Why Did VXX and VIXY Diverge in 2022?

Tactical traders and hedge fund managers seeking asymmetric hedging opportunities can use VXX and VIXY to capitalize on volatility spikes while maintaining limited downside risk. Since both ETFs track short-term VIX futures, they tend to rise sharply when market volatility surges, making them potential hedges against equity drawdowns. However, due to the natural decay from roll costs, holding them for long periods can be costly. The key to structuring an asymmetric hedge with VXX or VIXY is to establish a predefined risk entry with asymmetric upside potential—such as using options instead of outright positions or timing entries around expected volatility catalysts. By combining a small, well-sized position with a predefined exit strategy, we can minimize losses while positioning for an exponential upside move if volatility spikes. This tactical approach transforms VXX and VIXY from decaying assets into tactical tools for hedging and profiting from market stress events.

I started looking to gain exposure to long volatility via the ETFs/ETNs when they first launched after the 2008 crash, and they've remained in our arsenal since. However, we've seen many structural issues along the way, so it's essential to know your weapon.

In 2022, we observed another divergence worth understanding.

VXX and VIXY are two exchange-traded products (ETPs) designed to provide exposure to short-term VIX futures, making them popular among traders looking to hedge volatility or speculate on market turbulence. Despite tracking the same underlying index, these two products experienced a significant divergence in performance during 2022. This divergence can be attributed to a combination of structural differences, market events, and liquidity factors that temporarily broke their usual price relationship.

Structural Differences: ETN vs. ETF

At a high level, both VXX and VIXY are designed to follow the S&P 500 VIX Short-Term Futures Index, which rolls exposure between the first and second month VIX futures contracts. However, their structures differ:

- VXX is an exchange-traded note (ETN) issued by Barclays. This means it is an unsecured debt obligation, with no actual holdings of VIX futures—investors rely on Barclays to deliver returns based on the index.

- VIXY is an exchange-traded fund (ETF) managed by ProShares. Unlike an ETN, it holds actual VIX futures contracts, requiring continuous rebalancing and subjecting it to tracking errors.

In normal conditions, both should perform similarly, as the underlying index exposure is the same. However, due to structural roll decay, both products tend to lose value over time unless volatility spikes. This decay occurs because the VIX futures curve is typically in contango (longer-term futures are more expensive than near-term contracts), meaning these funds regularly sell cheaper near-term contracts and buy pricier longer-term ones, incurring losses.

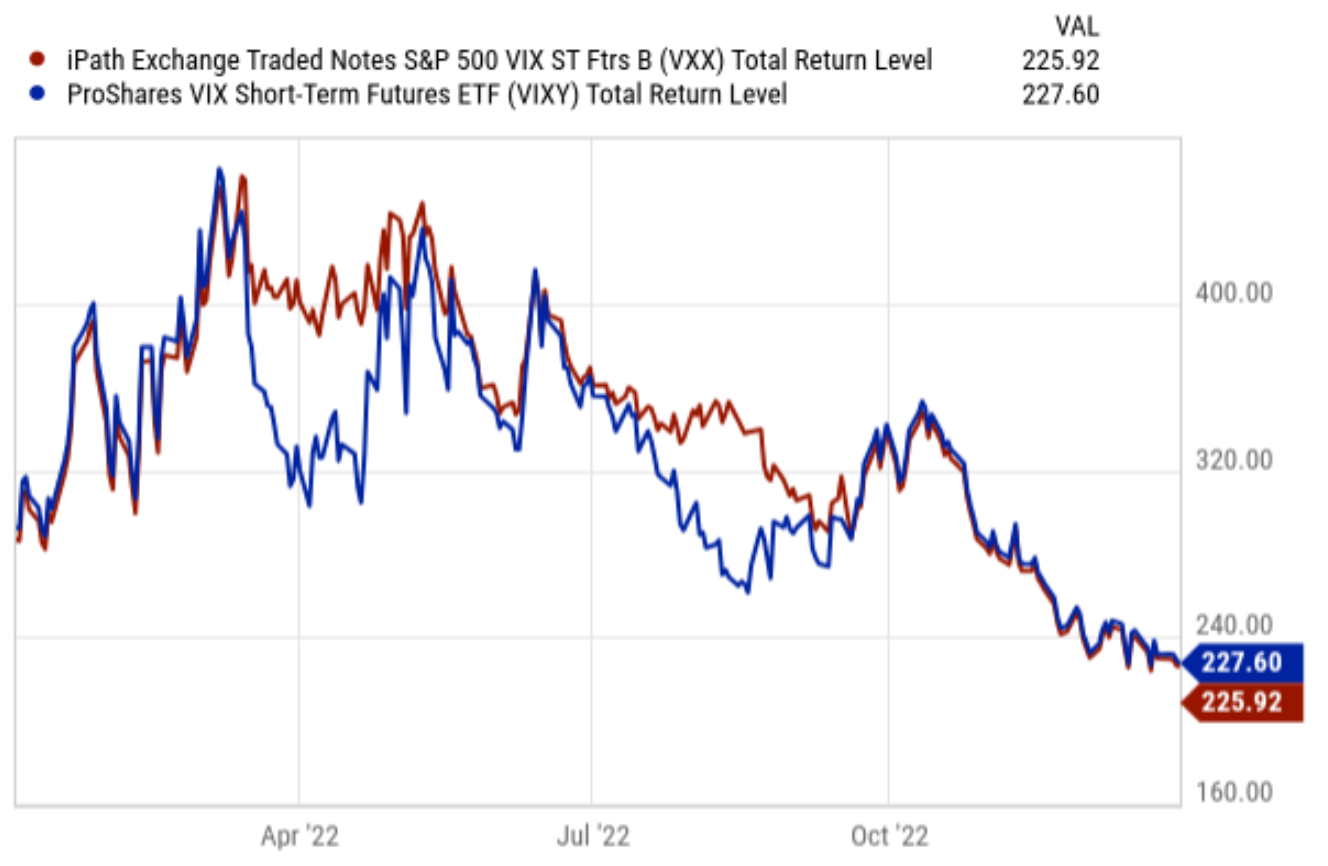

Under normal market conditions, arbitrage mechanisms ensure that both VXX and VIXY trade close to their net asset value (NAV). But in March 2022, this mechanism broke down for VXX, creating a major divergence.

Market Events Driving Volatility in 2022

Several macroeconomic and geopolitical events shaped volatility trends in 2022:

- January–March: Rising inflation, aggressive Fed tightening signals, and geopolitical tensions (particularly Russia’s invasion of Ukraine in late February) led to major spikes in volatility. The VIX surged to 37.5 on February 24, pushing both VXX and VIXY higher.

- April–June: As markets digested the rate hikes and the bear market deepened, volatility remained elevated. However, because the VIX futures curve remained in contango, VXX and VIXY faced the usual decay from roll costs.

- September–December: The Federal Reserve’s continued rate hikes, a strong labor market, and recession fears contributed to periodic volatility spikes, but with no sustained “super spike,” both VXX and VIXY continued trending downward due to structural decay.

The March 2022 Barclays Issuance Halt – The Main Cause of Divergence

The key event that broke the link between VXX and VIXY occurred on March 14, 2022, when Barclays suspended new share creation for VXX. This meant that new VXX ETNs could no longer be issued, turning VXX into a “scarce” product.

Since VXX’s supply was now fixed while demand remained strong, it started trading at a massive premium to its actual value. On March 14–15, VXX surged nearly 60% in two days, while VIXY remained rationally priced based on VIX futures. This dislocation occurred because:

- No new VXX ETNs could be created to meet demand.

- Short sellers of VXX faced a squeeze, as they could no longer access new shares to cover positions.

- Speculators piled into VXX, betting the premium would rise further.

For months, VXX traded well above its fair value, whereas VIXY continued tracking its index properly. This divergence persisted until September 2022, when Barclays finally resumed VXX issuance. At that point, arbitrage forces quickly collapsed the premium, bringing VXX back in line with VIXY.

Liquidity and Trading Factors That Exacerbated the Divergence

Liquidity and trading mechanics played a crucial role in the March–September dislocation:

- Creation/Redemption Mechanisms: VIXY’s ETF structure allowed authorized participants to create or redeem shares to keep prices aligned with NAV. VXX, however, relied on Barclays issuing new ETNs, which was suddenly unavailable.

- Short Interest and Squeeze Dynamics: Before the halt, nearly 90% of VXX’s float was sold short. When the creation mechanism broke, short sellers had no way to create new shares to cover, fueling a dramatic price surge.

- Market Reaction and Flows: Traders moved assets from VXX to alternatives like VIXY, but the price premium on VXX remained for months due to the lack of supply.

VXX and VIXY usually move in tandem due to their similar tracking of VIX futures, but in 2022, Barclays' suspension of new VXX issuance created an unprecedented divergence. The March 2022 event highlighted the risks of trading ETNs versus ETFs—while VIXY functioned properly throughout the year, VXX became detached from reality, trading at a significant premium before finally reverting.

This case serves as a reminder that structural mechanics matter as much as market movements when trading volatility ETPs.