When the trends change direction, I change my direction, what do you do?

When the trends change direction, I change my direction. What do you do?

That's my version of the famous quote often attributed to John Maynard Keynes,

"When the facts change, I change my mind. What do you do, sir?"

According to Quote Investigator, with boldface added to excerpts by me:

In 1924 John Maynard Keynes published an essay titled “Investment Policy for Insurance Companies” in “The Nation and Athenaeum” of London. Keynes contended that an insurance company must employ an active investment policy. The company must maintain constant vigilance and revise preconceived ideas in response to changes in external situations.

Keynes penned a statement that partially matched the expression under examination. He suggested that a successful investor must be willing change an opinion when facts and circumstances change.

Keynes goes on to say, and it's so good I had to bold it all:

"Unfortunately, it is not possible to make oneself permanently secure by any policy of inaction whatever. The idea which some people seem to entertain that an active policy involves taking more risks than an inactive policy is exactly the opposite of the truth. The inactive investor who takes up an obstinate attitude about his holdings and refuses to change his opinion merely because facts and circumstances have changed is the one who in the long run comes to grievous loss."

John Maynard Keynes wrote that in 1924, a century ago, yet most investment managers have yet to develop a system to tactical trading decisions or risk management systems for drawdown control to limit equity declines.

Keynes fundamentally changed the theory and practice of macroeconomics and the economic policies of governments. Originally trained in mathematics, he built on and greatly refined earlier work on the causes of business cycles.

At Shell Capital, we change when the facts change, and I've been adapting to changing trends and market dynamics for over two decades.

Since I shared the last market trend and momentum observation, A directional, multi-dimensional momentum of the U.S. stock market for trend following, the U.S. stock market has reversed its trend from up to down.

A week ago I shared on Twitter;

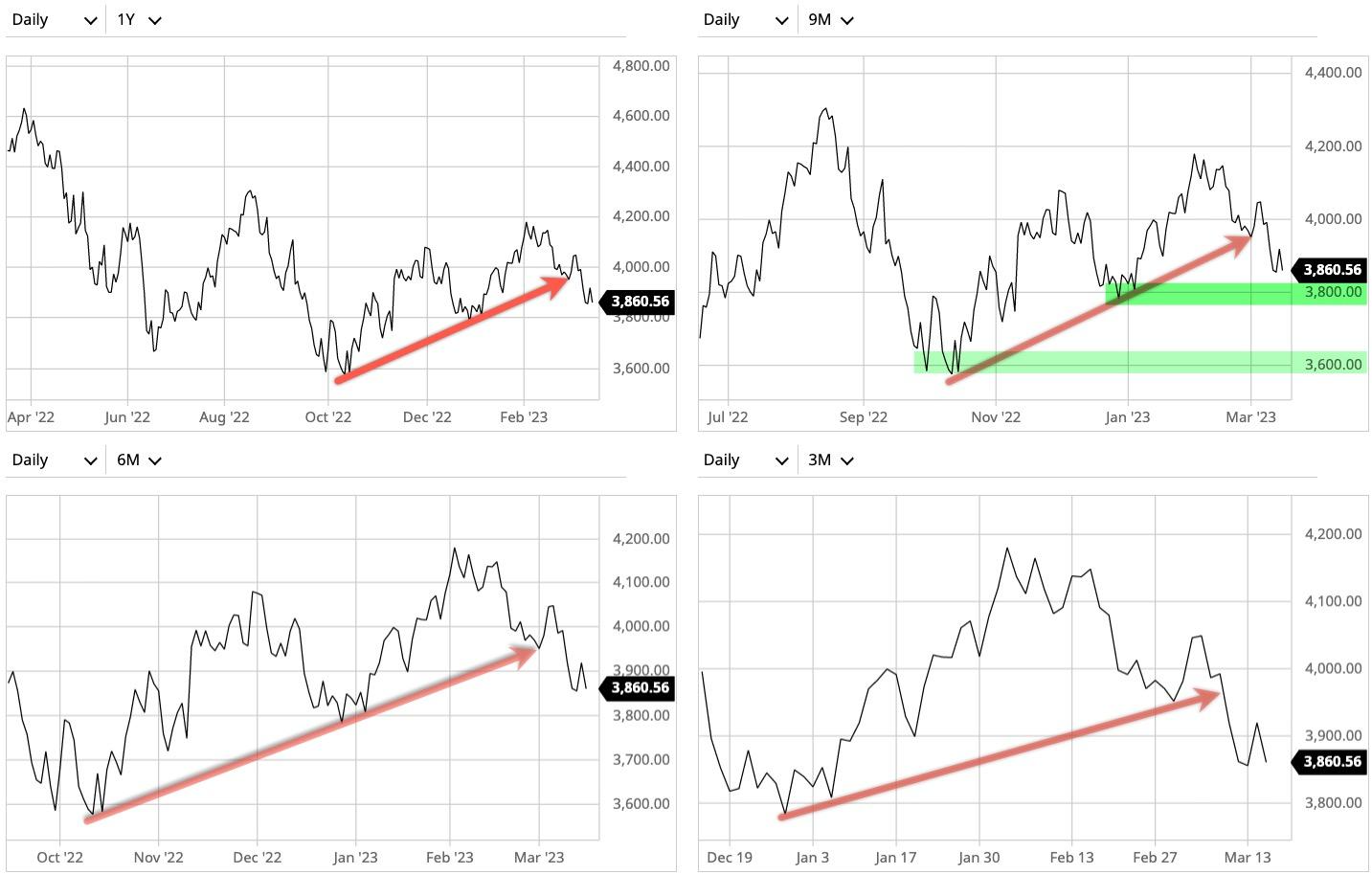

The Barchart below shows the S&P 500 stock index over 12, 9, 6, and 3-month momentum, or rate of change, and the directional trend is labeled with simple trend lines.

While momentum as measured by rate of change of the last 12, 9, 6, and 3 months remains positive, the near term direction the short-term U.S. stock market trend is down.

Based on this trend analysis alone, the stock market looks likely to find some buying interest that could support prices around ~3783 into the 3800 area amid a lot prior price congestion last December. At the same time, short-term velocity indicates the index is getting closer to oversold.

Given the directional trend change the last week, we've been mostly positioned in short term U.S. Treasury backed money markets, where rates are yielding over 4% now.

I hinted on Twitter the bond market was telling us something:

When rates shoot up so fast, it's the market waving dollar bills at us, enticing us with higher yields on safe U.S.-backed money.

The recent bank failures elevates the possibility of more panic selling and a shock or crash if there are more failures to come.

I've been saying for more than a year that this may be a prolonged bear market, especially if the economy shifts to a recession. There will be many short-term swings up and down along the way, and these cycles provide risks and rewards for tactical traders.

I'm man + machine, so we have robust systems with a range of inputs like the directional price trend, momentum, volatility, and investor sentiment. So, this is just a succinct commentary about the overall stock market trend, far from a complete review of my ASYMMETRY® systems.

Whipsaws are much more common in bear markets and non-trending markets that swing up and down.

In fact, non-trending markets are hostile conditions for trend-following systems that aim to enter after a price trends up, and exits after a position trends down. This is when we may shift to counter-trend systems that buy short-term oversold and sell-short term overbought, which have a better edge in non-trending markets, but nothing is ever perfect.

If we have a positive mathematical expectation, we don't need the perfection of winning every position, our edge is the average gains are larger than the average loss, for asymmetry.

I'm now looking for asymmetric risk/reward opportunities across global markets, and when prices spread out the dispersion may provide it.

Mike Shell

Mike Shell is the founder and Chief Investment Officer of Shell Capital Management, LLC, and the portfolio manager of ASYMMETRY® Managed Portfolios. Mike Shell and Shell Capital Management, LLC is a registered investment advisor focused on asymmetric risk-reward and absolute return strategies and provides investment advice and portfolio management only to clients with a signed and executed investment management agreement. The observations shared on this website are for general information only and should not be construed as investment advice to buy or sell any security. This information does not suggest in any way that any graph, chart, or formula offered can solely guide an investor as to which securities to buy or sell, or when to buy or sell them. Securities reflected are not intended to represent any client holdings or recommendations made by the firm. In the event any past specific recommendations are referred to inadvertently, a list of all recommendations made by the company within at least the prior one-year period may be furnished upon request. It should not be assumed that recommendations made in the future will be profitable or will equal the performance of the securities on the list. Any opinions expressed may change as subsequent conditions change. Please do not make any investment decisions based on such information, as it is not advice and is subject to change without notice. Investing involves risk, including the potential loss of principal an investor must be willing to bear. Past performance is no guarantee of future results. All information and data are deemed reliable but are not guaranteed and should be independently verified. The presence of this website on the Internet shall in no direct or indirect way raise an implication that Shell Capital Management, LLC is offering to sell or soliciting to sell advisory services to residents of any state in which the firm is not registered as an investment advisor. The views and opinions expressed in ASYMMETRY® Observations are those of the authors and do not necessarily reflect the position of Shell Capital Management, LLC. The use of this website is subject to its terms and conditions.