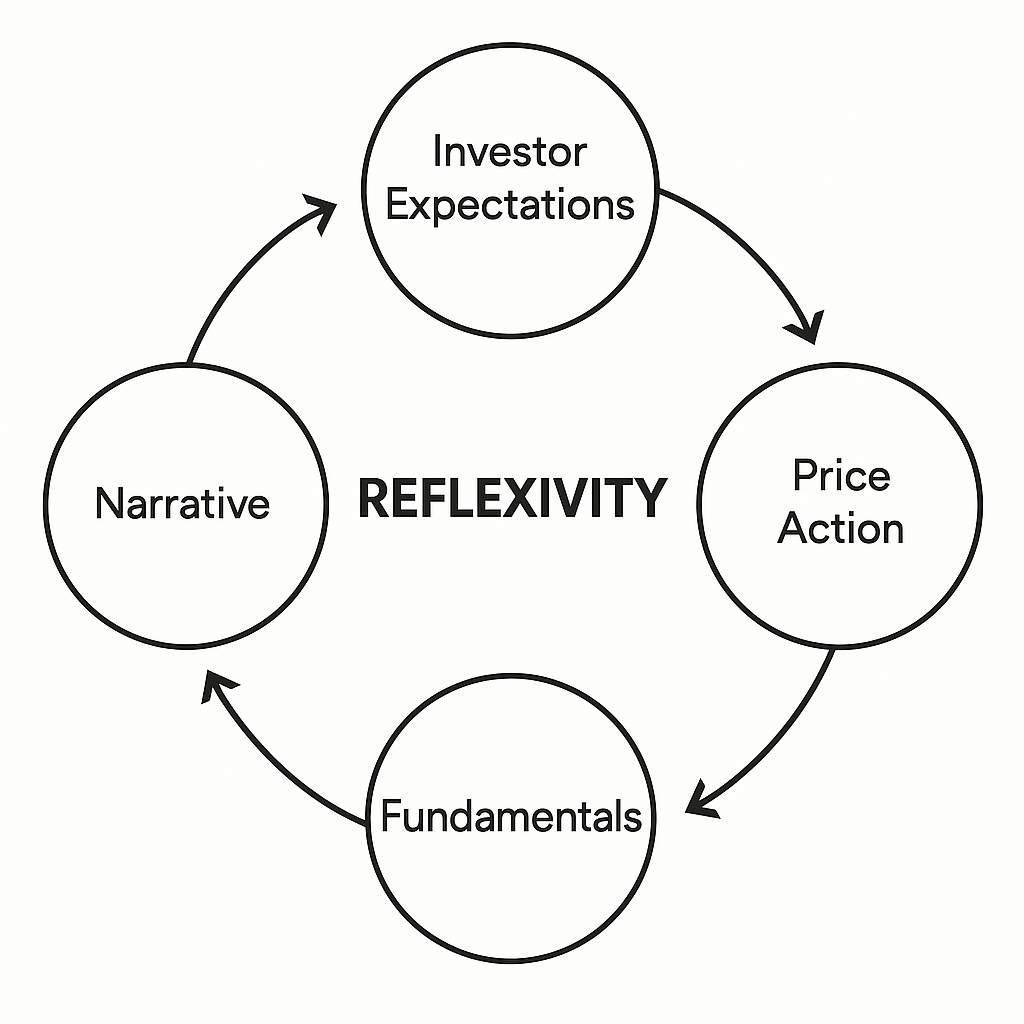

The Core Feedback Loop

Reflexivity has two phases:

- Cognitive Function – Investors form views about the market or economy.

- Participating Function – Their actions based on those views (buying, selling, hedging, reallocating) influence market outcomes.

The loop:

- Investor expectations change →

- Positioning shifts (flows, leverage, sentiment) →

- Price action moves →

- Narrative adjusts →

- Fundamentals adapt →

- Investor expectations change again…

Example: Reflexivity in a Bubble

Let’s say investors believe tech stocks will outperform. As they pile into them:

- Prices rise

- Momentum strategies amplify the trend

- Companies issue equity at high valuations

- They spend that capital on expansion, R&D, or buybacks

- Earnings improve—validating the original belief

But this isn’t an efficient market. It’s a reflexive loop, where perception created the fundamentals, not the other way around.

Reflexivity vs. Efficient Market Hypothesis (EMH)

- EMH assumes prices reflect all known information.

- Reflexivity suggests prices distort reality and help create the future.

This has major implications for how you identify asymmetric trades:

- EMH says you can’t beat the market.

- Reflexivity says if you understand the feedback loop before others, you can.

Where Reflexivity Shows Up

Reflexivity is present in any market with human feedback and flow-driven behavior, especially when leverage, liquidity, and narrative converge. Common examples include:

- Momentum-driven equity bubbles

- Credit booms and busts

- Currency crises

- Housing markets

- ETF flows into concentrated sectors

- Zero DTE option flow impact on S&P 500 price action

Reflexivity and Asymmetric Trading

For asymmetric investors, reflexivity is a source of optionality and convex payoffs. Why?

- Early perception shifts often lead to outsized price moves once reinforced.

- Reflexive trades have expanding payoff profiles when the loop builds.

- You can structure positions to benefit from continuation or collapse of the loop, using predefined risk (stop losses or options).

Practical Signs of Reflexivity in Action

Here’s how you may spot a reflexive dynamic early:

- Price moves precede fundamental justification

(e.g., a stock rallies before earnings revisions catch up) - Narratives build momentum post-price move

(e.g., analysts upgrade after a 20% rally) - Capital inflows follow performance

(e.g., trend-chasing behavior in sector ETFs) - Volatility suppression through hedging feedback

(e.g., option dealers buying futures to hedge short gamma) - Policy and market reaction blur

(e.g., central banks reacting to asset prices they’re also influencing)

Reflexivity and Risk Management

When reflexivity is at work:

- Price trends can overshoot, creating opportunity but also risk.

- Downside gaps can happen fast if the loop breaks (deleveraging, narrative collapse).

- Reflexive environments demand predefined exits, tight position sizing, and portfolio heat limits to control compounding drag.

Reflexivity explains why trend following works—but also why reversals are violent.

George Soros’s Reflexive Trades

Soros famously used reflexivity to time:

- The British pound short in 1992 (“broke the Bank of England”)

- The tech bubble short in 2000

- The housing credit long in 2009

What made these trades asymmetric? He didn’t just bet on fundamentals—he bet on when perceptions would reverse and unravel the loop.

Key Takeaways for Asymmetric Investors

- Reflexivity reveals where perception becomes reality.

This can lead to explosive upside (or crash risk). - Watch flows and positioning, not just fundamentals.

Institutional fund flows, option dealer hedging, ETF rotation—all feed reflexivity. - Structure trades for convexity.

Use options, stop losses, and position sizing to define risk and leave upside open. - The edge is in timing perception shifts.

Reflexivity gives traders a chance to be early, not just right.

The Bottom Line

Reflexivity is more than a Soros buzzword—it’s a market structure principle that helps explain both bubbles and crashes, trend persistence, and volatility clusters. By mastering reflexivity, asymmetric investors can better:

- Anticipate feedback loops before they peak

- Structure convex trades when perception drives price

- Adapt faster to shifts in narrative, positioning, and risk appetite

If you want to pursue asymmetric investment returns, reflexivity is a framework you can’t afford to ignore.