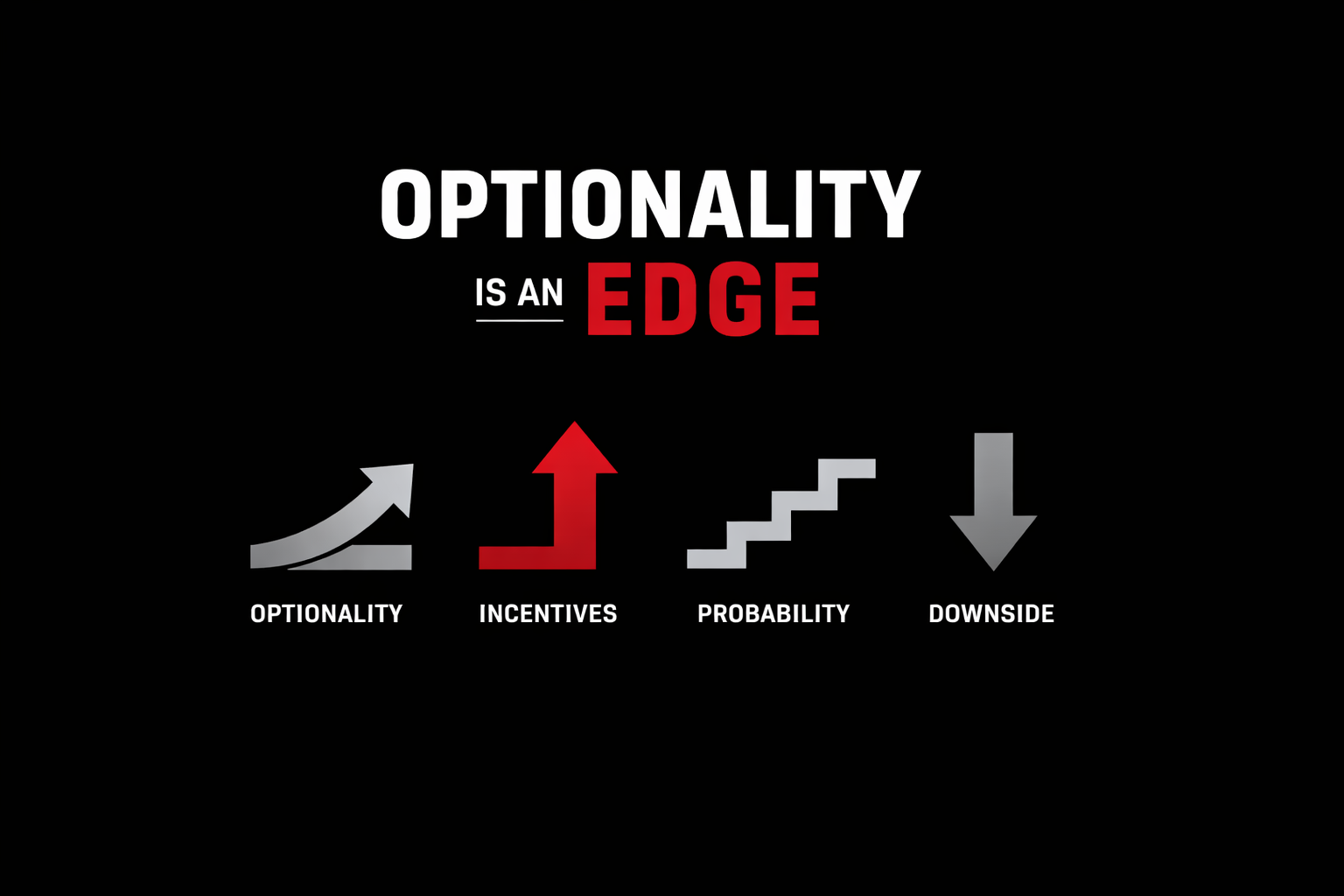

Gifts are given. Asymmetry comes from choices.

Talent may help investors understand markets, but it rarely determines outcomes. Asymmetric results come from choices—defining downside, sizing positions intentionally, and maintaining convex opportunities within a disciplined portfolio process.