Triggering Events Change the Consequences, Not Just the Circumstances

A liquidity event, a practice sale, equity vesting, and a partnership buyout—on the surface, these look like milestones.

In reality, they’re transitions.

A triggering event isn’t defined by the headline. It’s defined by what it does to the consequences of your decisions.

The common misconception is that more capital simply expands opportunity. That with a larger balance sheet comes more flexibility, more upside, and more freedom.

But the structure shifts.

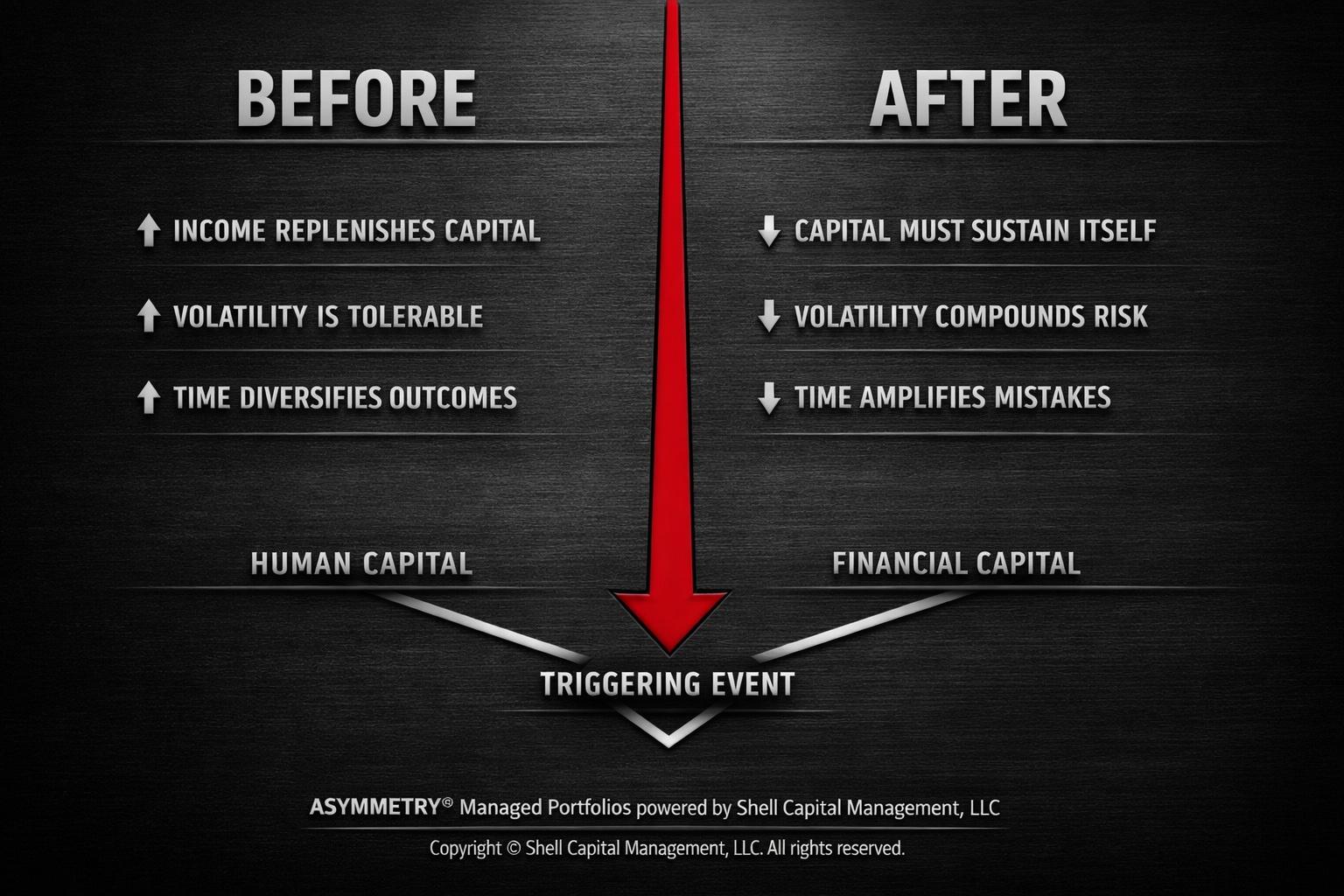

Before the event, risk is buffered by future earning capacity. Mistakes can be recovered from through time, income, and continued production.

After the event, capital becomes finite. Time becomes asymmetric. And errors carry a different weight.

This is the inflection point that most people miss.

From a first-principles perspective, a triggering event converts human capital into financial capital. It replaces a renewable resource with a depletable one.

That single shift changes everything:

The recovery function weakens. The downside becomes more permanent. The sequence of outcomes matters more than the average outcome.

This is where asymmetry becomes the central problem.

If you’re still operating under an accumulation framework—seeking returns without explicitly defining downside—you’re implicitly accepting exposure to outcomes that are no longer tolerable.

Because the consequences have changed.

From an ASYMMETRY® lens, triggering events redefine the payoff structure.

Before:

- Income replenishes capital

- Volatility is tolerable

- Time diversifies outcomes

After:

- Capital must sustain itself

- Volatility compounds sequence risk

- Time amplifies mistakes if unmanaged

Same markets.

Different reality.

This is where convexity and optionality either become intentional—or disappear entirely.

If downside is defined, position sizing is aligned, and liquidity is managed, a triggering event can create positive convexity. You preserve the ability to participate in upside while strictly controlling drawdowns.

If not, the same event concentrates risk into a smaller margin for error. Optionality collapses. The range of acceptable outcomes narrows—often without the portfolio being adjusted to reflect it.

Boundary conditions matter.

Not every life change is a triggering event. The distinction is whether the event forces a change in how capital must function.

Does it need to last longer?

Does it need to absorb more uncertainty?

Does it now represent security, not just growth?

If the answer is yes, the framework must change.

For business owners, physicians, surgeons, executives—this is the operator-to-investor transition.

You’re no longer primarily generating capital. You’re responsible for managing its exposure, its durability, and its ability to meet future obligations under uncertainty.

That requires a different discipline:

- defining downside in advance

- managing portfolio risk dynamically

- monitoring liquidity and volatility as primary variables

- structuring for asymmetry, not just return

The objective isn’t to maximize outcomes.

It’s to ensure that no single outcome can materially impair the future.

Triggering events don’t just change your circumstances.

They change what mistakes cost.

Mike Shell is the founder of Shell Capital Management, LLC, a registered investment adviser built for business owners preparing for and navigating a liquidity event. As a fiduciary—and a business owner for over two decades—he advises from the same side of the table, representing the owner’s interests at every step of the exit. This matters when the outcome isn’t just a sale price, but how much of that value is actually realized, retained, and compounded after the transaction.

Shell Capital was built on exit planning, orchestrating liquidity events, and managing the capital that follows with a family office mindset—focused on downside risk, optionality, and long-term control. Because the capital you unlock becomes the capital we manage, incentives are directly aligned: we don’t benefit from a transaction—we benefit from you getting it right.

If you’re within a few years of a potential exit, the decisions you make now will likely have an outsized impact on the outcome. That’s where we come in.